FED: Bowman And Waller Setting Up For A July Dissent

Though both Gov Waller and Vice Chair Bowman have come out after the June meeting and declared tentative support for a rate cut in July, this still appears to be a minority view.

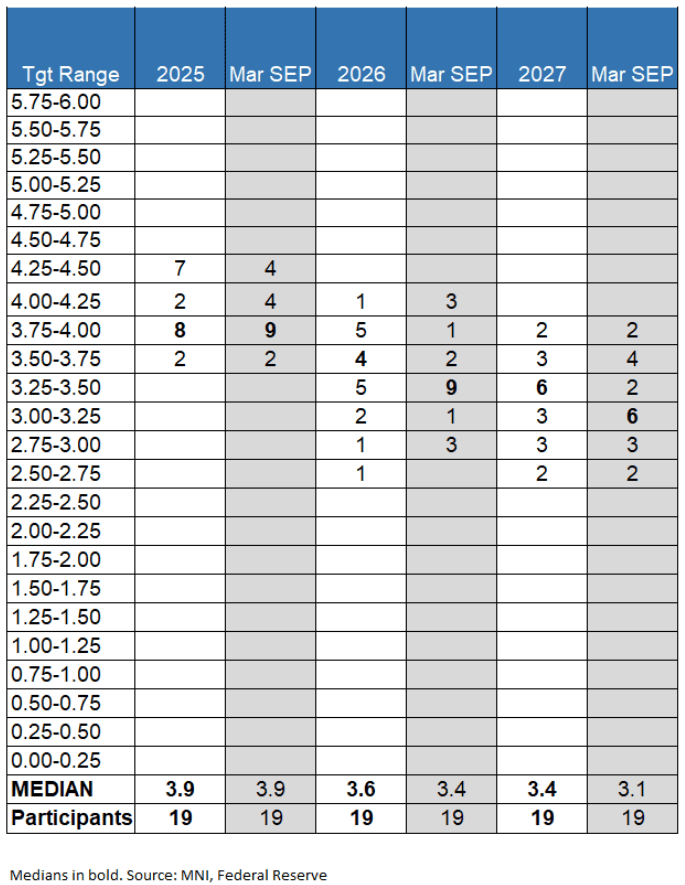

- They might be the two biggest doves on 2025 rates. While the SEP is not a perfect guide to guessing policy preferences, there were two 3.6% (75bp in cuts) dots in the June projections (see MNI's tabulation below) and those were the most dovish entries. We doubt opinions have changed much in less than a week, so we would think given they are looking at a July cut that they could well be looking for 3 cuts over the last 4 meetings of the year (Jul / Sep / Oct / Dec).

- Cynically speaking, both might be adopting dovish stances in angling for the top job at the Fed, with the White House's announcement of the candidate to replace Chair Powell next May possible at some point in the coming months. Waller is almost certainly in that conversation, though Bowman hasn't been seen as a major contender having just been given the Supervision job.

- But that said, their (stated) difference on policy with the majority of the Committee appears to be on fundamental grounds, centering on a) the impact of tariffs and b) the timeframe in which those impacts can be seen.

- Gov Waller has said repeatedly that his base case is for the tariffs to have a one-off impact on inflation, despite the risk that inflation is more persistent - arguments that Bowman, who has largely been silent on the issue for the last 5 months, appears to echo in her commentary. And both take the position that tariffs have not had a notable impact on inflation so far in the data, and that cuts could be necessary to bolster a labor market that is showing signs of deterioration.

- Contrast this with Powell last week who repeated that while the next easing "could come quickly", they would learn "a great deal more over the summer on tariffs".

- Indeed Bowman's comments about softening services PCE offsetting higher goods PCE sounded similar to Powell's last week. But Powell went on to emphasize that "we're beginning to see some effects [on core goods inflation]. We expect to see more". Bowman doesn't fully disagree but emphasizes the overall services vs goods impact, saying today "there will likely be only minimal impacts on overall core PCE inflation from changes to trade policy".

- It does raise the question of what kind of evidence would be sufficient by the July 30 decision for the Committee to cut rates. There's only going to be one more CPI report and one more nonfarm jobs figure by then. That's probably not to convince a patient FOMC majority to support an easing. That sets things up for two prominent dissents to a rate hold at the July meeting.

- But with Bowman not needed to be convinced of a need for easing, there is a much clearer path to rate cuts in the ensuing three meetings: we would guess most of the Board are in the 2-cut median camp already.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGB TECHS: (M5) Rallies off Lows

- RES 3: 147.74 - High Jan 15 and bull trigger (cont)

- RES 2: 146.53 - High Aug 6

- RES 1: 141.48/142.95 - High May 2 / High Apr 7

- PRICE: 139.40 @ 15:42 GMT May 23

- SUP 1: 138.54 - Low May 22

- SUP 2: 136.57 - 1.382 proj of the Jan 28 - Feb 20 - Feb 26 bear leg

- SUP 3: 134.89 - 2.000 proj of the Jan 28 - Feb 20 - Feb 26 bear leg

JGBs have rallied off recent lows and for now, however a bearish theme remains intact following the reversal that started Apr 7. A continuation lower would signal scope for an extension towards 136.57, a Fibonacci projection. On the upside, a reversal higher would instead refocus attention on 142.95, the Apr 7 high. The first important resistance to watch is 141.48, the May 2 high. A break of this level would be viewed as an early bullish signal.

US FISCAL: Total Tariff Income Jumping In May As New Rates Hit

Treasury reported a record $16.5B in customs/excise taxes on May 22, reflecting the large increase in tariff rates that went into effect in April.

- Today's report is important because it represents the largest tariff collections of the month which are typically on a due date around the 22nd, when most corporate importers make their payments.

- Thursday's one-day collection is a record, and the month has already set a new record. Tariff revenues have totaled $22.3B so far in May, and are came in at $17.4B in April (after averaging $8.1B/month in 2024).

- For the fiscal year as a whole so far, customs duties have totaled just under $93B, per the Treasury Daily Statement.

US FISCAL: Extraordinary Measures Continue To Dissipate Alongside Treasury Cash

Treasury's latest estimate of the size of "extraordinary measures" available to use "in order to prevent the United States from defaulting on its obligations as Congress deliberate[s] on increasing the debt limit" is down to $67B on May 21 (of an available $299B), vs $82B a week earlier.

- The amount hit the 2nd lowest level since the debt limit impasse started, at $46B, on May 20 (the low was $34B on Feb 24).

- With $476B in cash in the Treasury General Account on May 21, that left the total resources available to Treasury at $543B, the least since April 14 - the day before the annual April 15 tax deadline.

- Treasury Sec Bessent warned Congress earlier this month that "there is a reasonable probability that the federal government's cash and extraordinary measures will be exhausted in August while Congress is scheduled to be in recess. Therefore, I respectfully urge Congress to increase or suspend the debt limit by mid-July".