EM LATAM CREDIT: Banco de Credito del Peru: Mandate Investor Calls

(BCP; Baa1/BBB-/BBB)

IPTs 11.25NC6Y: N/A

FV 11.25NC6Y: 5.65%

• Peru’s largest bank BCP mandated investor calls followed by likely issuance of USD benchmark-size, 144a/Reg S, 11.25NC6-year Tier 2 notes rated Baa2/NR/BB+. We estimate fair value at 5.65% and a new issue concession of 10bp to expect 5.75% area guidance.

• BCP 6.45% 35s callable April 2030 were quoted at a 5.36% YTC, g-spread of 167bp and the BCP 5.8% 2035 were quoted 5.31%. The Treasury curve pickup from Apr. 2030 to Oct. 2031 is 14bp which equates to a FV of 5.5% then add 5bp credit spread for the longer maturity. We further account for the differences in coupon step-up provisions that influence the likelihood of the bonds being called, worth 10bp.

• The step-up coupon spread on the 6.45% 2035 is 248.6bp while the step up spread on Tier 2 5.85% 2035 is 224bp. The call dates are only one month apart so the yield differential of 5bp can be attributed to the difference in coupon step up. If the new issue coupon step up spread will be about T+205bp (assuming a 5.75% 6-year BCP note priced off the 5-year Treasury) that is nearly 50bp lower than the 6.45s, which we estimate to be worth about 10bp.

• Spain based BBVA’s substantial Mexican subsidiary BBVA Mexico (Baa1neg/BBB/BBB*+) implied subordination value was quoted 139bp going from Sept. 2029 senior debt at a g-spread of 73bp to BBVA Tier 2 notes maturing 2034 callable Sept 2029 at a g-spread of 212bp.

• BCP has Jan. 2029 senior debt quoted at a g-spread of 62bp. Applying the subordination premium that we observe in BBVA bonds would imply a BCP Tier 2 spread of 201bp for a roughly 3-year note. At 5.75% for a BCP 6-year note, that is a spread to comparable maturity Treasuries of 194bp.

• Investors accept a lower subordination premium for BCP relative to BBVA Mexico notes despite the substantially similar ratings. Note also that the yield spread between BBVA Mex Aug. 2029 senior notes and BCP Jan 2029 senior notes is quoted only 13bp apart which maturity adjusted is almost the same. The yield spread between BBVASM 7.625% 2035 Tier 2 notes and BCP 6.45% 2035 Tier 2 notes averaged 95bp over the past six months.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: US Macro: PPI (Wed) and CPI (Thu) Inflation

US PPI inflation is released on Wednesday before CPI inflation on Thursday, an unusual ordering that should see core PCE implications dialled in after the CPI release rather than the usual wide range waiting for specific PPI details. PPI will be watched more closely than usual this month after a far stronger than expected jump in last month’s July report fired a warning short over tariff-based cost pressures starting to feed through. That included a 0.6% M/M increase in our preferred core series of PPI ex food, energy & trade services, which strips out items such as the then booming portfolio management & investment advice category following the strength in equity markets. It's too early to gauge an accurate sense of analyst expectations for August.

CPI inflation on Thursday will then be the last major release ahead of the Sep 17 FOMC decision. Consensus looks for core CPI at 0.3% M/M after the 0.32% M/M in July, another monthly increase comfortably above a pace consistent with 2% inflation. August should in theory start to see the largest tariff impacts along with September and possibly October. Returning to July’s report, core goods inflation was softer than expected, at a still solid (by core goods standards) 0.2% M/M for a second month running but about half that of 0.4% expected by analysts. Instead, non-housing core services surprised higher. The latter was a “dangerous” development in the words of a usually dovish Chicago Fed’s Goolsbee (’25 voter), who speaking after Friday’s payrolls report is still undecided on a September cut whilst looking for August inflation data “to get more information”.

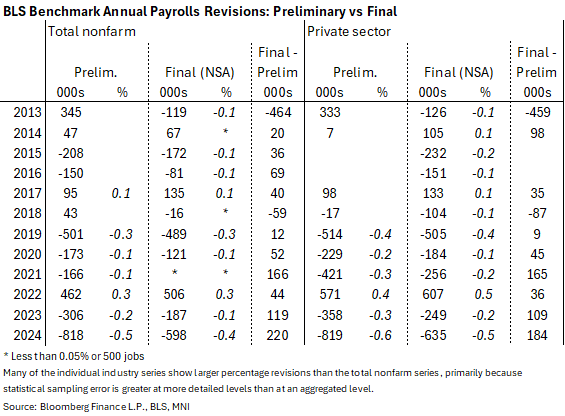

LOOK AHEAD: US Macro: Payrolls Preliminary Benchmark Revisions (Tue)

- The BLS on Tuesday will publish preliminary estimates of benchmark revisions, based off QCEW data for Q1.

- These will give an indication of the actual benchmark revisions on the Mar 2025 level of payrolls due with the Jan 2026 payrolls report released in early February.

- Bear in mind that the final benchmark estimate tends to nearly always be more negative than the preliminary figure – see historical values to the right.

- That doesn’t mean they can’t be large again after last year’s historically negative revision that lowered the level of payrolls by ~600k. Initial estimates we’ve seen look for another large downward revision, with the smallest being worth -550k but with wide ranges higher.

FED: Barclays Adds A Cut To 2025 Fed View

Barclays analysts now expect three Fed cuts in the remainder of the year, adding October to their pre-existing call for 25bp reductions in September and December. "Given the disappointing August employment report, we expect the FOMC to see more elevated downside risks to the employment side of the mandate."

- As for a 50bp September cut, "we think that the FOMC will view [that] as sending too strong a signal that labor market conditions are deteriorating. Indeed, we think that participants such as Powell understand that the slower pace of payroll employment reflects at least, in part, slower labor supply, which does not translate into increased labor market slack."

- For 2026 they continue to expect 25bp cuts in March and June to 3.00-3.25%, but "we do not think the FOMC will be able to cut rates more than twice next year, as we think that activity will show some slight acceleration, with the economy adapting to the new tariff environment and fiscal policy providing some support, and the unemployment rate will revert down amid limited increase in labor supply."