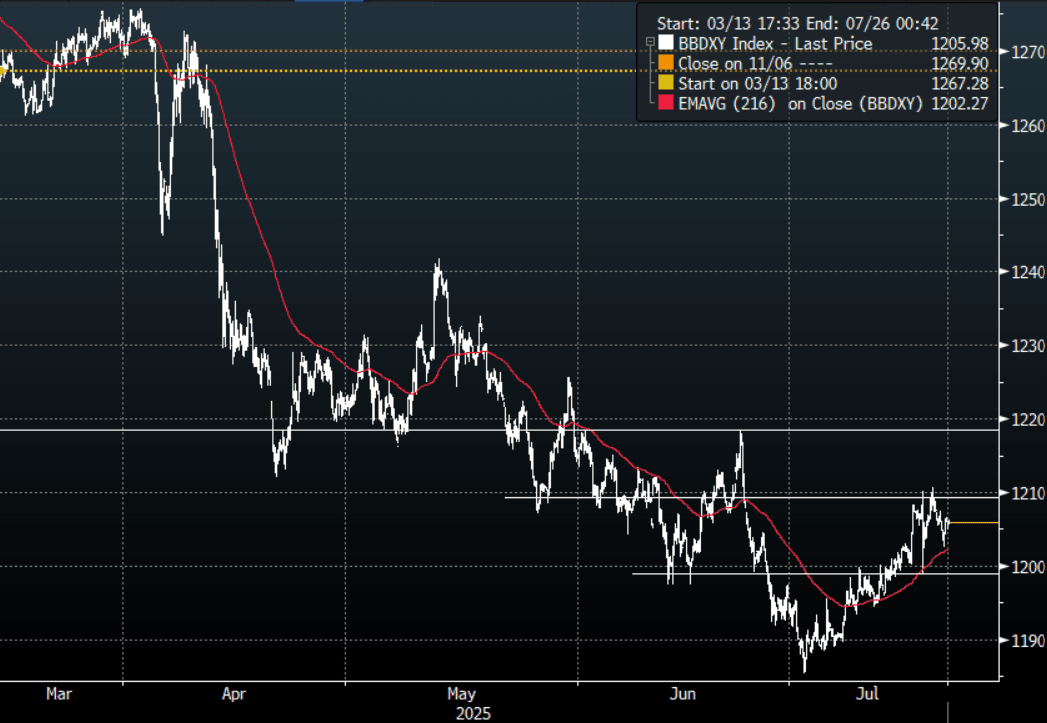

USD: BBDXY - Consolidates Recent Gains above 1200, Can It Actually Extend ?

The BBDXY range overnight was 1202.46 - 1207.37, Asia is currently trading around 1205. There were no signs of Powell being fired over the weekend and the USD sighs a breath of relief. Though President Trump's response to a WSJ article alluding to the fact it was Scott Bessent who laid out the case for why he should not oust Powell would leave the market feeling just as uneasy. It is starting to feel that without the headwinds from the rumours surrounding a Powell sacking, the USD could well have started some sort of a reversion back to the mean.

- Donald J Trump on Truth Social: “Nobody had to explain that to me. I know better than anybody what’s good for the market, and what's good for the U.S.A. If it weren’t for me, the market wouldn’t be at record highs right now, it would probably have crashed! So get your information correct. People don’t explain to me, I explain to them!”

- Robin Brooks on X: “The Dollar has now been essentially unchanged for 3 months. Nothing changes market narratives like price action (or lack of price action). Gone is all the talk about reserve currency status and sentiment has shifted to neutral from very negative just a few months ago...”

- There is a broad consensus that the USD is set to embark on a decent move lower as the world reduces its exposure to the US and repatriates a lot of these flows. This consensus will also result in some decent short squeezes as a lot of the market is positioned the same way.

- Data/Events : Leading Index

Fig 1: BBDXY Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Corrective Cycle

- RES 4: 1.4111 High Apr 4

- RES 3: 1.4016 High May 12 and 13 and a key resistance

- RES 2: 1.3832/1.3920 50-day EMA / High May 21

- RES 1: 1.3747 High Jun 19

- PRICE: 1.3733 @ 16:23 BST Jun 20

- SUP 1: 1.3540/3521 Low Jun 16 / 1.0% 10-dma envelope

- SUP 2: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 3: 1.3473 Low Oct 2 2024

- SUP 4: 1.3410 1.764 proj of the Feb 3 - 14 - Mar 4 price swing

The trend needle in USDCAD points south and this week’s recovery is considered corrective. Resistance at the 20-day EMA, at 1.3710, has been pierced. A continuation higher would signal scope for a stronger retracement and expose pivot resistance at the 50-day EMA, at 1.3832. For bears, a reversal lower and a resumption of the downtrend would pave the way for an extension towards 1.3521, envelope-based support.

LOOK AHEAD: Next Week's Key US Data Releases

US data is headlined by Thursday’s Q1 GDP revisions and Friday’s PCE report for May although there are plenty of other releases that will be watched with interest throughout the week.

- Q1 GDP data will be “stale”, especially being a third release, but it will nevertheless help the Fed assess whether its previous view on the economy is playing out. Recall that Powell at the May FOMC press conference said he expected consumption and inventories to have increased more strongly than first reported in the flash release. Last month’s second release showed that only partly played out, with inventories revised even higher but consumption revised down from 1.8% to 1.2%. Nevertheless, Powell at Wednesday’s June FOMC press conference still described the downward revised 2.5% for PDFP as “solid”.

- The May PCE report should be more impactful for clues on latest consumer momentum amidst strong income growth. Retail sales saw the largest monthly drop since March 2023 although the closely-watched control group was stronger than expected. As for inflation metrics, core PCE is seen around 0.15% M/M in May judging by unrounded estimates after the usual CPI, PPI and import price inputs, after 0.12% M/M in April.

- As for the other releases to watch, Monday’s preliminary June PMIs will give timely updates on wider activity after Empire and Philly Fed manufacturing surveys remained in contractionary territory. We also expect greater than usual focus on housing data (existing home sales Mon, new home sales Wed) after what have been some troubling releases across both construction and sentiment. Tuesday then sees the Conference Board consumer survey for an alternative look at the improvement since the de-escalation in trade policy before Wednesday’s advance trade data for the latest post tariff front-running update.

US TSYS: Tsys Narrow/Higher Range, Trump Been "Speaking to Iran"

- Treasuries look to finish higher Friday, top half of narrow range. Early risk-on tone followed unscheduled comments from Fed Governor Waller on the possibility of a rate cut in July and headlines that Iran was ready to discuss limitations on uranium enrichment plans.

- No market reaction to late Pres Trump comments to reporters & social media posts: "WILL MAKE TRADE DEAL WITH INDIA, PAKISTAN," "BEEN SPEAKING TO IRAN," "IRAN WANTS TO SPEAK TO US, NOT EUROPE" - Bbg posts. Trump adds Europe is not going to help with Iran, nor will China; Trump "might" support Israel/Iran ceasefire

- The price details of the Philly Fed manufacturing survey for June showed a pullback from elevated rates for both prices paid and prices received in the current period. Six-month ahead expectations for prices paid pushed higher again though, and at 68.9 is getting closer to the high of 77.8 from Jan 2022, although prices received isn’t quite as relatively elevated.

- Tsy Sep'25 10Y futures trades +5 at 110-30.5 vs. 111-03 high, remains below key resistance and its recent high of 111-14+, a Fibonacci retracement and the Jun 5 high. Clearance of this hurdle would be bullish and highlight a stronger reversal. This would open 111-30, a Fibonacci retracement.

- Curves steeper, 2s10s +2.611 at 47.137, 5s30s +3.530 at 93.143. 10Y yield at 4.3791% vs. 4.3593% low. Projected rate cut pricing back to 50bp by December.

- Cross asset: Stocks mixed (DJIA +29.34 at 42,202.0, SPX eminis -20.75 at 6013.5), Gold mildly lower at 3365.05, Bbg US$ index little firmer at 1210.80 +1.10.