EM CEEMEA CREDIT: Bank Muscat SAOG: 9M Earnings Prelim. Neutral take

(BKMBOM; Baa3/BBB-/BB+pos)

#MNI #Banks #EM #GCC

• Oman’s Bank Muscat posted prelim. 9M results: solid read, credit neutral. Full results due out following board approval later in the month. In secondary markets, recently launched BKMBOM 4.8 Oct30 chart at z+155bp, near the local highs.

• NII&F +5.9% y/y at OMR310.90mn, boosted by stronger +12.0% y/y Other Income at OMR123.57mn. Op. Profit +8.8% at OMR271.65mn on contained expenses +5.3% y/y, leaves Net Profit +12.2% y/y.

• Asset growth looks adequate, Total Assets +3.6% y/y at OMR14.5bn, sequentially consistent quarterly growth with lending sustained by deposits (LtD 104.7% YE24). Marginally lower y/y Impairments at OMR43.63mn. NPL ratio has been showing stable quarterly evolution in recent years (was 3.67% as of Q2).

• Ratings reflect a low triple-B stance at both Moody’s and S&P. Fitch’s cites better than peer profitability and asset quality, with BB+ ratings on positive outlook.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR OPTIONS: Call Spread vs Put Spread

SFRV5 96.43/96.62cs vs 96.25/96.12ps, bought the cs for 1 in 4k.

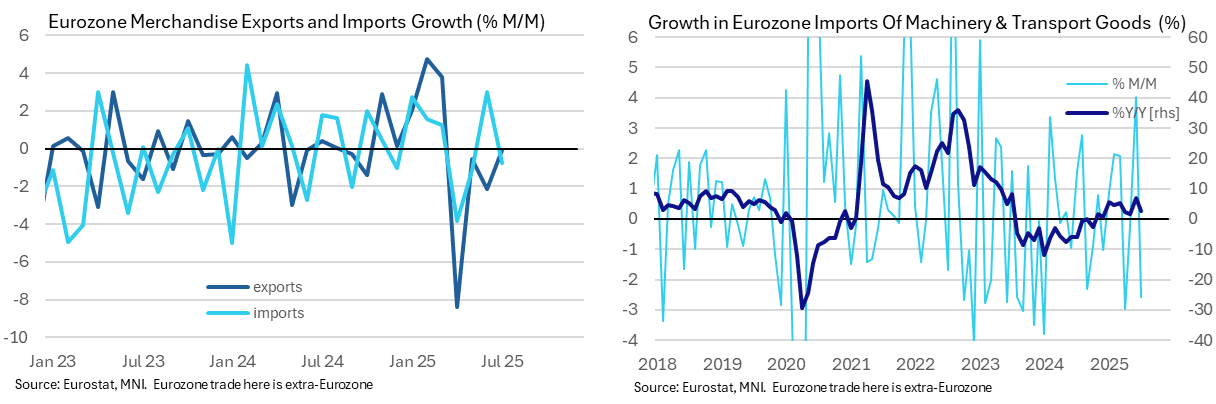

EUROZONE DATA: Soft Imports Take Some Of The Edge Off A Solid June [2/2]

- The modest widening in the surplus came as imports (-0.8% M/M) fell by more than exports (-0.1% M/M).

- It sees imports unwind part of the 3.0% M/M increase in June in what was a rare solid reading compared to recent months.

- An important caveat when it comes to digging into import details for domestic demand implications -- the miscellaneous category again shows a surge but this was revised away last month as these unclassified items are eventually correctly allocated.

- Specifically, the miscellaneous category surged 172% from to E6.8bn in Aug from a typical E2.5bn in July, with the latter initially reported at E7.1bn.

- With that in mind, monthly declines are currently seen as being led by the typically volatile raw materials category (-7.5% M/M) along with manufactured goods (-2.8%) and food, drinks & tobacco (-1.8%).

- We tend to focus on machinery & transport within manufactured goods, and this currently shows a disappointing -2.6% M/M to undo a sizeable part of June’s 4.0% increase. In doing so, it crimped annual growth in this nominal category to just 2.5% Y/Y.

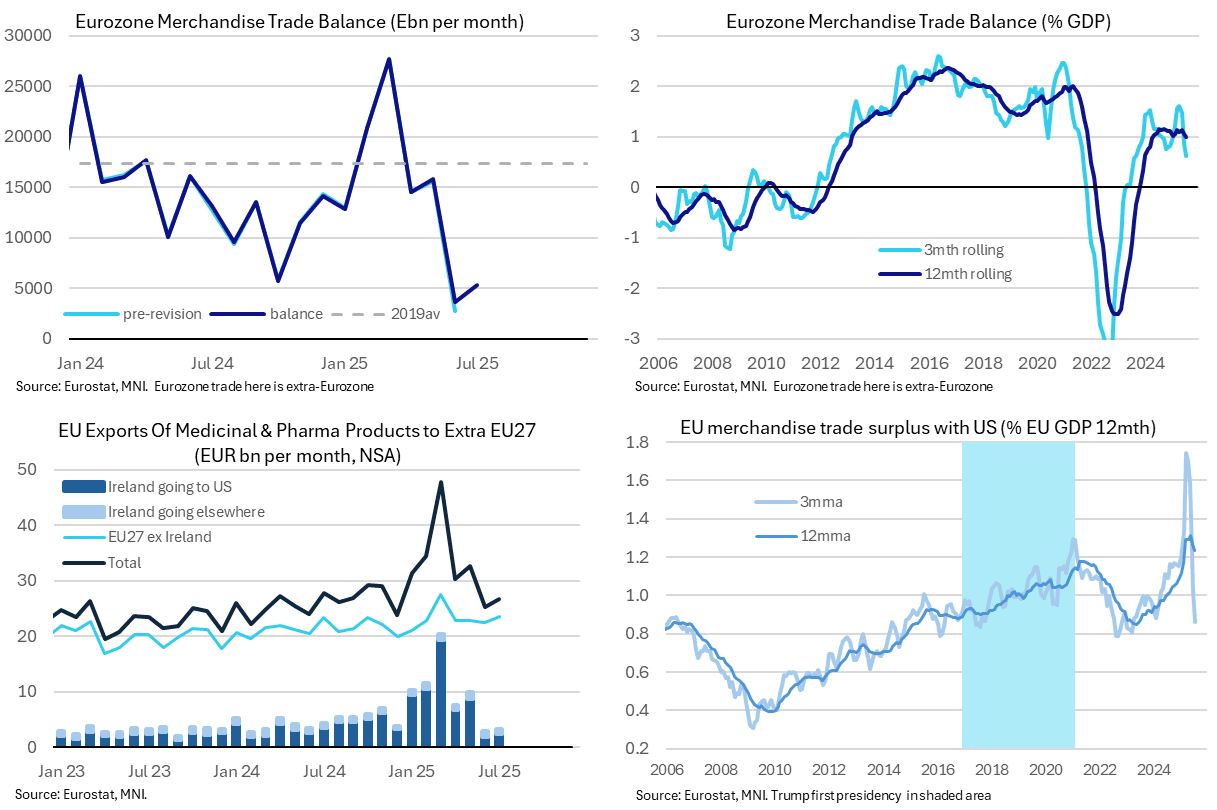

EUROZONE DATA: Trade Data See Further Post Tariff Front-Running Adjustment [1/2]

- The Euro area goods trade surplus surprised lower for the third time in four months, with a seasonally adjusted E5.3bn in July (cons E12.0bn expected) after an upward revised but still low E3.7bn (initial E2.8bn) in June.

- The Bloomberg consensus figure again consisted of only three responses, so we wouldn’t put too much weight on the surprise and instead focus on the direction.

- The trend is one of clear narrowing in surpluses, with an average E4.5bn in Jun/Jul, E15.2bn in Apr/May and E24.3bn in Feb/Mar on peak tariff front-running. For a sense of a more ‘typical’ surplus, it averaged E14.1bn per month through 2024.

- Alternatively, it leaves the latest three-month goods surplus worth approximately 0.6% GDP vs a peak of 1.6% GDP in the spring after an average surplus of 1.1% GDP through 2024.

- The more detailed NSA data show that Irish pharmaceutical exports to the US registered a second small month of E2.4bn after just E1.8bn in June. It's continued payback from a surge in Q1 when exports summed to E39bln vs the E44bln through 2024 as a whole. As such, it may not necessarily be surprising but it's still notable and could see similarly small readings ahead with Jan-Jul exports already worth a cumulative E58.7bn.