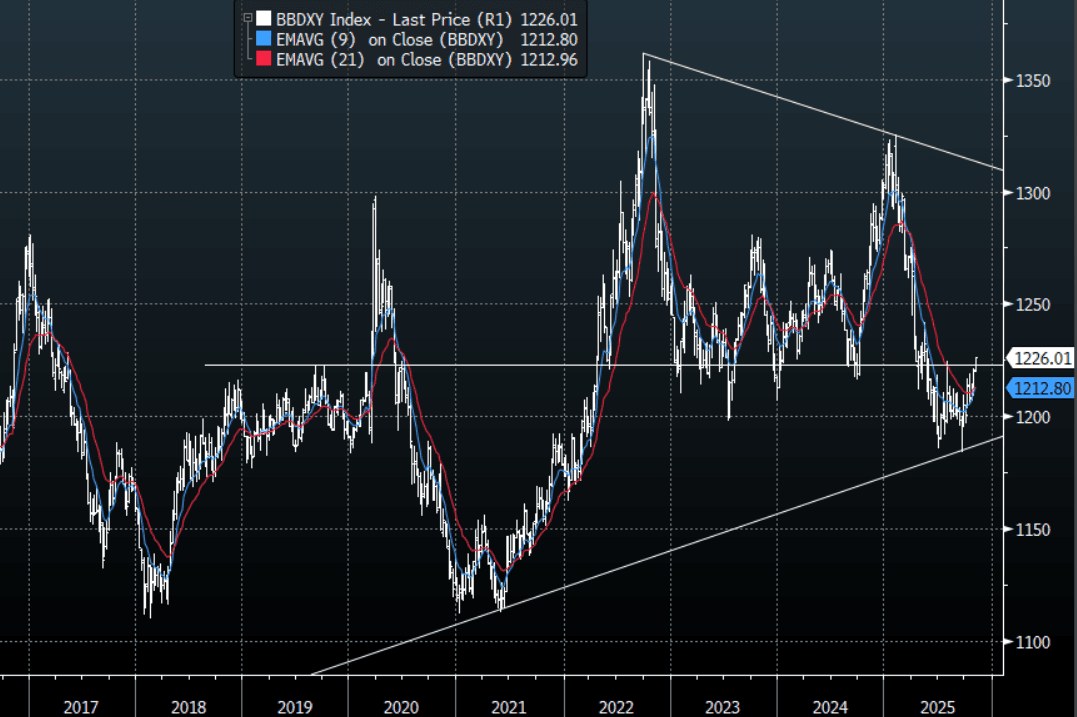

USD: BBDXY - Grinding Through Pivotal Resistance, Safe Haven Status Returns

The BBDXY range overnight was 1220.99 - 1226.13, Asia is currently trading around 1225, -0.02%. The USD continues to build on its recent gains eking out new highs every day, what stood out was with risk turning lower the USD gained some tailwinds as its status as a “safe haven” looks to have been reinstated. The 1230 area remains tough resistance, only a sustained close back above 1230 would start to challenge the conviction of the longer-term USD shorts. Risk/Reward does still favour fading this moving initially but the price action is starting to look more constructive as higher lows are being made and the dips remain very shallow pointing to a reduction in short positioning. A sustained move back above 1230 would potentially signal a medium term low is in place and a deeper pullback is on the cards.

- Robin Brooks wrote on X this pullback is linked to gold - “The Dollar today is at its strongest level since May and its rise is linked to the bursting of the gold bubble. Both things are driven by markets upgrading their assessment of the US economy. I forecast Dollar strength as a result of the gold unwind here.”

Fig 1: BBDXY Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: USD/JPY Marching Towards 150.00 Test, EUR/JPY To Record Highs

USD/JPY gains are the main focus point so far in Monday trade. We are close to late Sep highs near 150.00. A clean break higher would see attention shift to 150.92, the Aug 1 high. As we noted earlier, US-JP yield/swap rate differentials don't argue for a sustained move higher in USD/JPY beyond 150.00, but these spreads have moved in favor of the USD so far today. BoJ hike odds have fallen dramatically in the first part of trade, with a full hike not priced in until April next year. Oct hike odds are around 20%.

- The USD is ticking up against the rest of the G10, but moves are modest at his stage. EUR/USD is down 0.25%, but still above 1.1700. EUR/JPY is above 175.35 in latest dealings, fresh record highs.

- Focus for the EU session will be French President Macron's cabinet appointments, which largely saw continuity. French bond futures are weaker in the first part of trade.

- AUD/USD is under 0.6600, NZD, near 0.5825. Australian markets are largely out today due to a holiday.

- AUD/JPY is up to 98.75/80, fresh highs back to Jan of this year.

- The data calendar is very light today with only second tier Aust and NZ releases out a short while ago.

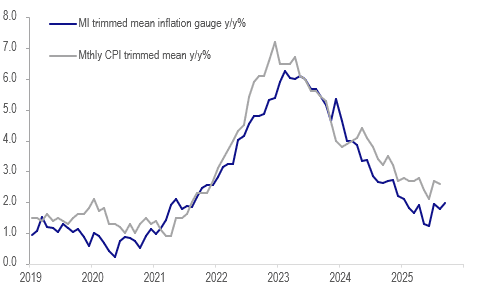

AUSTRALIA DATA: Data Continue To Signal Stall In Disinflation

The Melbourne Institute’s inflation gauge for September picked up 0.2pp to 3.0% with Q3 averaging 2.9% up slightly from Q2’s 2.8%. It also has a trimmed mean measure which also rose 0.2pp to 2% in September to be 1.9% in Q3 up from Q2’s 1.5% and may be trending higher again. Monthly CPI inflation is also higher over Q3 and RBA Governor Bullock sounded cautious last week as the central bank is concerned that there are signs a few key components are rising, especially market services which have also been sticky overseas. The key quarterly CPI data are released 29 October and are likely to determine the outcome of the 4 November RBA meeting.

Australia trimmed mean inflation y/y%

JGBS: Early Futures Spike Pared, 2/30s JGB Curve +14bps Steeper

JGB futures spiked higher at the open, getting to a high of 136.53, but we are back at 136.08, +.17 versus settlement levels in latest dealings. Markets are digesting Takaichi's surprise LDP leadership win from the weekend, with the spike being attributed to reduced BoJ tightening odds. Our bias is even with today's spike, the bear threat for JGB futures likely persists. Key short-term resistance has been defined at 137.30, the Sep 8 high. We ended last week at 135.93.

- The steepening bias is firmly intact. Front end JGB yields are down around 4bps for the 2yr, to 0.905%, while 3-7yr tenors are off around 2bps. The 10yr yield is up 1bps to 1.675%, while the 20-40yr tenors are up 7-10bps. The 2/10s curve is back to +77bp, +5bps stepper, the 2/30s curve is +236bps, +14bps steeper. Early Sep highs were at +245bps.

- Oct hike pricing for the BOJ has fallen back to an implied rate of around 0.53% (effective policy rate of 0.477%). We were at 0.62% at Friday's close. A full rate hike is not priced in until around the April 2026 meeting.