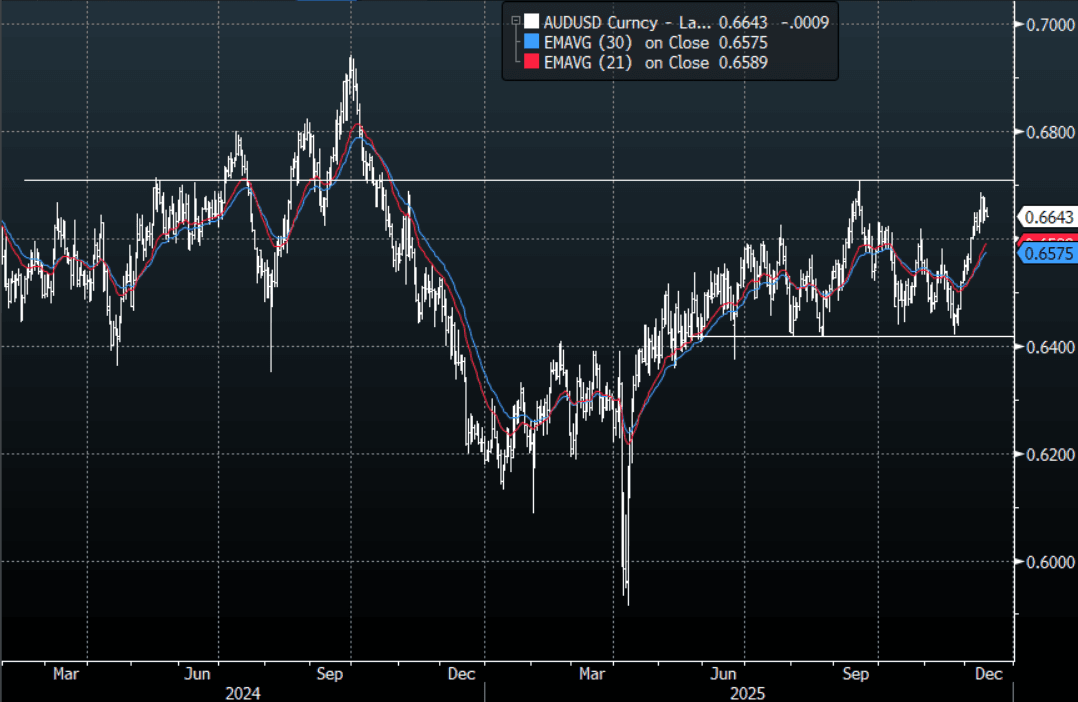

AUD: AUD/USD - Stalls Above 0.6650 As Risk Ends The Week Poorly

The AUD/USD had a range Friday night of 0.6633-0.6677, Asia is trading around 0.6645. The US stock market wobbled on Friday as AI concerns came back to the fore and US yields in the long end tick back up. This saw the USD’s decline stall but it has not bounced, yet. The AUD price action remains very constructive but the way risk starts the week will have important implications for its direction. While the AUD remains above 0.6500-0.6550 I suspect dips should continue to be supported. In the Asian session, I will be watching how risk opens the week and whether the 0.6600-0.6630 will continue to find demand. If this area does not hold it could signal a deeper pullback toward the 0.6550 area.

- Bloomberg - China Vanke failed to obtain sufficient support for its plan to delay paying a 2 billion yuan ($283 million) note due Dec. 15. {NSN T74QOOKGZAJ6 <GO>}

- Alexander Stahel on X believes this could have huge implications for Macro: “Let me be clear: This crisis is nothing the world has ever seen before. It makes the Japanese 90ies bust look like a children’s birthday. Sooner or later, the Chinese economy, and with demand for energy commodities and base metals, will fall into an “air-pocket”. Inevitable.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6555(AUD548m), 0.6650(AUD970m), 0.6750(AUD494m) . Upcoming Close Strikes : 0.6550(AUD1.07b Dec 18 ), 0.6675(AUD8989m Dec 18 ) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 39 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Softer To End The Week As Intraday Rally Reverses

Treasuries softened to end the week, with early gains dissipating and the cash curve ending bear steeper.

- An overnight selloff in Gilts related to UK fiscal concerns spilled over lightly into the US in early trade, but maintained a cautious tone for Treasuries following on from Fed commentary earlier in the week dampening enthusiasm for a December rate cut as well as weak long-end Treasury auctions.

- However a pullback in equities was enough to provide a safe-haven bid in equities which saw TY futures briefly touch the best levels of November so far. That would reverse however, with equities finding their footing and turning higher for the day and returning Treasuries to early morning levels.

- With the federal government shutdown now over, some postponed data is starting to come into view, with the BLS scheduling September's delayed nonfarm payrolls report for next Thursday, and the Census Bureau set to publish some delayed August data next week.

- Still, there's no official word on the fate of the October CPI release, which looks very likely to be cancelled altogether, or the date of the October employment report's publication (which is likely to see an establishment survey but not a household one).

- Against this backdrop, Friday's Fed commentary (with the usual exception of Gov Miran calling for further easing in December) was roundly hawkish, with Dallas's Logan and KC's Schmid reiterating their opposition to a December rate cut, largely out of concern over entrenched inflation. A December cut remained around 50/50 priced.

- Latest levels: The 2-Yr yield is up 2.1bps at 3.6121%, 5-Yr is up 2.6bps at 3.7327%, 10-Yr is up 2.7bps at 4.1463%, and 30-Yr is up 3.4bps at 4.7458%. Dec 10-Yr futures (TY) down 7.5/32 at 112-17 (L: 112-16 / H: 113-04.5)

- Along with the newly-rescheduled data mentioned above, next week's calendar includes the October FOMC minutes (we're watching for color on the debate over whether to ease any further) and flash November PMI data.

OPTIONS: US Options Roundup - 14 Nov 2025

Friday's U.S. rates/bond options flow included:

- TY Week4 (expiry 28th Nov) 112.75/113.50cs vs 112.25p, bought the cs for flat in 30k

- TYZ5 113.00 calls ~5.6K given at 0-13.

- SFRZ5 96.37/96.43cs, traded 0.5 in 11k.

- SFRZ5 96.31/96.43cs, traded 1.75 in 4k.

- SFRZ5 96.31/96.37cs 1x2, traded flat in 7.5k.

- SFRZ5 96.31/96.37cs, traded 1.5 in 2k.

- SFRZ5 96.25^, traded 15.25 in 2k.

- SFRZ5 96.25/96.31/96.43c fly, traded 0.75 in 5k.

- SFRF6/H6 96.31/96.50^^ spread, bought for 6.25 in 2k. This was also bought into the close Yesterday for 6 in 5k.

- SFRH6 96.18/96.06ps 1x2, bought for 2.25 in 5k. This was also bought into the close Yesterday for 2 in 20k

- SFRU6 99.00/100.00/101.00c fly, traded 1.25 in 2k.

- SFRU6 96.87/97.12cs vs 0QU6 97.12/97.37cs, bought the front for 0.75 in 2.5k.

- 0QZ5 97.00/97.06/97.18c fly 2x3x1, traded 1.5 in 5k.

- 0QZ5 97.00/97.06/97.18/97.25c condor, traded for 1 in 4k.

- 0QF6 96.93/97.06cs, traded 4.5 in 10k.

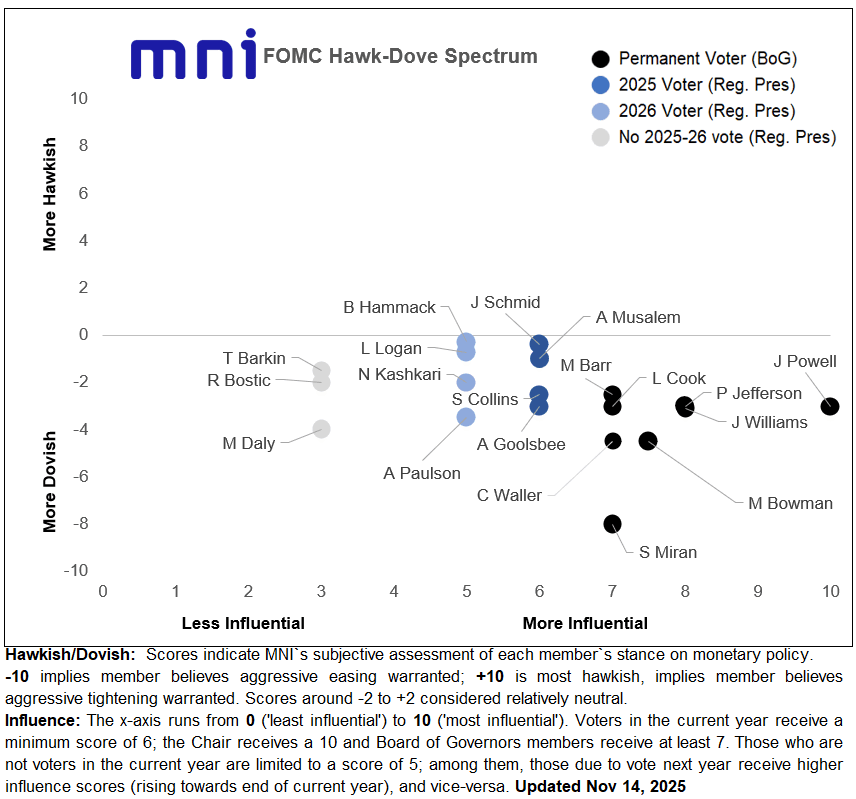

FED: Dallas's Logan Reiterates Cut Opposition; Regional Voters Getting Hawkish

Dallas Fed President Logan, a 2026 FOMC voter, reiterates that she doesn't currently see the need for a rate cut in December - recall she said after the October meeting that she opposed that cut.

- “I think it would be hard to support another rate cut unless we were to get convincing evidence that inflation is really coming down faster than my expectations or that we were seeing more than the gradual cooling that we’ve been seeing in the labor market". She says that “until I see convincing evidence that we are headed all the way back to our 2% target, I really do think modestly restrictive policy is appropriate." In general "it does not seem like a labor market to me that would for me... to see that it would be appropriate for further preemptive insurance."

- She was appearing at a joint Dallas-KC Fed event, the latter of whose president Schmid dissented in favor of a hold in October.

- Logan's comments are a reminder that the 2026 FOMC regional Fed presidential voters appear to be leaning increasingly hawkish: Logan, Cleveland's Hammack, and Minneapolis's Kashkari all say they did not support the October cut, though Philadelphia's Paulson appears to be more dovish-leaning.

- Generally speaking, the regional presidents have become quite hawkish versus the Fed Board - of the 12 presidents, it's only really SF's Daly and Philadelphia's Paulson that seem clearly amenable to further near-term rate cuts. Our latest Hawk-Dove update is below.

- We'll be watching in the FOMC Minutes (1400ET next Wednesday) for the degree of expressed opposition to October's rate cut and color on the debate over whether to ease any further. At the press conference, Chair Powell highlighted FOMC division over prospects for a December cut: “there's a growing chorus now of feeling like maybe this is where we should at least wait a cycle, something like that”, and noted that the meeting minutes would offer some more color on the internal debate. Since the meeting it's been clear that the hawks have become more vocal and arguably more entrenched, with more reluctance to ease any further given the federal data "fog".