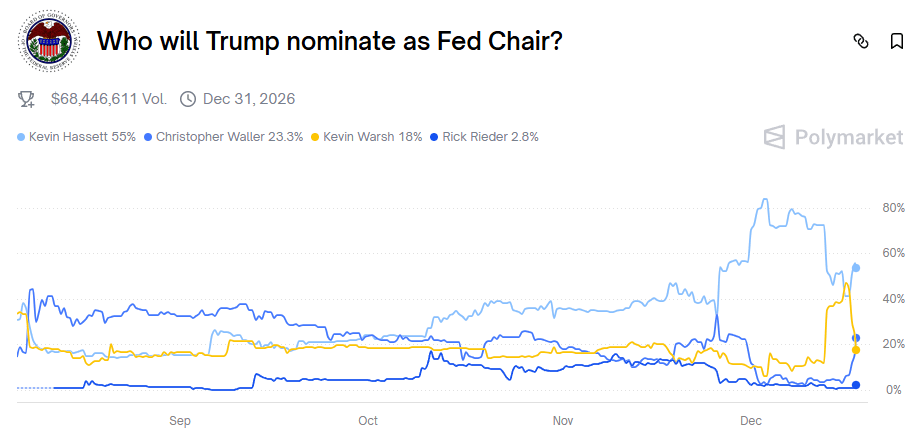

FED: Bessent Pushes Back On Latest Criticism Of Hassett As Potential Fed Chair

- "*BESSENT: ANY CONCERN ON HASSETT AT FED 'IS ABSURD'

- *BESSENT: HASSETT IS EMINENTLY QUALIFIED, WITH VIEWS OF HIS OWN" - bbg

Bessent echoing his stance although this time following Politico late yesterday citing three people familiar with the matter that Trump officials have raised doubts about Hassett. Despite those latest reports, Hassett's probability of becoming next Fed chair is higher on the day at 55%. Waller (23%) has overtaken Warsh (18%, down from almost 50% at one point in the last two days) with the two seemingly vying for the role if Trump wants to go down the route of choosing a previous Fed Governor. (All probabilities from Polymarket)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Majority Leader Thune To Hold Procedural Votes On FY26 Bills This Week

The Senate will return on Tuesday for a short week, before departing again on Thursday for the Thanksgiving recess. Senate Majority Leader Thune (R-SD) is expected to tee up procedural votes on the next ‘minibus’ FY2026 appropriations package, including bills funding Defense, Labor-HHS, Commerce-Justice-Science, and Transportation-HUD.

- Punchbowl notes, “Moving forward will require 60 votes, but it’s unclear whether enough Democratic senators will be ready to formally kick off the floor process, especially as the Democratic Caucus is still reeling over last week’s shutdown-ending deal. Thune will also need unanimous consent to group the funding bills together. That’s going to be extremely difficult, with objections expected on both sides of the aisle.”

- The route to legislating all twelve of the annual spending bills before government funding expires on January 30 appears fraught. The three FY26 bills included in the minibus package to reopen the government had all been previously negotiated with the House.

- None of the remaining nine funding bills have been conferenced yet, so have major gaps in topline spending levels and policy priorities. If the remaining nine bills aren’t passed by both chambers by January 30, another short-term funding bill will be required to avert a second government (partial) shutdown.

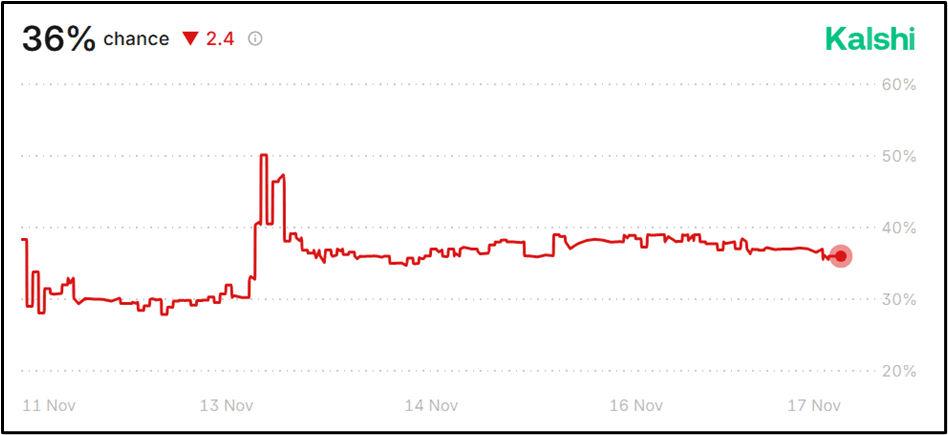

- According to Kalshi, the implied probability of a shutdown on January 31 is 36%. We expect this to rise in the coming weeks if bipartisan progress isn't made on the spending bills.

Figure 1: Government Shutdown on January 31, 2026

Source: Kalshi

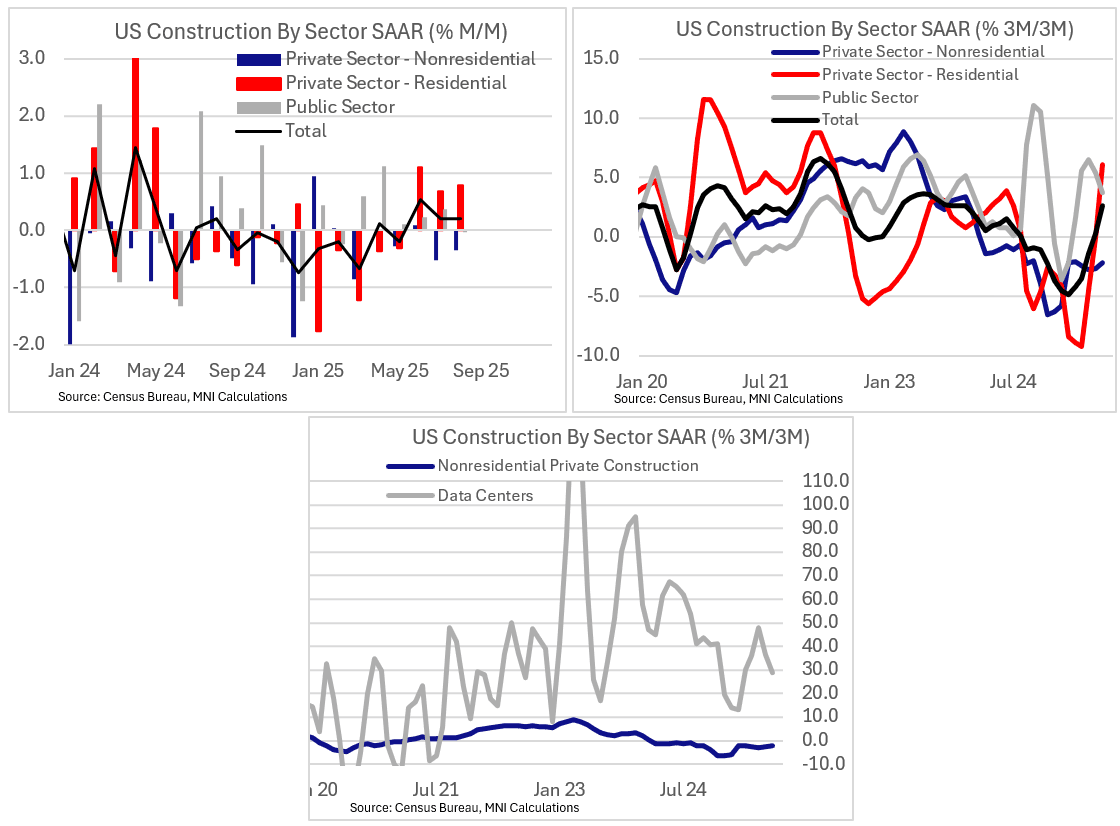

US DATA: Housing Is Starting To Lead Construction Growth As Data Centers Slow

August construction data - whose Oct. 1 release was delayed 6 weeks due to the federal government shutdown - showed a 0.2% M/M rise in spending (-0.1% expected, 0.2% prior rev from -0.1%). Overall construction looks to be stronger on the residential side than it did earlier in the year, boding positively for that side of the GDP equation, with public sector construction also looking solid enough. However, non-residential construction growth has stalled amid policy uncertainty, with even the vaunted data center boom showing signs of moderating over the summer.

- This was the 3rd consecutive rise in construction (which is expressed in seasonally-adjusted annual rate and nominal terms), the longest expansion since 2023. And the recent pickup is being driven by private sector construction: it rose 0.3% for a 3rd consecutive gain and is now rising 2.3% on a 3M/3M annualized basis following 11 consecutive declines.

- Somewhat surprisingly given the travails of the housing market, the pickup is being driven by residential construction - a 0.8% rise saw the 3M/3M rate jump to 6.1% for the first positive reading since August 2024 and the highest overall since April 2022 (the level is now at the highest of the year).

- Conversely nonresidential construction has contracted 2 months in a row, including manufacturing, both of which are at the lowest levels since 2023.

- One trend worth noting is an apparent slowdown in data center construction. It's still growing at an extremely elevated pace overall, 29% 3M/3M annualized in August, but this is down from nearly 100% at peaks in 2023/24.

- Public sector spending has been consistently positive for the last 6 months, making October's flat reading the weakest since February, but this is still an overall contributor to construction spending. There was virtually no growth in data center construction by value between June and August. That being said, this series has increased 4-fold since the end of 2021 and is worth about 5.5% of total non-residential private construction, up from 2% in that span.

OPTIONS: Expiries for Nov18 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600-05(E915mln), $1.1675(E1.4bln), $1.1700(E1.0bln

- USD/JPY: Y153.00($1.3bln)