US CREDIT UPDATE: BDCs/Alt Finance: Week in Review

BDCs/Alt Finance: Week in Review #MNI #FINANCE * BDCs/Alt Finance underperformed the benchmark inde...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Dissent Fairly Contained; Powell Doesn't Push Back Much Vs Jan Cut (2/3)

Dissent Contained: While dissents to the rate decision had been anticipated (namely Gov Miran in favor of a 50bp cut), the Committee didn’t appear to any more divided than had been feared. Two regional presidents dissented in favor of a hold (KC’s Schmid again; in a modest surprise, the second was Chicago’s Goolsbee), but we’d seen some expectations that all four presidents could vote for a hold. And in the Dot Plot, the 12 (of 19) members putting in a 25bp cut was a fairly solid core.

- On a less dovish note, this meant there were 6 who filed a “shadow” dissent with rates unchanged at end-2025 – and those 4 outside of Schmid and Goolsbee probably include Logan, Hammack, and Kashkari – all 2026 voters. While that’s not really a surprise given inter-meeting comments, some of them may have pencilled in no change in rates through next year (3 dots at 3.9%), or perhaps somebody is eyeing a hike (though Powell said that wasn’t any participant’s base case).

Not Pushing Back Forcefully Against A January Cut: One of the key focuses of the meeting was how much Powell and the FOMC would lean against a January cut. If anything Powell was less cautionary about a follow-up cut than he sounded in October when he delivered an actual “hawkish cut”.

- Powell said "We're going to get a great deal of data between now and the January meeting, and I'm sure we'll talk more about that, and that will the data that we get are going to factor into our thinking.... We did some cutting, and then we paused for a while to work our way through what was happening in the middle of the year. And then we resumed cuts in September.... We're well positioned to wait and see how the economy evolves from here…. In terms of what it would take, we all have an outlook in terms of what is going to come, but I think ultimately having cut 75 [basis points], the effects of the 75 basis points will only begin to be coming in. As I said before a couple times, we are well positioned to wait to see how the economy evolves. We will have to see. We will get quite a bit of data."

- That broader guidance on being “well positioned” was repeated multiple times: "adjustments to our policy stance since September bring it within a range of possible, plausible estimates of neutral and leave us well positioned to determine the extent and timing of additional adjustments to our policy rate based on the incoming data, the evolving outlook and the balance of risks".

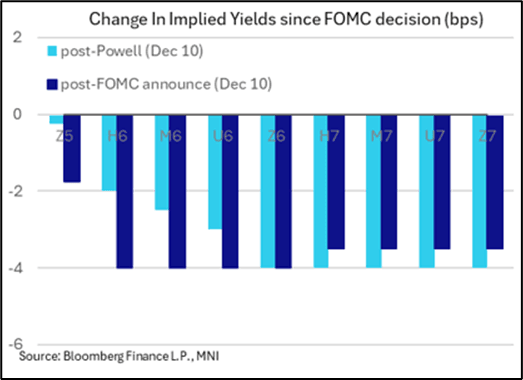

FED: December 2025 FOMC: Less Hawkish Than It Could Have Been (1/3)

The FOMC delivered what was widely anticipated to be a “hawkish cut” at the December meeting, lowering the Funds rate range by 25bp to 3.50%-3.75% while portraying a cautious stance on further adjustments in the Statement and Dot Plot. But with most of the main communications having been well-anticipated – from the subtle shift in forward guidance in the Statement, to the unchanged Dot Plot rate forecast medians – overall the meeting outcome brought some slight dovish surprises and a concomitant market reaction.

- Rates markets ended up pricing in two 25bp cuts thorough October 2026 a little more firmly (by about 2bp) than they did before the decision, though a January cut remains a longshot (about 25% implied probability before and after the meeting).

- Earlier we went through the composition of the Dot Plot (unchanged medians, including 1 cut in each of the next 2 years), the adjustments to the economic projections (slightly lower inflation profile through 2026), and the change in Statement language (eyeing the “extent and timing” of future adjustments) below – but none of these were at all surprising. In particular, the paucity of official economic data since the September projections made it unlikely that participants would have a radically changed view of the outlook, and so it proved in the SEP.

- That didn’t mean there weren’t some surprises, but these were marginally dovish leaning on net.

- We haven’t yet seen any analyst view changes following the meeting, though there’s probably not enough new information received that would change opinions on the rate trajectory.

Fed Front-Loads Reserve Management Purchases: In the biggest surprise, the Fed announced that it will buy $40B monthly in bills as part of reserve management purchases, starting on Friday. While Powell said that this decision had nothing to do with monetary policy, it was interpreted as a dovish development.

NZD: Breaks Above 0.5800 Pivot, Targeting 200-day EMA Resistance Above 0.5830

NZD/USD pushed through 0.5800 in Wednesday trade, as the Fed cut 25bps as expected, but wasn't as hawkish with its guidance as feared. The pair got to 0.5825, and we track slightly lower in early Thursday dealings, last near 0.5815/20. This is fresh highs back to the first half of Oct, having broken above the 0.5800 pivot point, only the 200-day EMA resistance remains on the topside, which comes in just above 0.5830. First half Oct highs were at 0.5845.

- Broader USD indices faltered in Wed trade (the BBDXY off around 0.45%, the DXY down 0.60%). NZD/USD was mid range from a G10 stand point, slightly outperforming AUD. US Tsy yields finished down across the benchmarks, led by the front end (2yr off 8bps to 3.54%).

- NZ-US yield differentials continue to track higher. The 2yr swap rate differential is to -47bps, highs last seen in early Sep and pointing to further NZD gains. Equity market gains were positive in US markets as well, adding to the risk on tone for the NZD (SPX +0.67%).

- Locally today we have Q3 manufacturing activity. There is no consensus expected, with the prior outcome at -2.9%q/q for volumes.