POLAND: Below-Forecast Inflation Boosts Sell-Side Calls For Rate Cut Next Week

Poland's headline inflation cooled to +2.8% Y/Y in August, according to preliminary data from the statistics office, undershooting expectations and moving closer to the +2.5% point-target. Recent communications from MPC members suggested that they expected inflation to print at +2.9%. A rough breakdown of the data suggested that core categories drove the surprise, which would be another argument for the MPC to resume interest-rate cuts. Detailed data and official estimates of core inflation will be published on September 15 and 16, respectively, after the NBP's next monetary policy meeting slated for September 2-3.

- ING note that inflation was close to the NBP's target in August and the downtick in headline figure was driven by lower core inflation (down to +3.1-3.2% Y/Y from +3.3%). In their view, this seals the deal on a September rate cut, but we may need to wait for the next ones. MPC members indicated that the NBP is not in a a rate-cutting cycle, while the government unveiled a high deficit target for 2026.

- mBank write that core inflation eased to +3.0-3.1% Y/Y amid a significant cooling of its momentum. If confirmed, this would represent a very positive, disinflationary piece of information. In their view, the MPC may cut rates in September with confidence.

- Pekao write that the inflation reading was lower than expected thanks to a slowdown in core inflation to around +3.1% Y/Y, which is an additional positive piece of news. In their view, this should be a sufficient arguments for the MPC to cut interest rates next week.

- PKO take note of below-forecast inflation and note that fuel prices (-1.9% M/M) were the main source of the downside surprise. Core inflation fell by a significant margin, in their view, to around +3.0% Y/Y. Food (+4.8% Y/Y) and energy +2.3% (Y/Y) inflation also ticked lower. They note that yesterday's comments from MPC's Iwona Duda suggest that the central bank's forecast

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

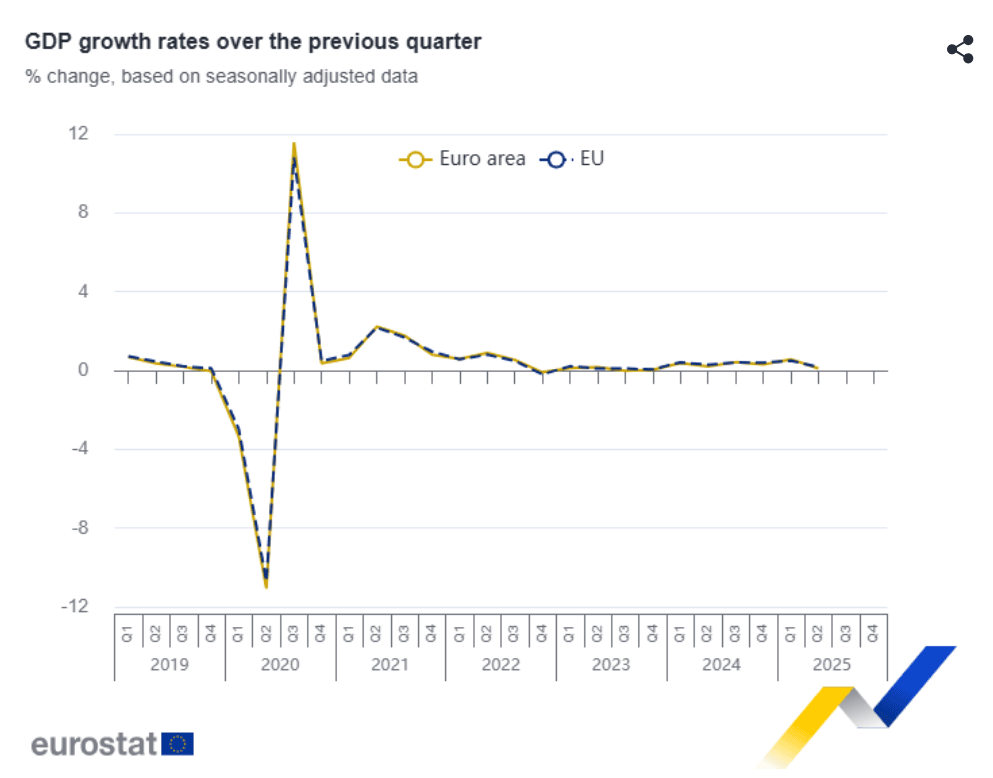

MNI: EUROZONE Q2 PRELIM FLASH GDP +0.1% Q/Q

- MNI: EUROZONE Q2 PRELIM FLASH GDP +0.1% Q/Q

- EUROZONE Q2 PRELIM FLASH GDP +1.4% Y/Y

EUROZONE DATA: Upside Risks To Q2 Eurozone GDP Materialize

Eurozone GDP printed 0.1% Q/Q in Q2, slightly stronger than consensus of 0.0% and slightly softer than the ECB's 0.2% staff projection. It was below Q1's outsized 0.6%.

- Ireland, which had a strong upward contribution in Q1, dragged the print lower this time at -1.0% Q/Q.

- Across the four major economies, detailed information on the Q1 data is lacking. Drivers across countries are mixed, with Germany mentioning stronger private and government consumption but weak investment, France seeing a material inventory contribution but weak domestic demand, while Italy and Spain both see positive domestic demand.

- Summarising the main quarterly GDP prints released yesterday/this morning:

- Eurozone: 0.1% Q/Q vs 0.0% cons, 0.6% prior.

- Germany: -0.1% Q/Q vs -0.1% cons, 0.3% prior.

- France: 0.3% Q/Q vs 0.1% cons, 0.1% prior.

- Italy: -0.1% Q/Q vs 0.1% cons, 0.3% prior.

- Spain: 0.7% Q/Q vs 0.6% cons, 0.6% prior.

BONDS: Off Highs Into Italian & UK Bidding Deadlines

Impending bond supply out of Italy and the UK probably factor into the pullback in core global FI in recent trade, macro headlines fairly limited.