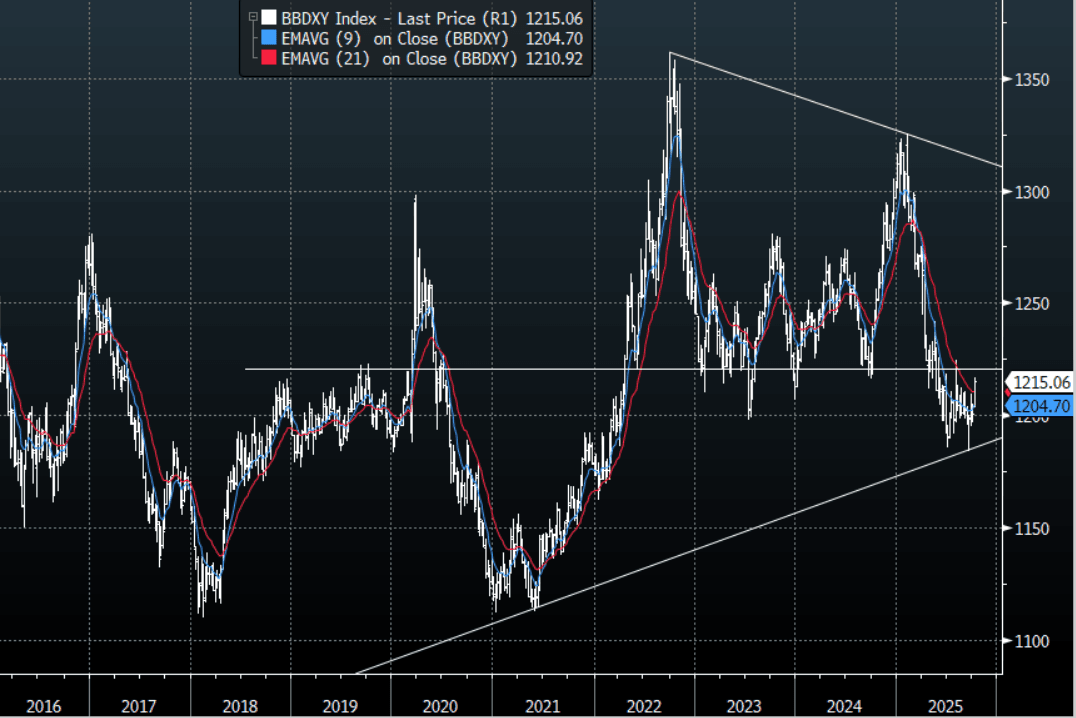

USD: BBDXY- Extends Higher As Correction Builds Momentum, Tough Resistance Ahead

The BBDXY range overnight was 1209.51 - 1216.78, Asia is currently trading around 1215, -0.10%. The USD extended higher and continues to build on its upward momentum overnight. The 1215-1225 area remains tough resistance, only a sustained close back above 1230 would start to challenge the conviction of the USD shorts. The weaker hands may be folding but I suspect we would need to do some work before the market can call a low for the USD as longer term accounts potentially look to fade this squeeze as they increase hedging ratios.

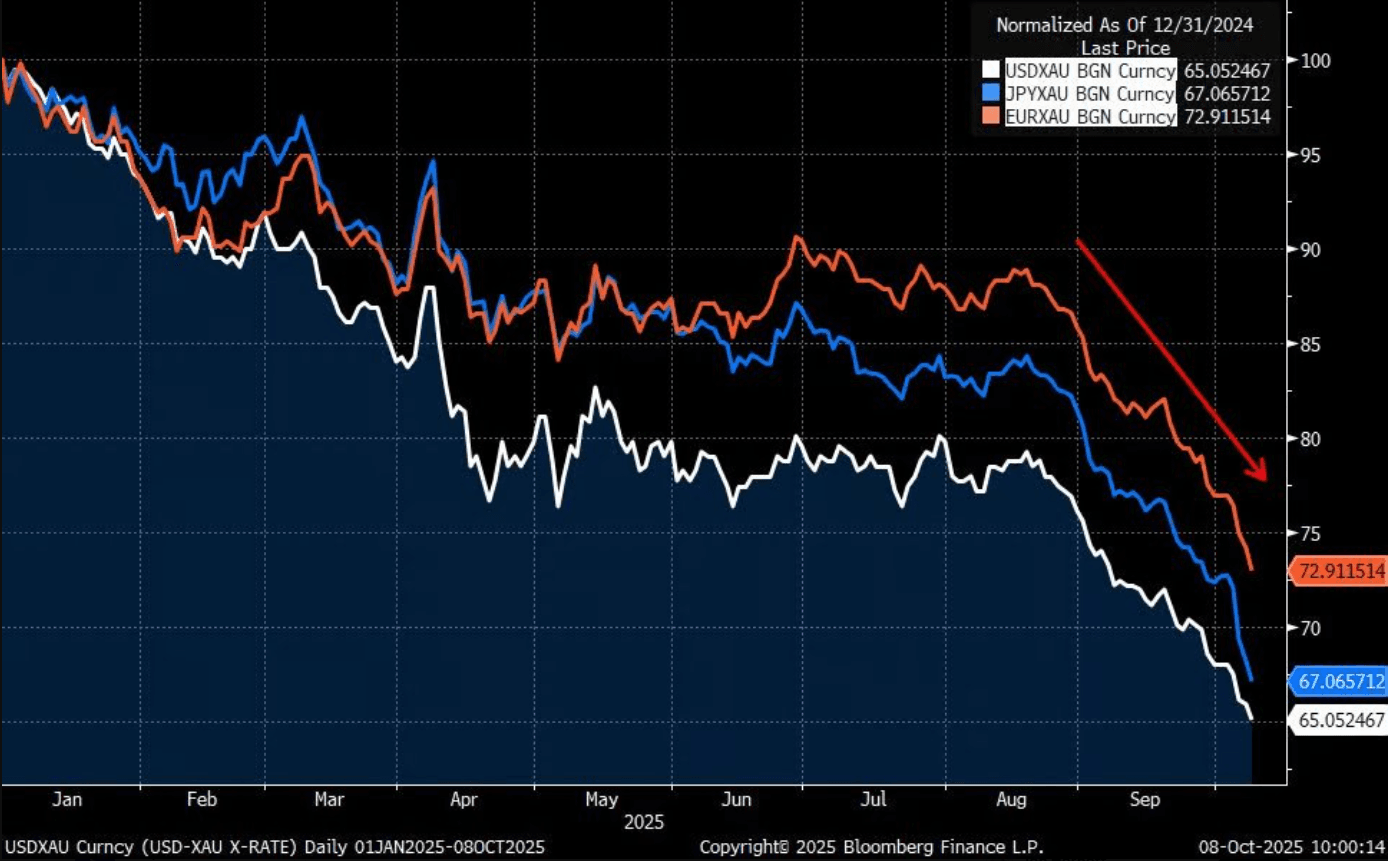

- It is not just the USD that has been sold but fiat currency as a whole as the noise around fiat debasement starts to grow louder.

- Daily Chartbook on X: “"Another way to visualize it: It's not 'dollar-debasement,' it's fiat debasement. And it has accelerated in September." - @f_wintersberger. See Fig 1 below.

Fig 1: Fiat vs Gold

Source: MNI - Market News/@dailychartbook/@f_wintersberger

Fig 2: BBDXY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JAPAN DATA: Rtrs Monthly Tankan At Multi Yr Highs, Official Q3 Print Due Oct 1

Headlines crossed earlier from Reuters from its monthly survey tracking the BoJ's quarterly Tankan survey - "Manufacturers' sentiment index +13 in September vs +9 in August" (Rtrs). It added, "...showed the manufacturers' mood index improved to 13 in September from 9 in August, marking a third month of increases and the highest reading since August 2022."

- "Multiple managers in the transport machinery sector said they were receiving solid orders, while some referred to stagnant domestic production in recent months given a shrinkage in exports" (via Rtrs). However, the report also noted more caution around the outlook, reflecting concerns on the domestic economic backdrop.

- The official Q3 Tankan report will be out on Oct 1 and will be a key watch point for the BoJ, as it looks to gauge fallout from the US-Japan trade deal.

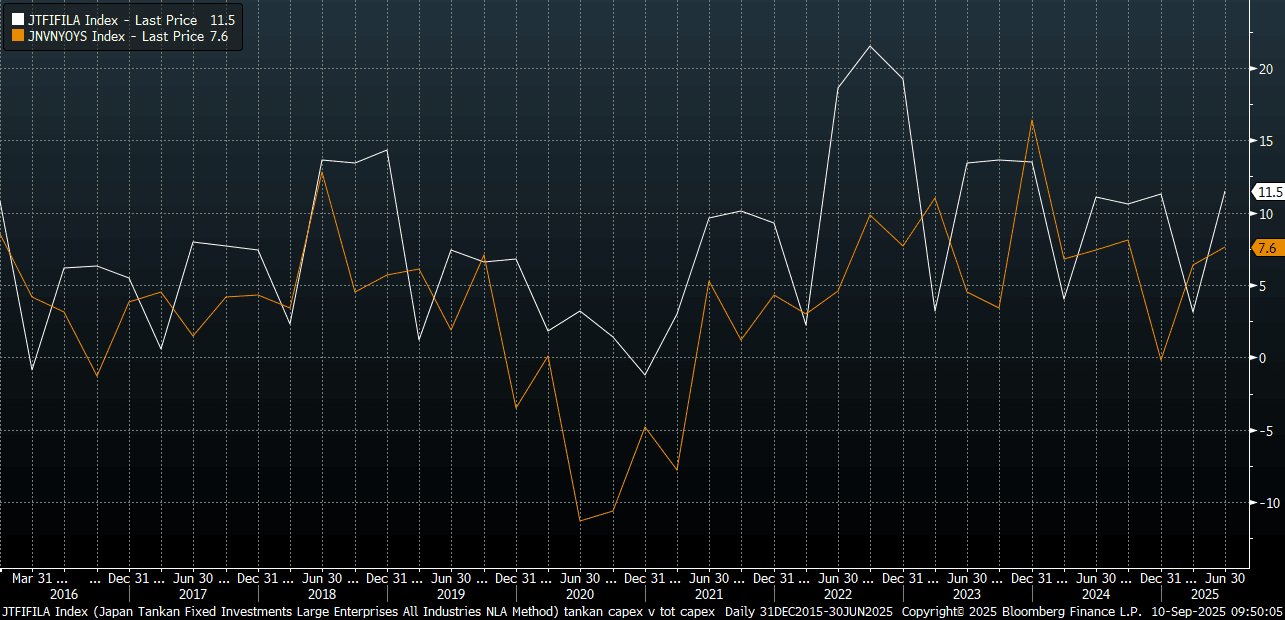

- The last Tankan survey for Q2 painted a resilient backdrop for large manufacturers, while the all industry capex estimate was also nudged higher. The chart below plots this capex estimate against total capex investment y/y.

- A resilient Q3 outcome could give the BoJ renewed confidence in the economic outlook and ring rate hikes back onto the agenda. We saw late yesterday some hawkish headlines via BBG, indicating there is a "chance of" a hike this year despite the political turmoil following PM Ishiba's resignation Sunday, which also weighed on USD/JPY (but follow through to the downside was limited). "Some officials are even of the view that a hike might be appropriate as early as October", the Bloomberg article added.

- Market pricing for a hike in Oct remains fairly modest at this stage though.

Fig 1: Tankan Capex Estimate & Capital Investment Y/Y

Source: Bloomberg Finance L.P/MNI

JGBS: Futures Back Under 138.00, 5yr Supply On Tap Today

JGB futures finished the post Tokyo close on Tuesday at 137.76, -.24 versus settlement levels. Some negative lead likely came from core markets elsewhere, with US Tsy futures weakening ahead of key inflation data (out later today and tomorrow).

- Also note some likely weight from news wires headlines. A set of hawkish comments from the BOJ, indicating there is a "chance of" a hike this year despite the political turmoil following PM Ishiba's resignation Sunday, which also weighed on USD/JPY (but follow through to the downside was limited). "Some officials are even of the view that a hike might be appropriate as early as October", the Bloomberg article added.

- Market pricing for a hike in Oct remains fairly modest at this stage (implied rate of around 0.57%, versus a current effective policy rate of 0.48%).

- For JGB futures, recent lows for futures rest close to 137.20, while recent highs were at 138.37. The general technical bias remains for a bearish threat for futures.

- In the cash JGB space, the 10yr yield finished up just above 1.57%, while the 30yr was near 3.27%. The 2/30s curve finished up around +243bps.

- The data calendar is empty today. Rtrs noted earlier: "Japanese manufacturers' sentiment was its best in more than three years in September, the Reuters Tankan poll showed, with trade uncertainties easing after Japan reached a tariff deal with the U.S. in July." The actual Q3 Tankan survey is released on Oct 1.

- We do have 5yr debt supply on tap today. The last 5yr debt auction had a bid to cover ratio sub 3.00.

AUSSIE BONDS: Futures Tick Lower, AU-US10yr Spread Still Elevated

Aussie bond futures are biased lower in the first part of Tuesday dealings. 10yr futures (XM) were off 3.5bps to 95.675, likewise for 3yr futures, last at 93.525. This follows the softer tone to US Tsy futures from Tuesday US trade, which has extended into early Wednesday Asia Pac dealings. US NFP revisions we weaker than forecast but we do have key inflation prints coming up.

- For Aussie futures we remain within recent ranges, but comfortably above earlier Sep lows.

- In the cash ACGB yield space we are close to 3bps firmer across the benchmarks, so lagging the US Tsy yield move from Tuesday. The 3yr benchmark was last at 3.45%, the 10yr close to 4.29%. The AU 3/10s curve was last around +84bps.

- The AU-US10yr spread is around +20bps, still elevated compared to 2025 averages.

- The local data calendar is empty today.