PHP: Away From 57.50 Upside Test, But Negative Sep Seasonality In Focus

USD/PHP sits just off session highs, last near 57.35/40 (still up around 0.15% for the session so far). Earlier highs were at 57.47, which was close to recent highs near 57.54 (Sep 3). The pair is back above all key EMAs, which are fairly close to the 57.00 region for the 100 and 200 days respectively.

- This leaves USD/PHP within recent ranges for now. Today's weakness in PHP doesn't appear to reflect fresh negative news. Local equities are up a touch after yesterday's 1.55% fall. Onshore media noted corruption concerns as weighing on equity sentiment. via BBG: " The Philippines’ corruption probe widened to more infrastructure projects on Tuesday, with a former public works official alleging that street lamps, roads and buildings are also overpriced and substandard."

- We did see strong offshore equity inflows yesterday, but this did little to aid PHP sentiment in aggregate.

- Month end and quarter end flows could also be starting. Traditionally PHP has negative seasonality versus the USD in the month of Sep. USD/PHP gains are on average 1.1% in Sep going back over the past 10yrs (although a few years dominate the sample, 2016, 2021 and 2022).

- BSP may look to curb a fresh break through 57.50 though, so the market is likely to be mindful of intervention risks.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: JPY Crosses - Trade Sideways As USD Collapses Across The Board

US equities exploded higher in the Friday N/Y session as the market reacted to what it interpreted to be a very dovish speech. This morning US futures opened a little lower, ESU5 -0.15%, NQU5 -0.17%. The JPY crosses traded sideways for the most part as the USD took the brunt of the reaction across the board.

- EUR/JPY - Friday night range 171.83 - 172.68, Asia is trading around 172.45. This pair’s move higher looks to be stalling for the moment. A sustained break above 173.00 could see momentum pick up and the uptrend regain the upper hand.

- GBP/JPY - Friday night 198.33 - 199.53, Asia trades around 199.05. This pair consolidated on a 198 handle on Friday night. A sustained break above 200.00 is needed to see momentum higher restored.

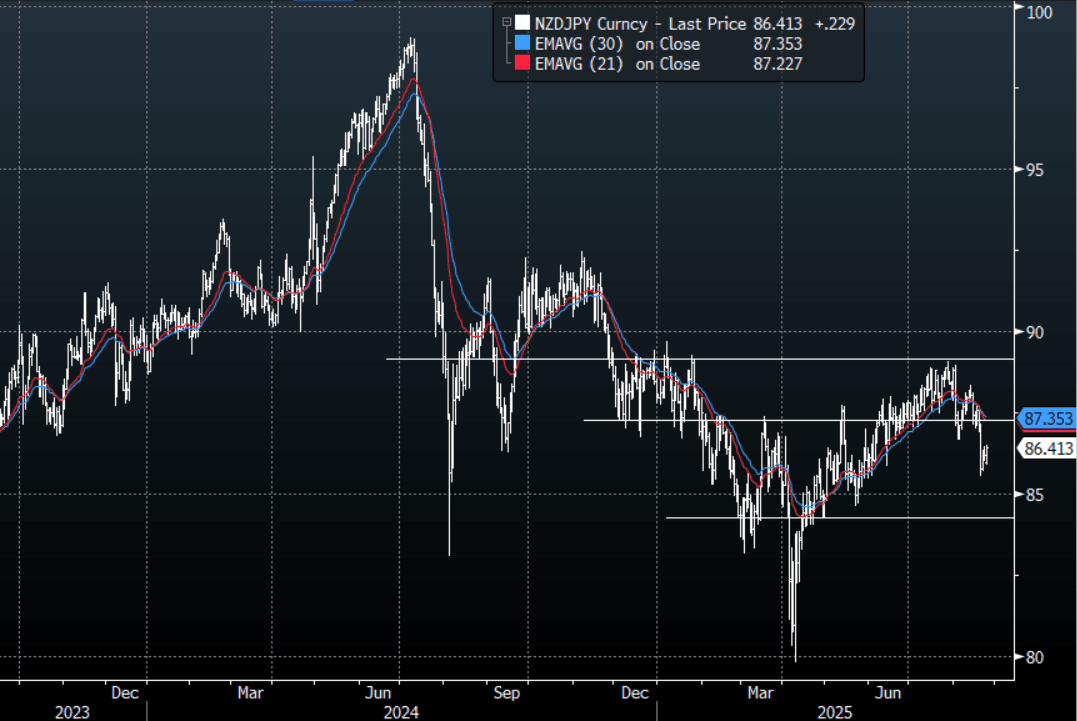

- NZD/JPY - Friday night range 86.00 - 86.46, Asia is currently dealing 86.40. The pair broke through its support around 86.50 on the back of a dovish RBNZ last week. This was a powerful move lower and if sustained should now see bounces met with supply. Any bounce back towards 87.00/87.50 should see sellers first-up, the huge bounce in risk does offer some pause for those looking for the pair to extend lower.

- CNH/JPY - Friday night range 20.4349 - 20.7058, Asia is currently trading around 20.5700. This pair has again bounced off its pivotal 20.30/20.40 support. A sustained break back below 2.3000 is needed to turn momentum lower again, until then it looks comfortable in a 20.4000-20.9000 range.

Fig 1 : NZD/JPY Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSTRALIA: Analysts Split Over Where Cash Rate Expected To Trough

Bloomberg’s updated consensus forecasts show that the RBA is widely expected to be on hold in September and that there will be one final cut for the year in Q4, likely November as that coincides with the RBA’s revised outlook. The survey was taken over August 14-19, after the last RBA decision and updated forecast release. Forecasters are split over 2026 though and where rates will trough with most projecting either 3.35% with no moves in 2026 or 3.1% with one last cut early next year.

- One of the main outliers is Westpac, which expects another rate cut in Q2 2026 with the cash rate then stabilising at 2.85%. AMP is forecasting the same path.

Australia cash rate projections %

- There were only slight revisions to the RBA’s August staff projections and it appears there was nothing in them or the statement for analysts to change their forecasts.

- Consensus still expects CPI inflation to be at 2.9% y/y in Q4 2025, 0.1pp below RBA, and 2.7% in Q4 2026, 0.2pp lower than RBA.

- Growth expectations are unchanged for 2025 with both Q2 and Q3 still forecast to rise 0.5% q/q and Q4 0.6%. Q4 2025 is in line with the RBA at 1.7% y/y but Q4 2026 is 0.2pp stronger at 2.3%. 2026 has been revised down 0.1pp to 2.2%, due to weaker expected GFCF, with 2027 unchanged at 2.5%.

- The unemployment rate is also little changed. It is forecast to end 2025 0.1pp higher at 4.4%, 0.1pp above the RBA, but then stay there until end 2026 when it moderates to 4.3%.

- The probability of a recession remains low at 15%.

NEW ZEALAND: VIEW: Westpac Expects Spending To Rise As Cuts Feed Through

Retail sales volumes rose 0.5% q/q in Q2, which was stronger than expected. Westpac notes that while conditions for the sector remain tough, there are signs of a “long-awaited recovery”. Real sales grew 2.3% y/y after 0.7%. Core real sales were stronger than the headline rising 0.7% q/q after 0.4%. Westpac is currently forecasting a flat Q2 GDP print on September 18 but will review its forecast after other quarterly data releases.

- Westpac is optimistic regarding the consumption outlook noting that “spending levels are already pushing higher, and the full impact of the large reductions in interest rates over the past year is yet to be felt”.

- “Over the coming months, increasing numbers of borrowers will be rolling on to lower borrowing rates. The related lift in disposable incomes could be sizeable in some cases, and that’s set to boost spending through the latter part of the year.”

- “There are still some headwinds for the retail sector. Most notably, unemployment is likely to rise around to 5.3% before the end of the year.”

- “While the retail sector is still confronting some tough trading conditions, we are starting to see signs that the long-awaited recovery is taking shape. Spending levels have risen for the past three quarters. That includes gains in discretionary areas like recreational goods and electronics. However, it is still a mixed picture with spending in sectors like hospitality still flat.”

- However, “spending growth remains quite modest – the volume of goods sold rose around 2.5% over the past year, compared to gains of around 4.5% per annum before the pandemic”.