BOE: Balance Sheet Size Falls; But Set to Pick Up Again Next Week

Oct-30 15:11

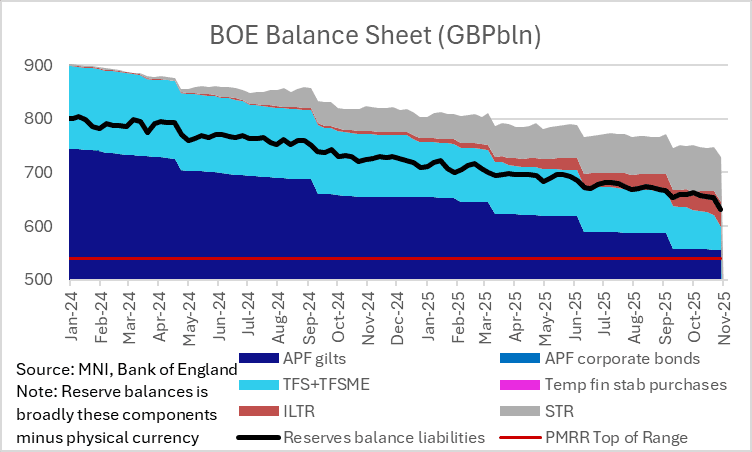

- Reserve balances at the BOE have fell notably to GBP630.2bln as of 29 October - a GBP23.3bln reduction from the prior week (22 October).

- This was almost entirely driven by the GBP22.8bln reduction in TFSME balances to GBP41.9bln (which is very close to the GBP40bln level expected by the end of October).

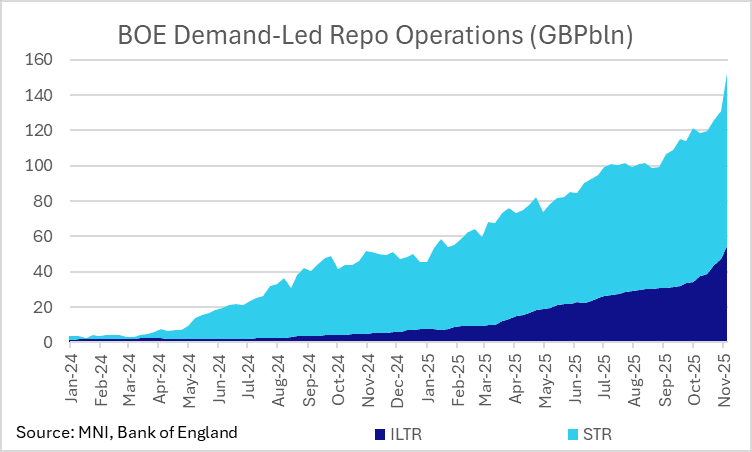

- Note that due to T+2 settlement the large increases seen in this week's repo operations will not be reflected on the balance sheet until next week. As a recap between them these operations increased by a combined net GBP21.4bln this week.

- So there is a large reduction in the size of the Bank's balance sheet - but it is almost guaranteed that it will rebound again next week - with the non-repo led operations likely to only see small changes and the vast majority of the near-term TFSME repayments having already happened.

- We may see a bit of volatility in the upcoming repo operation sizes but overall our analysis from earlier - that the overall size of the balance sheet is likely to be broadly unchanged - continues to stand and we see this reduction in balance sheet size as a blip rather than a meaningful reduction.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS/SUPPLY: Treasury Ups Bill Sizes To New Records

Sep-30 15:11

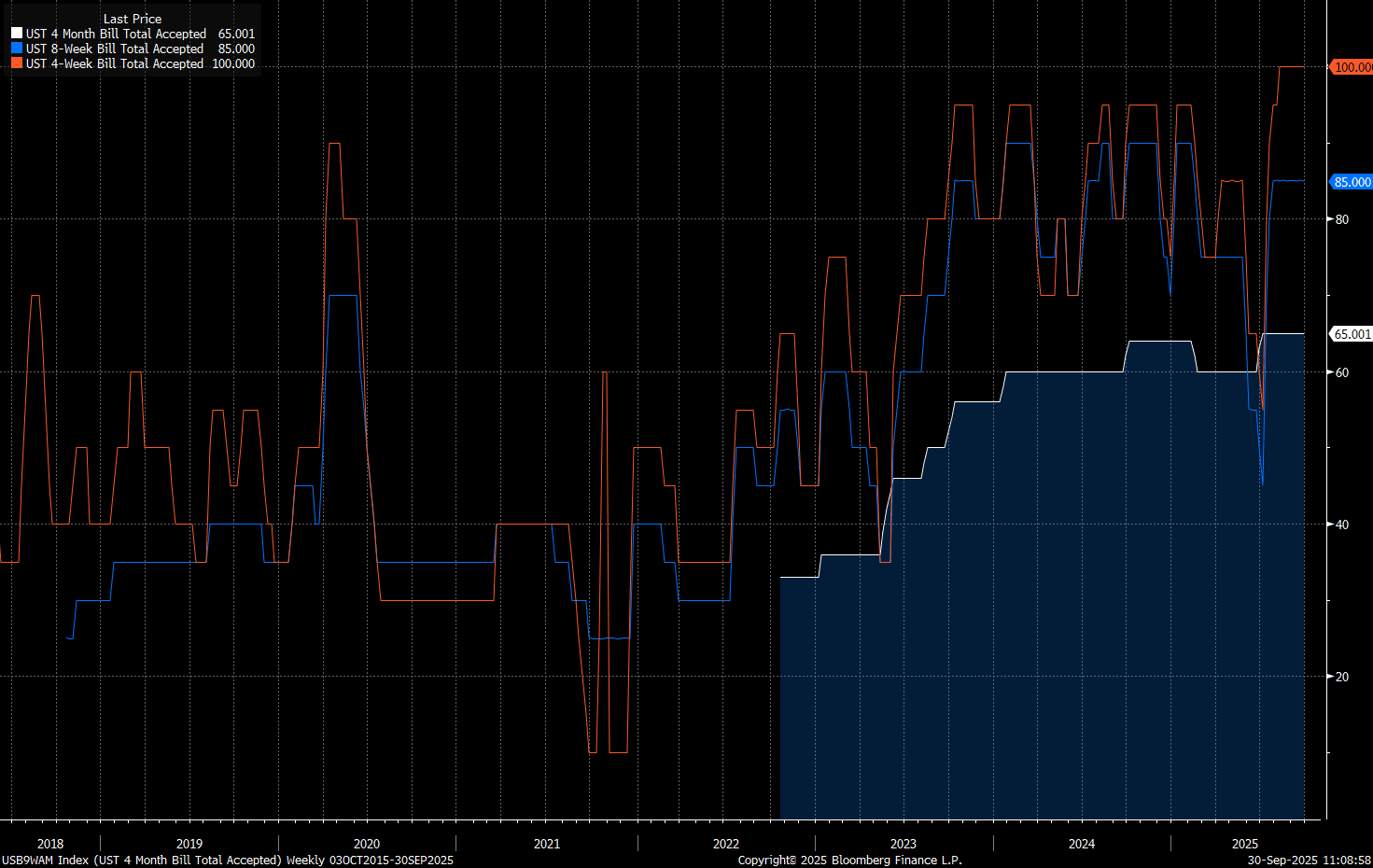

Treasury's bill auction sizes for this week were unexpectedly upped: 4-week by $5B to a record $105B, 8-week also by $5B to a joint-record $90B, and 4-month by $2B to a record $67B. See chart below for size history.

- Instead of raising $5B in net cash if they had been unchanged, these will raise $17B on next Tuesday Oct 7's settlement.

- Most expectations we'd seen were for bill sizes to remain relatively steady until later in October so this is coming a little early.

- While it's not clear this was the reasoning, Treasury's TGA cash position had been seen as a little weaker than had been expected in September, and likely to fall short of the $850B targeted for today's end-quarter date (was $786B as of the last Treasury statement date on Sept 26).

SOFR OPTIONS: Dec'25 SOFR Call Buy, Strangle Sale Update

Sep-30 14:55

- +15,000 SFRZ5 96.75 calls, 1.75 ref 96.31

- -12,000 SFRX5 96.12/96.62 strangles, 1.75-2.0

BOE: Breeden due to speak on monetary policy at 16:30BST

Sep-30 14:48

- Deputy Governor Sarah Breeden rarely speaks on monetary policy but her speech scheduled for today at 16:30BST at Cardiff University is provisionally entitled “The Monetary Policy Outlook”.

- This will certainly be a key speech. She sounded slightly more dovish than Governor Bailey in our view following her testimony ahead of the TSC on 3 June but hasn’t really spoken on monetary policy since.

- Her tone is likely to be pivotal for markets, particularly if she strikes a dovish tone given current market pricing.

- We think that markets are underpricing the probability of a Q4 cut with less than 1bp priced for November and less than 5bp cumulatively priced for December.

- Note that yesterday, Deputy Governor Ramsden did not rule out voting for a cut in November but was generally considered the most dovish member to not dissent at the September MPC meeting. In order to reach the five members needed for a cut we would need the two September dissenters (Dhingra and Taylor) and then likely all of Ramsden, Breeden and Bailey. That leaves the four members who hawkishly dissented in August continuing to favour a skip.