BRAZIL: BCB’s Galipolo Says Data Don’t Support Change In Policy Direction

Nov-27 19:41

- Speaking at an event in Sao Paulo earlier, BCB Governor Galipolo pushed back a little on expectations of an imminent interest rate cut following benign IPCA inflation figures, saying that he doesn’t see any data that promotes a change of direction. The central bank, he said, remains vigilant and cautious, according to headlines on Bloomberg.

- Galipolo said that the new data continue to show what is expected, that monetary policy is working, but very slowly. Activity remains resilient, he said, helped by the credit market.

- He also reiterated that the BCB would like for inflation to converge to the target at a faster pace, repeating that the policy rate will be kept at the necessary level for the necessary time to hit the inflation target.

- Amid ongoing uncertainty about the lagged effect of US tariffs, his comments suggest that he remains cautious on rate cut prospects for now, despite the recent return of inflation to the target range ceiling and in contrast to BCB Director David’s slightly softer tone this week. The next Copom meeting is on Dec 10, when a further rate hold is expected.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Light Bear Flattening On FOMC Eve

Oct-28 19:41

Treasury cash yields were little changed Tuesday, with anticipation building ahead of Wednesday's likely Fed cut and possible decision to end QT.

- Yields rose to session highs in early trade alongside a strong equity cash open (the S&P 500 rose to a fresh all-time high above 6,900 on tech strength), but soon faded to trade relatively flat on the session.

- A poor 7Y Note sale (0.8bp tail) ended the month's auction schedule on a sour note, but there was little broader market reaction.

- In data, Conference Board consumer confidence was mixed, with the headline index deteriorating less acutely than expected and the "labor differential" stabilizing after a multi-year low posted in the prior month - suggesting little additional urgency for the Fed to cut rates to buoy employment.

- On that front we also got a surprise announcement from ADP that they would henceforth produce a weekly private payrolls update, the first of which showed a solid-by-recent-standards 57k gain in the 4 weeks to Oct 11, potentially underpinning cautious sentiment in rates.

- The short-end underperformed overall in a slight bear flattening move, with Fed funds implied holding about 1.5bp higher on the session covering FOMC meetings through next June. This came as effective Fed funds ticked up another 1bp Monday, mitigating the signal derived from futures for actual rate moves.

- Cash levels in late afternoon NY trade: the 2-Yr yield is up 0.6bps at 3.488%, 5-Yr is up 0.2bps at 3.606%, 10-Yr is down 0.2bps at 3.9776%, and 30-Yr is down 0.5bps at 4.5474%. In futures, Dec 10-Yr (TY) up 1.5/32 at 113-15 (L: 113-9.5 / H: 113-18.5) amid solid though unremarkable volumes.

- The FOMC decision at 1400ET with Chair Powell press conference a half hour later is Wednesday's main event, though earlier in the session we will get weekly MBA mortgage applications and pending home sales data as well as the Bank of Canada decision (25bp cut expected).

- As noted in our preview, MNI's base case is for an immediate end to QT to be announced Wednesday alongside the well-priced 25bp rate cut. PDF here

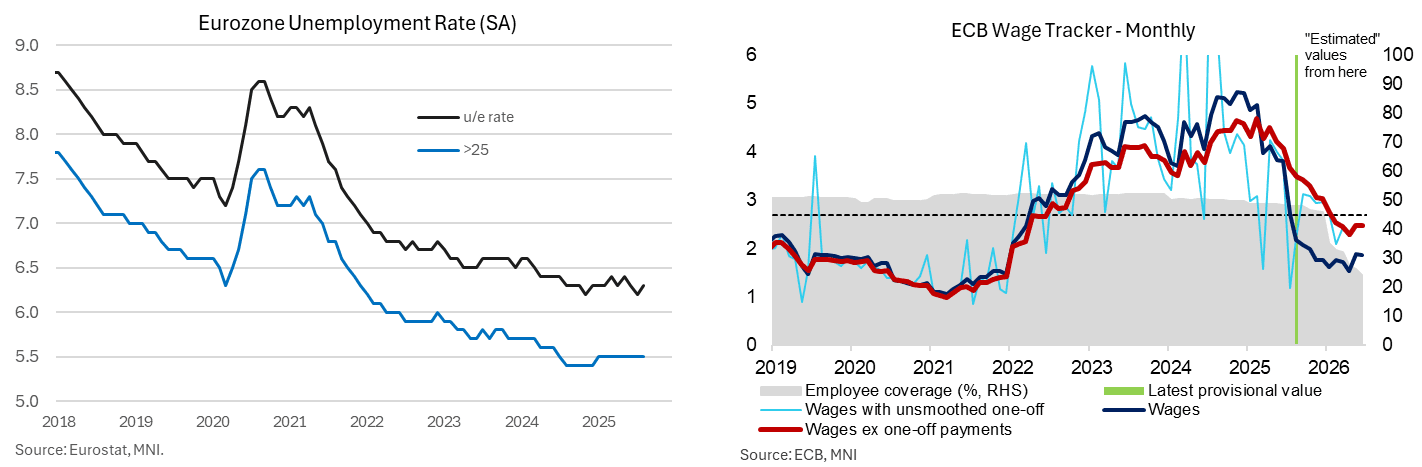

ECB: Macro Since Last ECB - Labour: U/E Rate Still Close To Lows, Wages Cooling

Oct-28 19:40

- The Eurozone unemployment rate surprised a tenth higher in August at a seasonally adjusted 6.3%, ticking up from an unrevised 6.2% in July. The lack of upward revision was of some note after regular upward revisions in recent months, leaving that 6.2% at joint historical low along with Nov 2024.

- As such, the unemployment rate continues to point to a historically tight labour market, and analysts expect more of the same in the September report released also on the day of this week’s ECB decision.

- Meanwhile, revisions to the ECB wage tracker, released as usual the Wednesday after the ECB decision, were immaterial relative to the July update. As is also typical, the ECB will have had access to this latest estimate with the September meeting but we include here with it being the ECB’s primary focal point for wages.

- The tracker excluding one-off payments (which is probably the best measure of underlying compensation pressures) was estimated at 2.58% in Q1 2026, down from 2.61% in July. The tracker now includes data up to Q2 2026, albeit with a low employee coverage, with wages excluding one-offs currently seen at 2.41% Y/Y for what would be modest additional moderation.

- As indicated by President Lagarde in the September press conference, the tracker continues to suggest that compensation pressures will ease in the coming years.

USDJPY TECHS: Key Resistance Remains Exposed

Oct-28 19:30

- RES 4: 155.55 2.00% retracement of the Jan 10 - Apr 22 bear leg

- RES 3: 154.39 76.4% retracement of the Jan 10 - Apr 22 bear leg

- RES 2: 153.82 1.618 proj of the Sep 17 - 26 - Oct 1 price swing

- RES 1: 153.27 High Oct 10 and the bull trigger

- PRICE: 152.16 @ 16:00 GMT Oct 28

- SUP 1: 151.76 Intraday low

- SUP 2: 151.09 20-day EMA

- SUP 3: 149.57 50-day EMA

- SUP 4: 149.05 Low Oct 6 and a gap high on the daily chart

A bull cycle USDJPY remains intact and short-term weakness is considered corrective. Attention is on key resistance at 153.27, the Oct 10 high and a bull trigger. Clearance of this hurdle would confirm a resumption of the medium-term uptrend. This would open 153.82, a Fibonacci projection. Note that MA studies are in a bull-mode position, highlighting a primary uptrend. First important support to watch lies at 151.09, the 20-day EMA.