FED: Beige Book: Employment Responses Continue Trend Deterioration

Nov-26 19:49

- You can clearly see the deterioration over time in the breadth of employment level responses in the table below.

- Whilst one district seeing a small increase isn’t unusual, there is starting to be a clearer shift to those seeing declines albeit still mostly only slight declines at this stage.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Macro Since Last FOMC - Prices: Data Quality Concerns Increase

Oct-27 19:49

- When thinking about how the Fed will view this report, it’s important to note that translating it to core PCE with no publication of a PPI report would have been hard enough this month (CPI provides ~65% of inputs), but uncertainty is greater still with a deterioration in the quality of the CPI report itself.

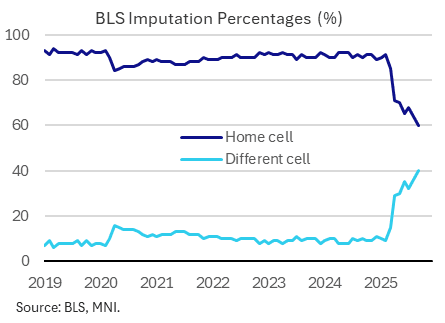

- September saw 40% of sources using “different cell” imputation, a new high after 36% in August as budget and staff cuts have an increasingly large impact. It has historically averaged closer to 10% and peaked at 15% in the pandemic when in-person surveys weren’t possible, but it jumped to ~30% April and has continued to increase since.

- This September release shouldn’t have been impacted by the government shutdown in the sense that the data would have already been collected.

- The shutdown was however seriously calling the quality of the subsequent October report into question, although the White House's Rapid Response account on X.com suggests that the BLS may not release it because it was unable to conduct the in-person surveys as normal during the month.

- As for alternative timely indicators, the Fed’s Beige Book published Oct 15 was arguably the most inflationary Beige Book of 2025, certainly joint with June which saw 8 (of 12) districts characterize inflation pressures as "moderate", despite weaker growth conditions.

FED: Macro Since Last FOMC - Prices: A Lone CPI Report Surprises Softer

Oct-27 19:47

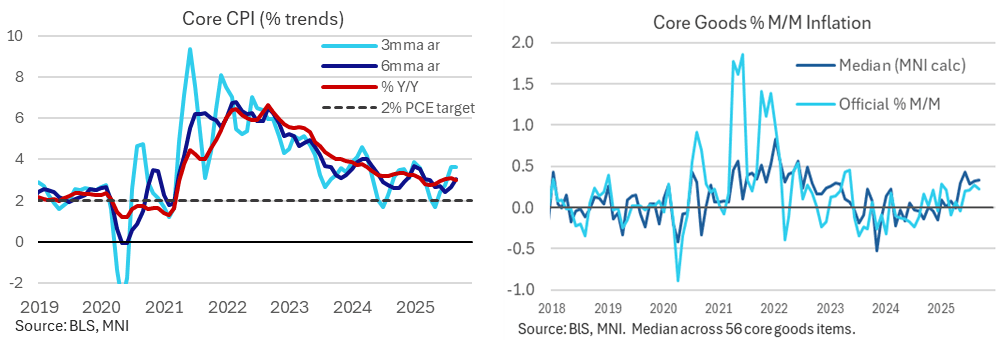

- The September CPI report was clearly softer than expected, with core inflation at a seasonally adjusted 0.23% M/M (unrounded consensus of 0.32) after 0.35% in August, back to the pace seen in June after two 0.3% readings.

- Core goods were one weak point with markets still firmly on tariff passthrough watch, increasing 0.22% M/M (consensus 0.34) after 0.28% M/M in August with a surprise decline in used car prices partly at play.

- Our look at broad price pressures within the core goods basket suggests September saw a very similar picture to August, with the peak coming back in June rather than seeing any additional acceleration in tariff passthrough. It continues to run a little hotter than the official core goods series but with a smaller gap than a few months ago.

- Elsewhere on the services side, rental inflation was softer than expected and included a sizeable reversal of OER inflation after a southern-based spike the prior month. The 0.26% M/M average for rental inflation over August and September sees it maintain its return to pre-pandemic run rates as has broadly been the case since the middle of the year.

- Core services excluding housing were still firm however at 0.35% M/M and are now running at 4.7% annualized over three months or 3.3% over six months, but this metric has poor correlation with its PCE counterpart.

- Taking more of a step back, core CPI inflation surprisingly eased back a tenth to 3.0% Y/Y after two months at 3.1%, still within a 2.8-3.3% range seen since mid-2024. Three-month core CPI inflation stands at 3.6% annualized whilst the six-month is softer at 3.0% annualized.

BOC: MNI BoC Preview-Oct 2025: Mixed Data Unlikely To Derail Cut

Oct-27 19:36

The Bank of Canada is set to cut its policy rate by 25bp for a second consecutive meeting on October 29 - MNI's preview is Here

- The new 2.25% overnight rate would represent the bottom of the BOC's "neutral" estimate range (2.25%-3.25%), reflecting an environment in which economic slack has built amid the fallout from the US-Canada trade conflict but with trim/median inflation continuing to run at the high end of the BOC's target band.

- Overall the data remains volatile and mixed, with stronger-than-expected CPI and labour market data for September not enough to derail another cut amid increasingly muted private sector inflation expectations and a limited rebound in economic activity after Q2's sharp contraction.

- Overwhelming market and analyst conviction on a 25bp cut appears to understate risks of a rate hold, especially given the mixed inter-meeting data.

- But Gov Macklem appeared to give the green light to a cut in recent comments, and a cut should be considered much more likely than a pause.

- Macklem is unlikely to deliver any clear signals about future decisions at the press conference, keeping market pricing split between one further 25bp cut in the cycle vs no further easing.