MALAYSIA: BNM on Hold

- Malaysia’s central bank (Bank Negara Malaysia) kept the benchmark interest rate unchanged as widely expected whilst highlighting concerns as to the growth outlook from lingering external risks.

- The overnight policy rate was maintained at 2.75% at the second-last meeting scheduled for 2025.

- 22 of the 24 economists polled by BBG forecast no cut.

- At the current level, BNM said it “considers the monetary policy stance to be appropriate and supportive of the economy amid price stability”.

- Data over the period since the last meeting suggests that robust domestic demand remains the backbone of growth, rather than exports, whilst inflation remains below forecasts.

- Following the cut at the July meeting, a move the BNM described as ‘pre-emptive’, and the May decision to reduce the reserve requirement ratio, it seems that for now the BNM are happy to sit with those changes to preserve growth.

- The economy is expected to grow between 4.0% and 4.80% this year with domestic demand expected to ably supported by growing investment activity.

- The Ringgit finished Thursday softer by -0.13% at 4.2257. The bond market rallied into the meeting, with the MGS 10-Yr down -5bps from Wednesday's close, risking a reversal today.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Unchanged, Q2 Employment Largely In Line

In local morning trade, NZGBs are unchanged so far after the release of Q2 Employment data.

- Q2 NZ employment fell 0.1% q/q to be down 0.9% y/y, in line with consensus, and the unemployment rate rose 0.1pp to 5.2%, slightly lower than expected but in line with the RBNZ’s May forecast. It is the highest rate since Q4 2016 excluding Covid. Private wages were higher than expected rising 0.6% q/q, but in line with the RBNZ.

- US tsys finished mixed Tuesday, curves twisting flatter, following stagflationary July's ISM Services data and a weak 3Y auction that drew 3.669% high yield vs. 3.662% WI.

- The headline Services PMI reading fell by 0.7 points to 50.1 (51.5 expected, 50.8 prior), merely a 2-month low but suggesting that an expected pickup in momentum and sentiment is not materializing.

- Swap rates are unchanged.

- RBNZ dated OIS pricing is little changed across meetings. 23ps of easing is priced for August, with a cumulative 41bps by November 2025.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 1.75% May-41 bond.

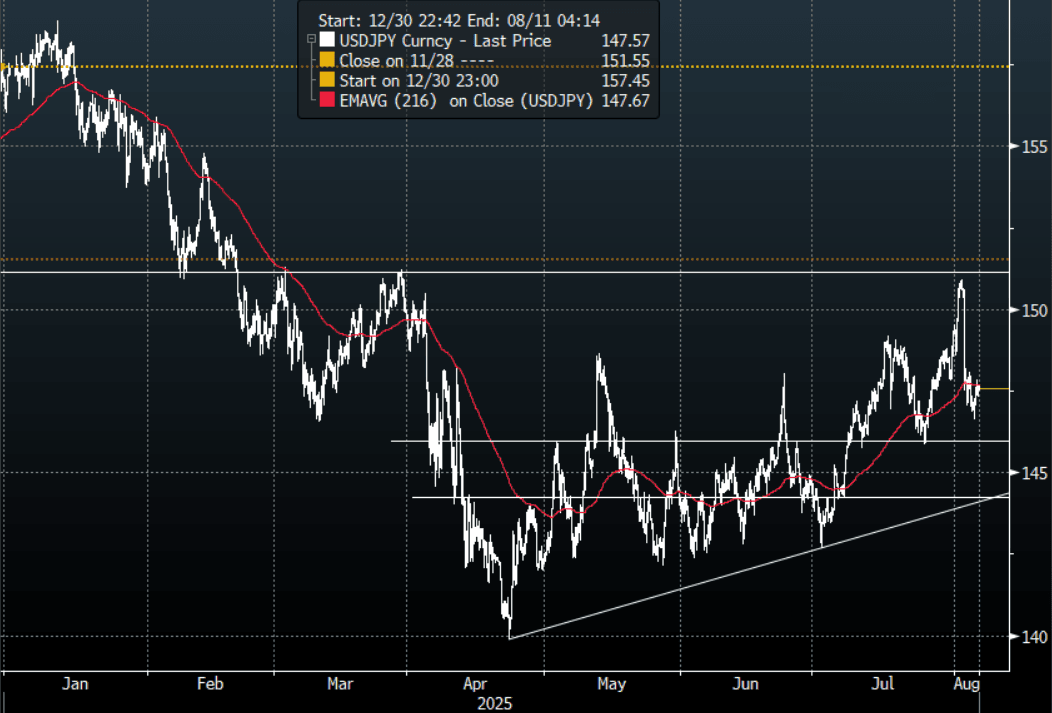

JPY: USD/JPY - Consolidating Below 148.00

The overnight range was 147.03 - 147.83, Asia is currently trading around 147.55. USD/JPY managed to bounce off its support around 146.50 but has again stalled back towards the 148.00 area as risk closes poorly. Price has moved very quickly away from the pivotal 151/152 area much to the relief of Institutional JPY longs and the BOJ. CFTC Data shows leveraged accounts had started to aggressively build Yen shorts last week so this quick move lower would be a bitter pill to swallow. Price is holding above the support area around 146.50/147.00, a move sub 145.00 is needed to turn momentum lower once more, until then the 145.00-151-00 range should dominate.

- Bloomberg - “ In a break from a decades-old policy, the Japanese government will encourage farmers to disregard a de facto cap on rice production and boost cultivation of the food staple, a step that could win support from the agriculture sector and soothe consumers' frustration over soaring living costs.”

- “(Bloomberg) - The Japanese yen has rallied more than 2% so far this month, among the biggest gainers out of 31 G-10 and EM currencies tracked by Bloomberg. The outperformance will persist as stalling US economic growth boosts the yen’s haven appeal, while seasonal patterns support an extension of the rally.” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.00($1.5b).Upcoming Close Strikes : 147.65($1.14b Aug 7), 148.50($1.24b Aug 7) - BBG.

- CFTC data shows asset managers surprisingly added slightly to their JPY longs +75119( Last +72326), while leveraged funds aggressively added to their newly built short JPY position -31280(Last -11571).

- Data/Event : Real Cash Earnings

Fig 1 : USD/JPY Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

NEW ZEALAND: Unemployment Lower Than Expected, Private Wages Higher

Q2 NZ employment fell 0.1% q/q to be down 0.9% y/y, in line with consensus, and the unemployment rate rose 0.1pp to 5.2%, slightly lower than expected but in line with the RBNZ’s May forecast. It is the highest rate since Q4 2016 excluding Covid. Private wages were higher than expected rising 0.6% q/q, but in line with the RBNZ. See Statistics NZ press release here. More details to follow.