USDCAD TECHS: Bearish Outlook

* RES 4: 1.3845 High Jan 22 * RES 3: 1.3800 High Jan 23 * RES 2: 1.3725/3753 High Feb 6 and 24 / Hig...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

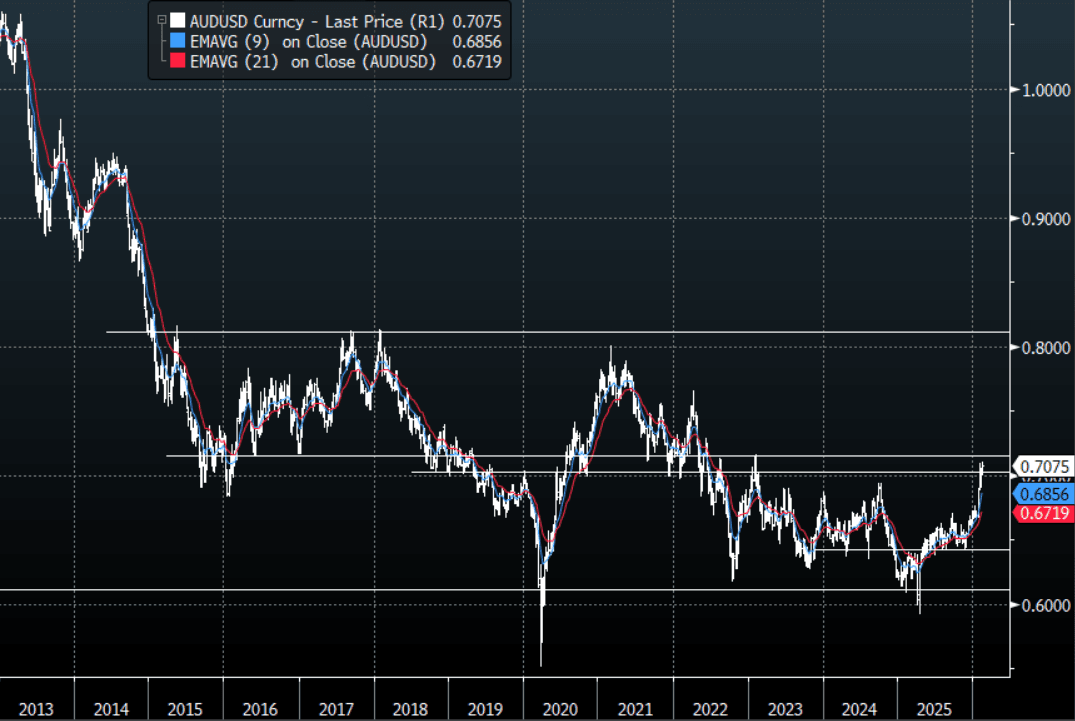

AUD: AUD/USD - Stalls Toward 0.7100 As Market Awaits NFP Data

The AUD/USD had a range overnight of 0.7065-0.7091, Asia is currently trading around 0.7080. The AUD’s momentum has stalled toward 0.7100 as the market awaits the US labour data tonight. The USD is again back under pressure and the move lower in yields is just adding to its headwinds, the AUD remains a favourite to express a long against it. The AUD has been outperforming across the board as leveraged funds continue to add to their longs as further hikes are potentially priced in. On the day, the first support is back toward the 0.7010–0.7040 area, and the important 0.6950 area. The bulls will be looking for dips to remain supported in order to regain the momentum to rechallenge the pivotal 0.7100-0.7200 area.

- MNI - US January Labour Market Report. Monthly payroll growth is currently expected at 70k in January for a slight acceleration from the 50k in December and 56k in November. The market likely currently views that to be on the high side considering a swathe of soft labor indicators recently. We’ll finally see these annual benchmark revisions to the level of employment back in March 2025 with this release, with the preliminary estimate of -911k but -700-800k more likely in our view.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.7010(AUD560m). Upcoming Close Strikes : 0.6800(AUD1.55b Feb 13), 0.6850(AUD933m Feb 12) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 80 Points

- Data/Event: RBA Deputy Governor Andrew Hauser participates in a fireside chat in Sydney, Home Loans Value

Fig 1: AUD/USD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

US LABOR MARKET: A Heavy Layoff Month In A “Low Hire, Low Fire” Market

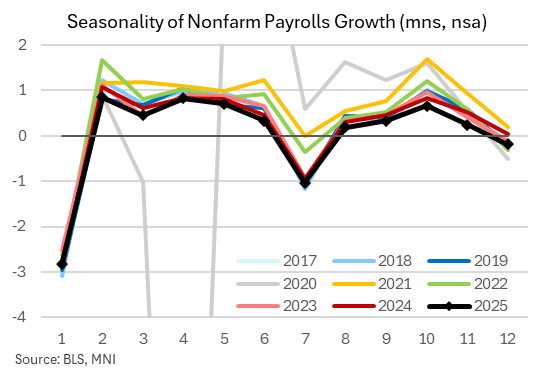

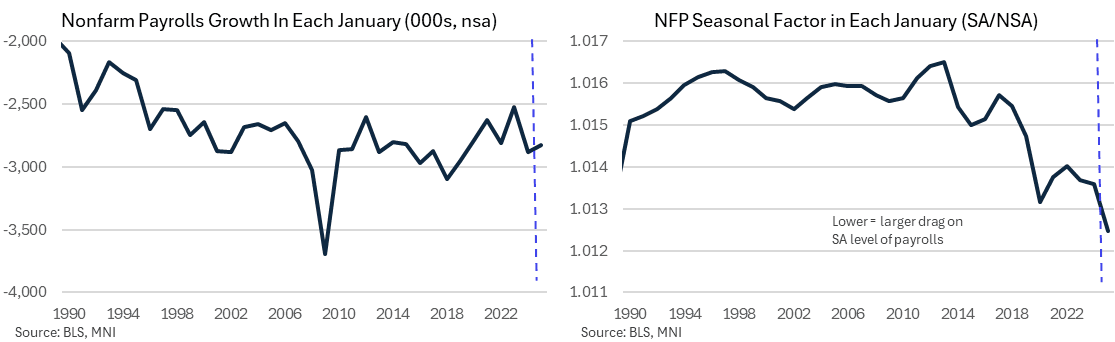

- Along with considerations needed to be made for annual benchmark revisions and a new birth/death model coming with Wednesday's NFP report, bear in mind that January's bring specific seasonal adjustment needs.

- January typically sees by far the most pronounced pattern of the year with large declines in the non-seasonally adjusted number of payrolls after the holidays. Indeed, payrolls fell by 2.8mln in Jan 2025 and 2.9mln in Jan 2024, both closer to the 2.94mln averaged in 2015-19 for a crude pre-pandemic trend after the 2.5mln in Jan 2023 (a period of particularly labor tightness), was its smallest decline since 1995.

- With the labor market softening but still seemingly in a “low fire, low hire” state, this month’s update could see fewer layoffs than would historically be the case although that’s increasingly being normalized by the growing weight on the post-pandemic sample.

- Going against this, seasonal factors have been increasingly penal for January readings in recent years, with the 2025 factors boosting the seasonally adjusted level of nonfarm payrolls by its least in at least thirty-five years.

- The past five years of seasonal factors will be revised with this release.

US PREVIEW: B/D Updates Also Set To Introduce Volatility (2/2)

The BLS’s analysis has suggested smaller forecast errors via the “real-time” estimates vs waiting for the large annual revisions.

- However, some analysts including Goldman Sachs have noted that this change could lead to greater month-to-month volatility in the Establishment Survey's payroll readings.

- For January, in which the seasonal adjustment plays a big factor (see our NFP preview), it’s possible that an unusual swing in birth-death adjustments in the new methodology could play an outsized factor (birth-death is reported non-seasonally-adjusted). A lower-than-usual birth-death figure under the new methodology vs what has historically been seen would likely mean a drastic undershoot vs consensus on January payrolls, for example.

- Analyst expectations for the Birth-Death adjustment are scarce, but BofA writes “Using real time survey signals as part of the new methodology should lower the Birth-Death model contribution to job gains, particularly in a cooling labor market. Hence, incorporating the difference from pre-pandemic levels, we estimate a 20-30k downward revision to monthly payroll growth starting April 2025 due to the updated Birth-Death model…If our estimate for the Birth-Death model-based revision is correct, payroll growth was likely running close to zero on average in the April-December 2025 period. In this period, the unemployment rate went up about two tenths. This is consistent with our lower breakeven job growth rate estimate of roughly 20k on account of tighter immigration policies implemented in 2025….if the Birth-Death model related revisions in the post April 2025 period are sizeable, this could generate a more significant market response.”