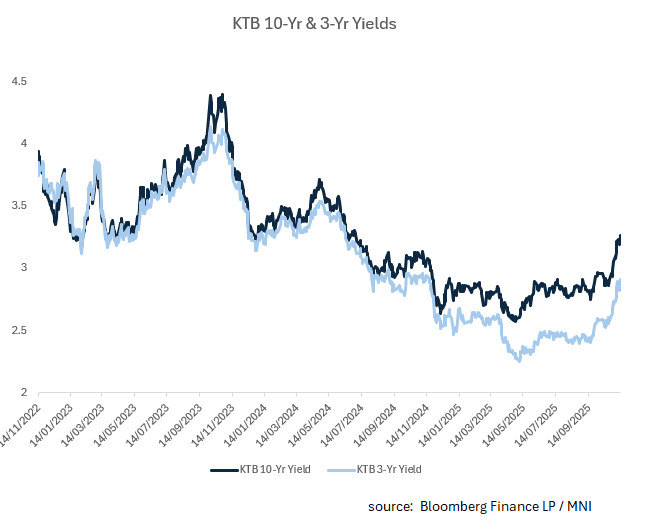

SOUTH KOREA: Bond Markets React to Rhee Comments, Rate Cuts a Memory

- Last week we noted that the recent BOK decision driven by concerns from the housing sector and an improving trend for CPI will likely see the BOK on hold for some time. The housing market challenge is something that many developed nations have faced or are still facing and that up until recently, the Korean swaps curve had a mid year 2026 cut priced in, but no longer does. In the bullet we asked the question whether the next move for the BOK is up? (source MNI)

- Korean bond futures have fallen for throughout November, down -1.97pts on the 10-Yr bond futures, with up days followed by losses the next day in excess of the gains.

- 10-Yr Korean treasury futures were down -0.28 in the morning session as the unwind of rate cuts continued. However, comments from the BOK Governor Rhee that the BOK 'remains in an easing cycle, but the timing and size of cuts may shift depending on data," and that Seoul's property prices were "way above" the central bank's expectations, and authorities need to see how the government's steps to cool the market play out" drove bond futures even lower, finishing down -0.71 at 114.29.

- The market reaction seems overdone, an idea supported by the rally at the open today as what Governor Rhee said, has been said before.

- However, as pointed out yesterday in our bullet "Inflation Green Shoots Could See Rates on Hold for Near Term, " given the focus on the Seoul property market, the BOK could be on hold for some time.

- In the cash government yield space, we are up strongly in Nov to date, see the chart below. Buying interest may emerge on further extensions higher (3% for 3yr and close to 3.50% for the 10yr), particularly with still modest growth prospects into 2026.

Fig 1: South Korean 3yr and 10yr Bond Yields

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OIL: : Crude Continues Recovery Watching Supply/Demand Outlook Key Though

After sinking around 5% on Friday driven by energy demand concerns in the face of renewed US-China trade tensions, oil prices recovered slightly on Monday following President Trump taking a step back and the associated improvement in risk appetite. There had also been a Ukrainian strike on a major Russian refinery on the weekend. The market watches these developments closely as they risk refined product supplies and may have contributed to an increase in Russian crude exports.

- WTI rose 1.1% to $59.56/bbl after reaching $60.17 and has started Tuesday around $59.76. Moves above $60 were brief. It is down 4.4% this month. Initial support is at $58.22, 10 October low, with resistance at $62.75, 50-day EMA.

- Brent is currently around $63.52/bbl after increasing 1.0% to $63.39. It was unable to break through $64 yesterday reaching $63.95. The benchmark is 4% lower in October with a bearish threat remaining. Initial support is at $62.00, 10 October low, while resistance is $66.31, 50-day EMA.

- OPEC published its October report on Monday keeping its oil demand forecasts unchanged at up 1.3mbd in 2025 and 1.4mbd in 2026. The group tends to be more optimistic than others. The IEA’s report is out Tuesday and it tends to be more cautious with it expecting a market surplus in 2026 for some time.

- Non-OPEC supply is forecast to rise 800kbd in 2025 and 600kbd in 2026 driven by US, Canada, Brazil & Argentina. Output from OPEC+ rose 630kbd in September according to the group’s report. It agreed to increase production by 137kbd in both October and November but most members are now facing capacity constraints which may impact its ability to lift supply and gain market share, except for Saudi Arabia.

JGBS: Focus On Whether Futures Bounce Can Be Sustained As Onshore Returns

JGB futures finished up at 136.42, +.52 versus settlement levels. Prices surged Monday, in sympathy with global bond markets, helping the price rally toward last week’s high. Sentiment was buoyed by the flight to bond markets, although with equity sentiment stabilizing focus will be on whether this is sustained. We will need to challenge resistance before signaling a broader reversal. Key short-term resistance has been defined at 137.30, the Sep 8 high. The latest sell-off, however, resulted in a break of support at 136.19, the Sep 4 low and a bear trigger. Clearance of this level confirms a resumption of the downtrend and opens 135.39 next, a Fibonacci projection.

- Cash JGBs finished up last Friday at 1.69% for the 10yr (just off cycle highs), while the 2/30s curve was at +228bps, slightly steeper.

- Japan markets return today. Politics remains a focus point, with opposition parties set to meet today to discuss the collapse of the governing coalition last week. These meetings could help determine whether Takaichi goes ahead with a minority government, or looks to bring forward elections. Her odds of becoming the next PM have slid to 77, per Polymarket (down from post LDP leadership election highs near 100).

- Locally on the data front Sep money stock figures, not typically a market mover.

- Note tomorrow we have a 20yr debt auction.

NZD: Kiwi Lower Following RBNZ LVR Decision, Economy Continues To Need Support

NZDUSD declined to 0.5721 following news that the RBNZ would increase the share of loans with an LVR above 80% from 1 December, an easing of financial conditions. The pair is currently trading slightly above that level. It was around 0.5728 before the news after dipping briefing on data showing a contraction in retail spending in September.

- Kiwi was one of the better G10 performers on Monday with NZDUSD slightly higher at 0.5725 off the intraday low of 0.5719.

- September retail card transactions fell 0.5% m/m after rising 0.6%, the first negative after three consecutive increases. Annual growth slowed to 1.2%. Despite the soft end to Q3, the quarter saw a 0.6% q/q increase in nominal retail spending. Q3 retail sales volumes are released 27 November. They rose 0.5% q/q & 2.3% y/y in Q2.

- Aussie outperformed on Monday leaving AUDNZD up 0.6% to 1.1379 after reaching 1.1384 with the pair partially regaining some of Friday’s losses. It is currently up 0.1% to 1.1387. With more NZ easing widely expected and not even a full 25bp priced in for Australia by end-2025, AUDNZD could return and even go beyond its post-October RBNZ rate cut highs.