EU BASIC INDUSTRIES: BASIC INDUSTRIES: Week in Review

Sep-20 11:17

- Bearish calls on iron ore from commodity analysts continue to flow through, with calls for $80-85 growing. Nonetheless, prices held above $90 again this week. BHP warned that AI growth will worsen the future shortfall for copper.

- Spinoffs continue to be a growing theme in the sector. SKF laid out plans to separate its Automotive and Industrial divisions. Little detail on capital structure was provided, but it said both will have “strong” balance sheets post separation.

- On that theme, BASF’s new CEO laid out a possible IPO of the Agricultural Chemicals division in 2026. That could take leverage meaningfully lower with strengthening the balance sheet mentioned, even if shareholder returns form part of the use of proceeds.

- Anglo American is progressing its coal assets sale. While the valuation has been impaired by the fire at the Grosvenor mine, credit won’t be impacted and continues to be driven by a takeover premium. Speculation continues that BHP will return after the shut-up ends in November.

- Knorr-Bremse is roadshowing for new 5Y and 8Y green bonds, a return to duration for the issuer. While it benefits from diversification, less cyclical aftermarket presence and a supportive rail market, margins are well below peak levels due to the slowdown in Chinese property development.

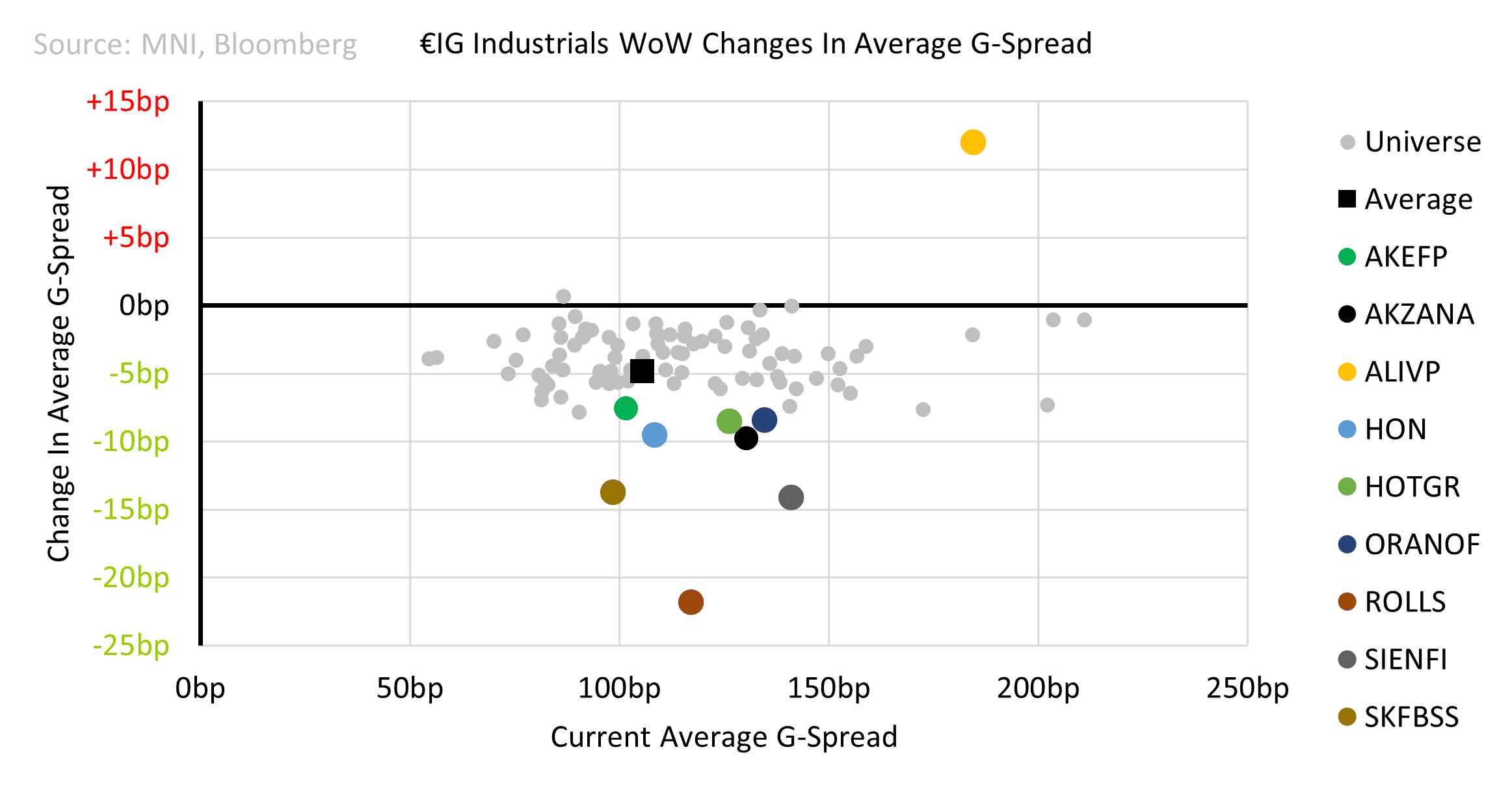

Spreads performed in-line with the index, with just Aliaxis (+12) wider for the week. Rolls-Royce (-22) put in a strong recovery, Siemens Energy (-14) was strong again and SKF (-14) reacted positively to the spinoff plan.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: Sep'24-Dec'24 Roll Update

Aug-21 11:18

Tsy quarterly futures roll from Sep'24 to Dec'24 rather muted at the moment. Percentage complete approximately 6% across the curve - a lot to go before next week's "First Notice" date on August 30. Current roll details:

- TUU4/TUZ4 appr 15,900 from -17.0 to -16.62, -16.88 last, 5% complete

- FVU4/FVZ4 appr 4,600 from -18.0 to -17.5, -17.75 last, 5% complete

- TYU4/TYZ4 appr 31,800 from -18.75 to -18.5, -18.75 last, 6% complete

- UXYU4/UXYZ4 appr 1,200 from -10.5 to -10.25, -10.5 last, 5% complete

- USU4/USZ4 3,300 from -6.25 to -6.0, -6.25 last, 6% complete

- WNU4/WNZ4 appr 1,200 from -1-03.25 to -1-02.5, -1-03 last, 8%

- Reminder, September futures won't expire until next month: 10s, 30s and Ultras on September 19, 2s and 5s on September 23. Sep options expire this Friday.

OUTLOOK: Price Signal Summary - Trend Structure In Bunds Remains Bullish

Aug-21 11:13

- In the FI space, a bullish trend condition in Bund futures remains intact and recent gains reinforce this theme. 133.21, the Jun 14 high, was cleared on Jul 29, confirming a resumption of the uptrend. A resumption of the trend would open 136.45, 76.4% of the Dec 27 - May 31 downleg (cont). The recent pullback has allowed an overbought condition to unwind. Support to watch is 134.02, the 20-day EMA.

- The trend condition in Gilt futures remains bullish and the latest pullback still appears to be a correction. Note that the move lower has allowed an overbought trend reading to unwind. A resumption of bullish price action would signal scope for a climb towards 101.78, the 2.236 projection of the May 29 - Jun 4 - 10 price swing. Initial key support lies at 99.54, the 20-day EMA. First resistance is at 100.80, the Aug 14 high.

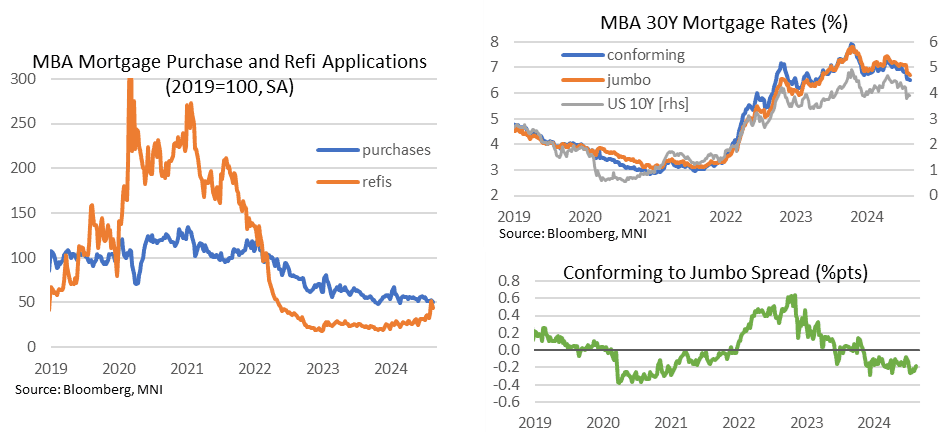

US DATA: Purchase Applications Shrug Off Mortgage Rate Declines

Aug-21 11:09

- MBA composite mortgage applications unsurprisingly pulled back with a seasonally adjusted 10.1% decline in the week to Aug 16, payback after jumping 16.8% the week prior.

- Refis drove the move with -15.2%, but two strong increases including a 34.5% surge the week prior leaves refi applications more than 30% higher since the end of July.

- Purchases also saw a notable decline (-5.2% after 2.8%) for the sharpest weekly decline since February.

- Whilst refi applications have seen a sizeable boost from the >50bp decline in mortgage rates (30Y down another 4bps to 6.50% for its lowest since May 2023), purchase applications have shown no sign of uplift.