US TSY FUTURES: BLOCK: Mar'26 30Y Ultra-Bond Sale

Jan-02 14:41

- -1,600 WNH6 117-19, sell through 117-20 post time pib at 0934:30ET, DV01 $293,000.

- The 30Y ultra contract trades 117-17 last (-15)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

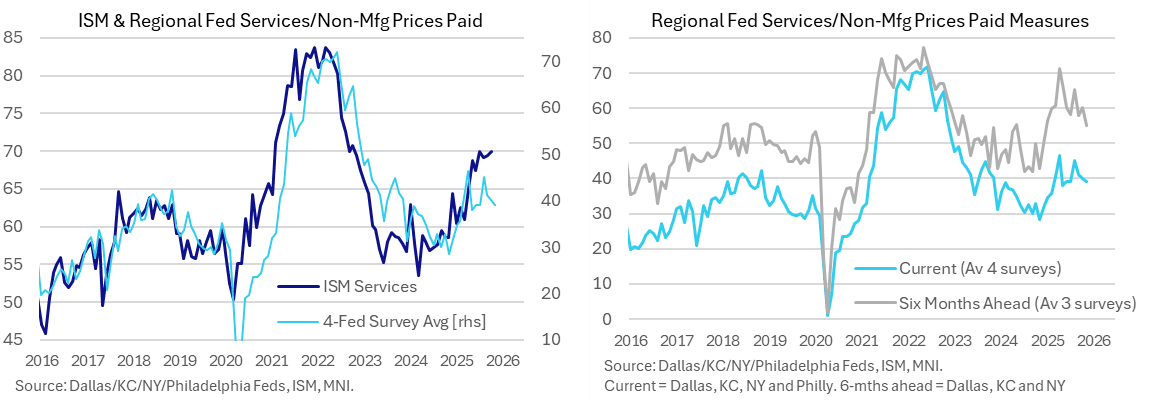

US OUTLOOK/OPINION: Two-Sided Risks To ISM Services Prices Paid From A High Base

Dec-03 14:37

- Bloomberg consensus sees the ISM services prices paid index slip 2pts to 68.0 in November after the surprise 0.6pt rise to 70.0 in October poked it above 69.9 in July for the highest since Oct 2022.

- It does however from a typically small survey sample of just three responses vs 51 for the headline services index.

- There are two-sided risks here from alternate indicators, with regional Fed surveys pointing to larger downside but the flash services PMI reporting its fastest cost inflation since Jan 2023.

- Regional Fed services/non-manufacturing surveys have been pointing to downside risks here through 2H25. That remained the case in November with an average of four surveys edging 1pt lower to 39.1 for its lowest since July – see the chart below noting that you can’t translate these absolute levels 1:1 for the ISM series.

- As for how service firms might be thinking about price pressures ahead, a smaller average of three regional Fed surveys saw prices paid six-months ahead ease 5pts to 55.0 in November for its lowest since Dec 2024.

- Firmly going against this however was the flash S&P Global US services PMI for November, reporting that “Service sector costs rose at the fastest rate since January 2023”. Further, when it comes to broader inflation perspectives, “selling price inflation slowed in manufacturing but reaccelerated in services.”

- Both were a clear uptick from a softer October when input cost inflation saw its lowest in six months along with selling price inflation also at its weakest since April.

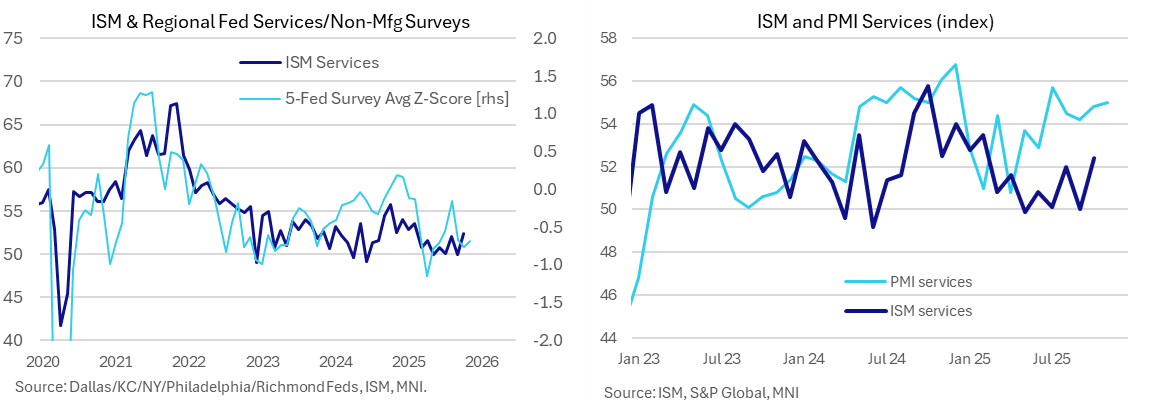

US OUTLOOK/OPINION: ISM Services Seen Dipping In Nov Despite Optimistic PMI

Dec-03 14:35

- Released at 1000ET, the ISM services index is seen dipping to 52.0 in November to only modestly ease after a stronger than expected eight-month high of 52.4 in October.

- The index has ranged between 49.9 (May) and 53.5 (Feb) so far this year and more recently oscillated between 50 and 52 handles since July.

- Alternate indicators on balance point to some limited upside but that's mainly from the services PMI, which is typically much more optimistic and by notably differing amounts month-to-month.

- S&P Global PMI: upside. The services PMI ticked up further to 55.0 in the flash November release from 54.8 in October for a fresh high since July and before that Dec 2024. As such, it points to both directional and level upside risk but, just as with the manufacturing survey, it has been far more optimistic than its ISM counterpart. It has averaged 3.4pts higher than ISM services in the latest six months but with a range of 2.1-5.6pts which means its predictive power should be viewed cautiously.

- Regional Fed surveys: neutral. The average of five regional Fed service/non-manufacturing surveys ticked down from -12.2 to -12.5 whilst the z-score inched higher from -0.8 to -0.7. The latter points to a small directional improvement on the month but is starting from a relatively lower level - see chart. The combination sees little conviction on risks to the ISM reading this month.

- There's no consensus for new orders although we'll watch them closely to see if it's possible to decipher a trend after what has been a particularly noisy few months (56.2 in Oct, technically a twelve-month high, after 50.4 in Sep and 56.0 in Aug). The flash PMI (link) encouragingly noted the "largest rise in new business so far this year" along with its "strongest output gain since July".

- The employment index meanwhile steadily increased in Sept and Oct to 48.2, still contractionary but a five-month high nevertheless. With no more BLS payrolls data due before the Dec 9-10 FOMC meeting, that should carry greater weight than usual.

EQUITIES: US Cash Opening calls

Dec-03 14:27

SPX: 6,818.5 (-0.2%); DJIA: 47,409 (-0.1%/-65pts); NDX: 25,445.4 (-0.4%) .