EU CONSUMER STAPLES: B&M; 4Q (3m to March) trading update

(BMELN; Ba1 Stable/BB+ Neg) (equities +5.5%)

3m to march saw;

- UK LFL sales fall -2.4%. Net of store openings sales +5.4%

- general merch increased on volumes and values giving LFL growth. It was offset by FMCG falls. It

has said in the past it is ~half/half split between the two.

- general merch increased on volumes and values giving LFL growth. It was offset by FMCG falls. It

- France LFL sales +3.2% and net of store openings +9.1%

- France smaller ~10% of group sales

That left FY revenue at £5.6b (net +4%) with UK LFL -3.1% and France LFL +2.6%

- Margins - no values given but gross described as "robust in UK". UK operating costs increased +6% which will include impact of store openings

- FY25 pre-IFRS EBITDA expected to be above recently lowered guidance of £605-625m (i.e. implies £615-625m vs. £629m last year)

- Add back circa +£250m for lease expenses for statutory EBITDA

- After dividend payments, leverage expected to be mid-point of pre-IFRS net 1.0x-1.5x target

- vs. 1.2x last year is unch and in line with what we expected (eqv. n/g 2.8x/3.0x)

- Store opening guidance is unch for 45 in UK this year (same as last year).

- CEO search underway and expected to be announced in "coming weeks".

- More complete FY pre-lim results will come 4th June.

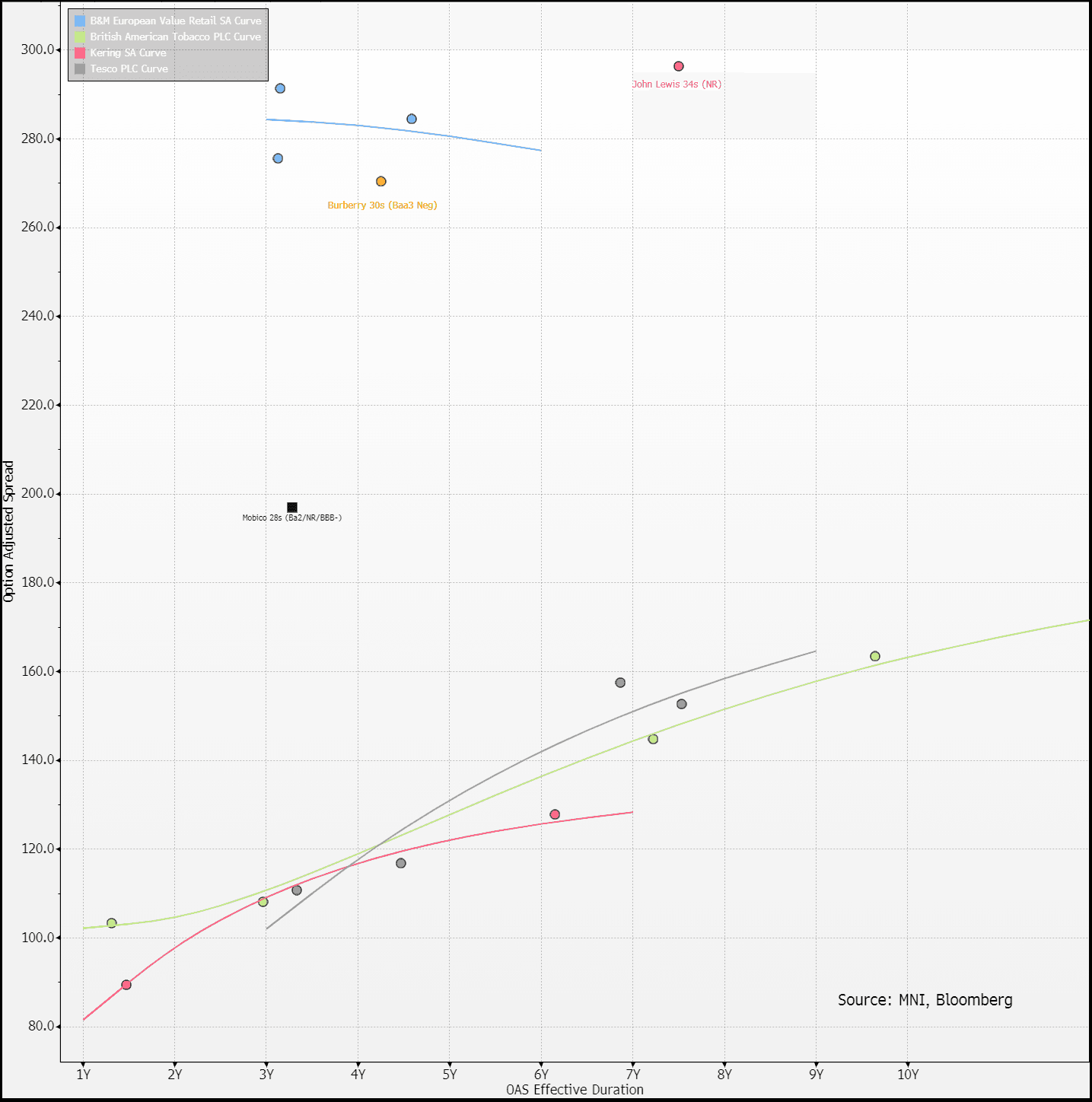

On RV; Burberry vs. B&M remains a tough call and today’s update doesn’t materially shift the needle. In a cyclical downturn, B&M 'should' be better positioned defensively. That said, if Burberry can replicate last quarter’s performance (earnings due 14 May), it will outperform.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: March Economic Projections: Higher Inflation, Weaker Growth, Same Rates

The MNI Markets Team’s expectations for the updated Economic Projections in the March SEP are below.

- The unemployment rate is likely to rise slightly for 2025 alongside a downgrade in GDP growth, while the 2025 core and headline PCE inflation projections are set to rise again. Changes to later years will likely be limited, however.

- More detail on the shift in Fed funds rate medians is in our meeting preview - we will add more color next week.

FED: Market Pricing Nearly 3 2025 Cuts As Conditions Tighten

Amid rising government policy uncertainty, sentiment among businesses and consumers has fallen sharply since the start of the year, while equities and the dollar have reversed their post-election rise. Overall, financial conditions have tightened, even if stress is not yet mounting, e.g. no major widening of credit spreads (the accompanying chart shows the Fed’s financial conditions impulse index but only through January).

- Combined with growth fears, this has affected expectations for the Fed’s rate path, with around 18bp more cuts expected in 2025 compared with what was seen after the January FOMC. 65bp of cuts are priced for the year as a whole. 2025 cut pricing reached 71bp before the February inflation data and 76bp before the February payrolls report.

- A rate cut is seen with near zero probability for March’s meeting, but the first full cut is just about priced for June, with a second nearly priced by September.

- Chair Powell has no reason to endorse or refute these expectations – he’s likely to be happy with a press conference that ends with little discernable change in pricing.

CANADA'S CARNEY ANNOUNCES ELIMINATION OF THE CONSUMER CARBON TAX

- CANADA'S CARNEY ANNOUNCES ELIMINATION OF THE CONSUMER CARBON TAX