OIL: Bouncing 2% Ahead Of The Weekend, WTI Still Sub Late Oct Highs

Oil benchmarks have built on Thursday gains in the first part of Friday trade. Brent was last around $64.20/bbl, up close to 2% from end Thursday levels, and higher for the week. WTI is back around $60/bbl, up over 2% and also tracking higher for the week. Impact of US sanctions on Russian oil flows is being cited as a reason for bounce (with these sanctions kicking in over the next few days). Via BBG: "On Thursday, the International Energy Agency warned of “considerable downside risk” to its outlook for Russian output from the moves." Risks of US military action against Venezuela, has also been cited as risk factor (per BBG) and may be helping drive short covering ahead of the weekend.

- The broader backdrop still look like oversupply concerns will dominate from a medium term standpoint.

- From a technical perspective, Wednesday's sell-off in WTI futures strengthens a bearish theme. A continuation lower would pave the way for a move towards key support and the bear trigger at $55.96, the Oct 20 low. Resistance to watch is $62.59, the Oct 24 high.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

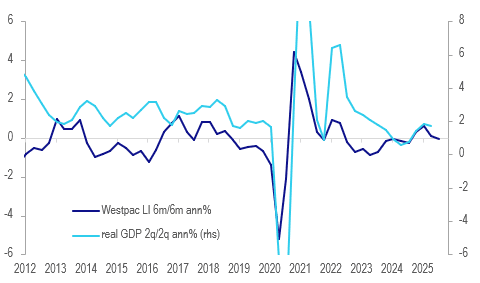

AUSTRALIA DATA: Westpac Lead Indicator Signals Around Trend Growth

The Westpac lead index fell 0.03% m/m in September bringing the 6-month annualised rate to +0.04% from -0.16%. It has oscillated around zero over the last 5 months. This measure leads detrended growth by 3 to 9 months and signals that growth may slow in H2 but be around trend early in 2026. Westpac is forecasting 2% growth in 2025 with it improving in 2026.

- Westpac forecast a 25bp rate cut at the November meeting but now believes that while the next move in rates is down, the upcoming decision will rely on Q3 CPI on 29 October. It notes though that its lead indicator signals GDP growth remains lacklustre.

- The indicator was stronger in H1 this year with the H2 moderation driven by dwelling approvals and AUD commodity prices. Westpac expects both of these components to turn with the latter already higher driven by gold and lower rates and policy likely to boost housing supply.

- Equity prices have been positive for the lead indicator over the last 6 months.

Australia Westpac lead indicator vs GDP %

JGBS: Futures Dips Supported As Tsys Push Higher, 20yr Auction Later

JGBs were a touch softer in the first part of trade, but sit back at 136.32, only -.01 versus settlement levels in latest dealings. The turn higher in US Tsy futures is likely providing some positive spill over for JGBs. Focus in the cash Tsy yield space will be on whether the 10yr yield can test under 4.00% (latest around 4.015%).

- For JGBs broader ranges continue to hold, with upside resistance still intact, while Tuesday highs were just above 136.50.

- In the cash JGB space, back end yields are softer for the 10yr through to 40yr. The 10yr last around 1.65%, 20-40yr tenors off 2-4bps. The 30yr leading.

- The front end of the curve is more stable, leaving the 2/30s curve flatter by 5bps to +228bps.

- We have the 20yr auction later.

- The opposition parties will meet at 4pm local time, ""*JAPAN'S TAMAKI: TO HOLD 3-WAY OPPOSITION PARTY TALKS AT 4 P.M.", via BBG. This comes ahead of next week's Diet session on Oct 21, where a new PM is expected to be elected. Uncertainty continues on who this will be, but Polymarket still has odds with LDP leader Takaichi.

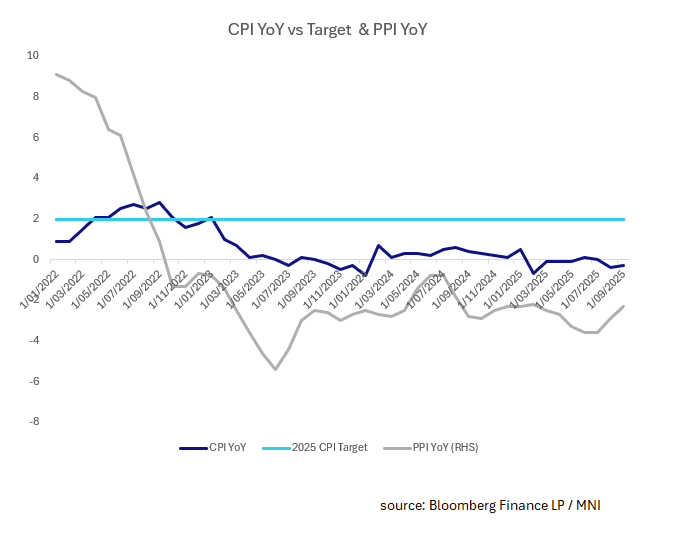

CHINA: No Good News from Inflation Releases

- The deflationary problem facing the Chinese economy was in full view today with the release of the September CPI and PPI.

- The CPI at -0.3% missed estimates of -0.2% as one of the longest streak of price declines in decades continues.

- To add to the PPI decline, factory gate prices (PPI) YoY declined -2.3% YoY.

- What started with a housing market crash post pandemic morphed into over capacity issues by manufacturers leading to price wars and has resulted in the government attempting to intervene to stop the price cuts.

- The GDP deflator has been in decline also for two years and as the broadest measure of prices; shows that the deflationary pressures are the strongest they have been since data began.

- Some domestic media outlets suggest that policy adjustments are needed imminently, though the first half of the year saw GDP better than expected. In the coming days we will get 3Q GDP (forecast is a decline to +4.7% from +5.2%).

- The next potential for seeing policy adjustment is the 1-Year and 5-Year Loan Prime Rate decisions on October 20. LPR's were last changed in May with some market commentators suggesting a further cut could be getting closer. Other market observers suggest a further adjustment to the RRR is the likely pathway for policy.

- The CBG 10-Yr had edged up in yield this morning to 1.84% whilst 10-Yr bond futures are lower by -0.12.