EU ENERGY SECTOR: BP: Castrol Headlines

(BPLN; A1/A-/A+)

Prior speculated values had ranged from ~$10bn initially to <$8bn more recently so the valuation comes in the middle of this range. The sale has been well flagged and is part of the communicated disposal programme targeting $20bn by 2027 so not likely a spread mover. An $8bn deal could reduce reported EBITDA leverage by 0.2x to 0.5x (or 0.9x incl. leases) with deleveraging a communicated priority.

- FT: BP in advanced talks to sell Castrol for >$8bn to Stonepeak.

- Sale part of BP’s $20bn disposals target by 2027.

- BP may retain a minority stake.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

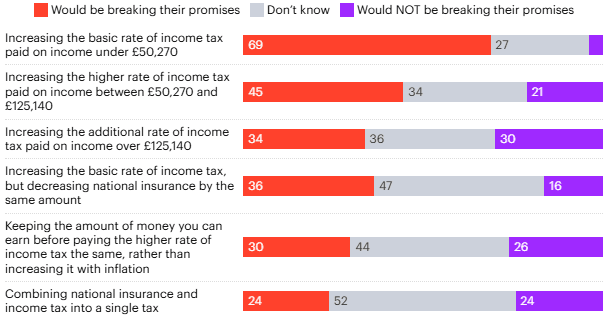

UK FISCAL: Poll: Voters Would See Basic Rate Tax Hike As Clear Manifesto Breach

The latest polling from YouGov shows that, while respondents are already anticipating tax hikes in the 26 November budget (UK FISCAL: Reeves Prepares Ground For Tax Hikes; Voters Already Expecting Them), the prospect of an increase to the basic rate of income tax would be a clear breach of its pre-election manifesto pledges.

- Amid rising speculation that the basic rate could be increased, 69% of respondents believe this would break the promise made pre-2024 election that Labour would not increase income tax, VAT, or National Insurance contributions. The proportion agreeing that the increase constitutes a breach falls to 45% when asked about an increase to the higher rate of income tax instead.

- The only potential policy polled that was on an even footing was when respondents were asked if combining income tax and National Insurance into a single tax would break pre-election promises, with 24% saying it would, 24% saying it would not, and 52% unsure.

Chart 1. Opinion Poll, 'What would count as Labour breaking their tax promises?', %

Source: YouGov. Fieldwork: 29-30 Oct.

OPTIONS: Expiries for Nov5 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1525(E630mln), $1.1600-20(E1.4bln)

- EUR/GBP: Gbp0.8745(Gbp753mln)

- USD/JPY: Y153.35-50($905mln)

- NZD/USD: $0.5650(N$1.2bln), $0.5675(N$1.2bln)

EURIBOR OPTIONS: ERM6 Call Buyer

ERM6 98.75 call, paper pays 1.0 in 9k

- ERM6 currently +1.0 tick at 98.045 today.