EU CONSUMER STAPLES: Barry Callebaut; 3Q (to May) results (x3)

(BARY; Baa3 Neg/BBB- Neg) (equities -13%)

On Financials:

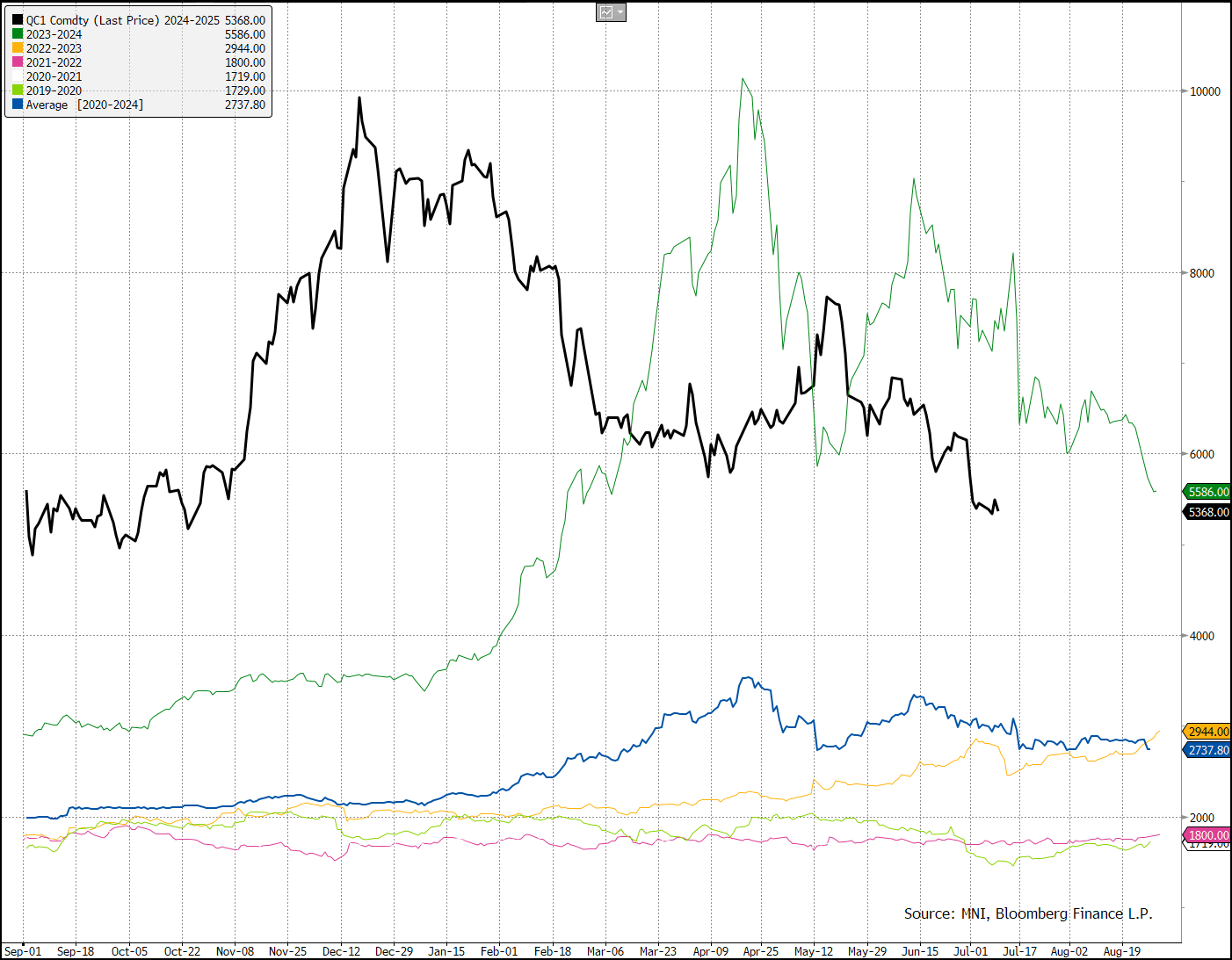

- Cocoa prices have increased +43% YTD -> when it says this it means for the FY beginning in September - most of this increase was in 6m to Feb/1H. Now it is flat to last year's levels (see below).

- Revenue has increased +57% to match this + some more pricing to offset other costs (like increased interest costs)

- Volumes have meanwhile fallen -6.3%. In 3Q specifically (3m to May) volume was -9.5%. The deceleration is somewhat expected - there is a 6-9m lag from spot prices reaching shelf pricing.

There are a few cuts to guidance:

- FY (to August '25) volume expected to be down -7% (prev. mid-single-digit).

- FY adj. EBIT to grow mid to high single digits (prev. double digit growth)

- Interest costs (below EBIT) are now expected to be above CHF 350m (prev. 350m) (last year CHF 207m)

- Net, this is still expected to leave Net Profit "significantly better" in H2 vs. 1H (when it reported adj. CHF 64m) - but will still be negative y/y (both for H2 and FY).

There were some positive remarks made on the balance sheet:

- Liquidity is ample and "I'm not anticipating that we need to raise more over the next month or even year".

- This is in-line with our expectation - if Cocoa prices hold even flat y/y, the WC outflow/drag will stop.

- It is looking at reducing WC cycle (currently has 12-18m between Cocoa contract/purchase & customer sales).

- It is looking at less cash intensive methods of financing including financing against inventory

- Still targeting net leverage of 3.5x (last reported 6.5x)

It played down impact of tariffs despite 3Q weakness in the US (US is 16% of group revenues):

- "we are actually very local with our business. We have operations in the U.S. We have operations in Canada. We have operations in Mexico. So, we can actually pivot to actually navigate this environment in the right way."

On Rating Action:

- On above revised guidance we see net leverage ending the year at 7.5x, ICR at 1.5x, and FCF coming in still around -€2b (on a WC swing).

- These are HY metrics -> rating agencies are being lenient as they understand this is structural and will reverse if Cocoa falls.

- As Cocoa is holding flat for now, WC swing will reverse to only flat (not positive) -> the higher debt level/leverage will remain till it actively reduces it (e.g. using regular operating cash flows).

- We think the rating agencies should view the higher debt level in the interim and increased risk to on any operating weakness as more in-line with HY ratings. It is hard to call for downgrades with certainty though - both agencies have given Barry a long runway to get back into rating thresholds.

We will follow up separately on bond levels.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: Large EU Basic Resources Put Spread

Large long dated Basic resource Option ratio Put spread:

- SXPP (21/12/29) 450/300ps 1x1.5, bought for 35.1 in 13.5k (13.5k x 20.25k).

BTP: Block trades

BTP Block trades, suggest sellers:

- IKU5 ~1.72k at 121.23 and ~1.4k at 121.19.

GILT TECHS: (U5) Bull Cycle Extension

- RES 4: 93.26 1.500 proj of the May 22 - 27 - 29 price swing

- RES 3: 93.05 1.382 proj of the May 22 - 27 - 29 price swing

- RES 2: 93.00 Round number resistance

- RES 1: 92.87 Intraday high

- PRICE: 92.83 @ Close Jun 10

- SUP 1: 92.33/91.56 Intraday low / Low Jun 9

- SUP 2: 91.16/90.59 Low Jun 2 / Low May 29

- SUP 3: 90.11 Low May 22 and the bear trigger

- SUP 4: 90.00 Round number support

Gilt futures have resumed their short-term uptrend and this strengthens the current bullish theme, marking an extension of the breach of resistance at 91.87, the May 20 high. The climb signals scope for a continuation higher and sights are on the 93.00 handle next. Initial firm support to watch lies at 91.56, the Jun 9 low. A clear break of this level is required to signal a possible reversal.