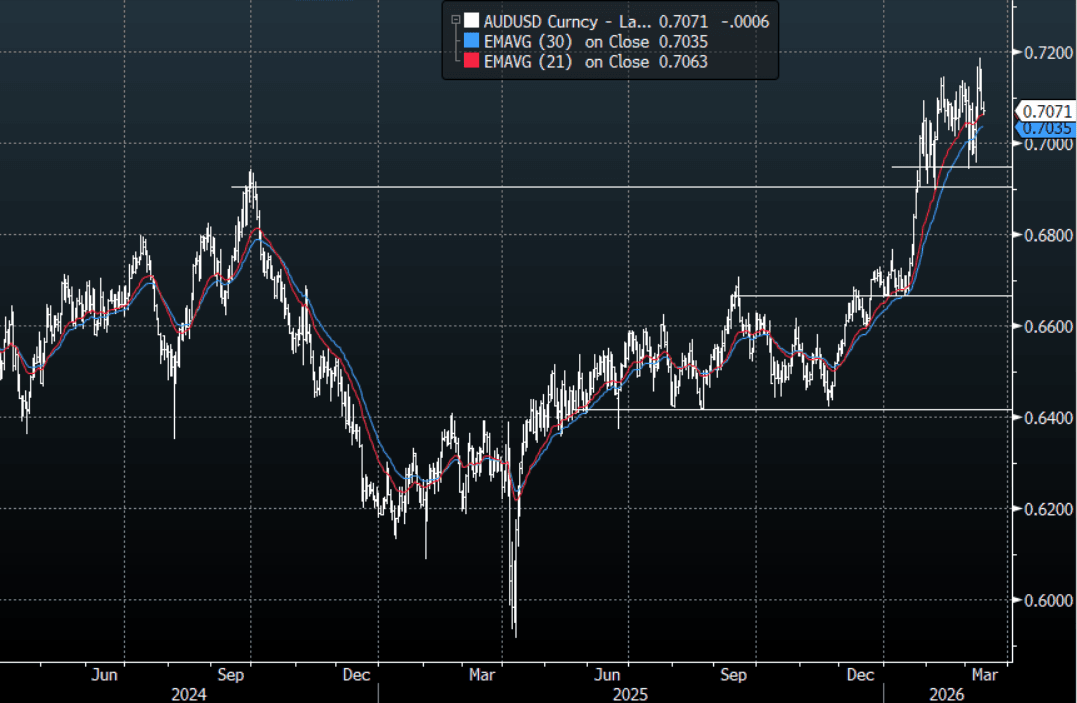

AUD: AUD/USD - Pulls Back Below 0.7100 As Risk Aversion Grows

The AUD/USD has had a range today of 0.7061-0.7092 in the Asia- Pac session, it is currently trading around 0.7070, -0.10%. The AUD could not hold above the 0.7100 area as it stalled toward 0.7150 and when US stocks got hit overnight the pair could no longer shrug off the backdrop for risk and quickly fell lower. The AUD is being caught between those wanting to be long as rate hikes are brought forward and those looking for a proxy for risk. Ultimately the price remains within this 0.6900-0.7200 range as the conflict continues for now and while above the pivotal 0.6900-0.6950 area the bulls hold the slight edge, but the market is already long so will be hoping for risk to stablise. On the day, this price action is tough to trade with conviction but I suspect with risk back under pressure and the inability to hold above 0.7100 will probably see any bounce back toward 0.7110-0.7140 faded initially.

- MNI AU - 25bp Hike By RBA Next Tues At ~70% Chance: Going into next week's RBA policy decision, RBA-dated OIS pricing implies a 71% probability of a 25bp hike, up from 35% at last Friday's close. The market is now as confident about a hike as it was ahead of February's 25bps hike to 3.85%

- “Institutional investors are buying US dollars at the fastest pace in nearly two years, as the Middle East conflict fuels a rush into safe havens, State Street said.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.7000(AUD853m), 0.7100(AUD896m), 0.7130(AUD839m). Upcoming Close Strikes : 0.6950(AUD1.07b Mar 18 ), 0.7100(AUD1.41b Mar 16), 0.7100(AUD752m Mar 18) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 93 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Richer Ahead Of US NFP, Stronger Demand Drove Hike - RBA Hauser

ACGBs (YM +3.0 & XM +6.5) are stronger.

- MNI: The Reserve Bank of Australia’s 25bp February hike to 3.85% reflected stronger global growth, looser financial conditions and firmer private demand relative to supply, Deputy Governor Andrew Hauser said.

- There has no cash US tsys dealings in today's Asia-Pac session, with Japan out on holiday.

- All focus turns to today's US employment data. Monthly payroll growth is currently expected at 70k in January for a slight acceleration from the 50k in December and 56k in November.

- Cash ACGBs are 2-5bps richer, with the 3/10 curve flatter.

- The latest ACGB April 2037 auction attracted solid demand, with the weighted average yield printing 0.68bps through prevailing mid-yields.

- Moreover, the cover ratio jumped sharply to 4.1429x from 3.4933x at the previous auction. The AOFM also plans to sell A$1000mn of the 2.50% 21 May 2030 bond on Friday.

- The bills strip has bull-flattened, with pricing flat to +3 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 15% for March to 93% by June and 146% by December 2026.

- Tomorrow, the local calendar will see Consumer Inflation Expectation data alongside the RBA’s Senate Testimony and RBA Hunter’s Speech.

Bloomberg Finance LP

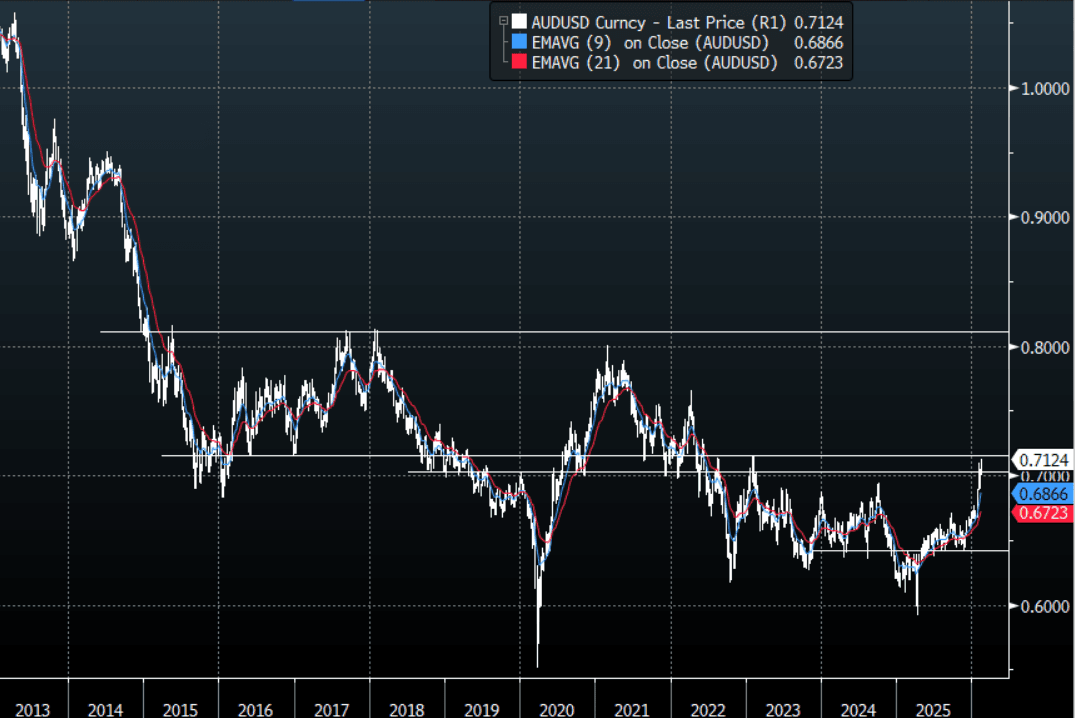

AUD: AUD/USD-Extends Above 0.7100 As Hauser Says: "Will Do What's Necessary"

The AUD/USD has had a range today of 0.7067 - 0.7128 in the Asia- Pac session, it is currently trading around 0.7125. The AUD took another leg up across the board as the market reacted to Hauser saying they “will do what's necessary to return inflation to target”. The USD is again back under pressure and the move lower in yields overnight is just adding to its headwinds, the AUD remains a favourite vehicle to express a long against it. The AUD has been outperforming across the board as leveraged funds continue to add to their longs as further hikes are potentially priced in. On the day, the first support is back toward the 0.7040–0.7070 area, and then the 0.6950 area. The bulls will be looking for dips to remain supported in order to break above the pivotal 0.7100-0.7200 area. A sustained break above here targets 0.7600-0.7800 first and then 0.8000-0.8200.

- "HAUSER: WILL DO WHAT'S NECESSARY TO RETURN INFLATION TO TARGET" - BBG

- MNI BRIEF: Stronger Demand Drove Hike - RBA's Hauser. The RBA’s 25bp February hike to 3.85% reflected stronger global growth, looser financial conditions and firmer private demand relative to supply. The reason policy turned around in February is because the facts changed,” he said, referring to last week’s decision.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.7010(AUD560m). Upcoming Close Strikes : 0.6800(AUD1.55b Feb 13), 0.6850(AUD933m Feb 12) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 80 Points

Fig 1: AUD/USD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

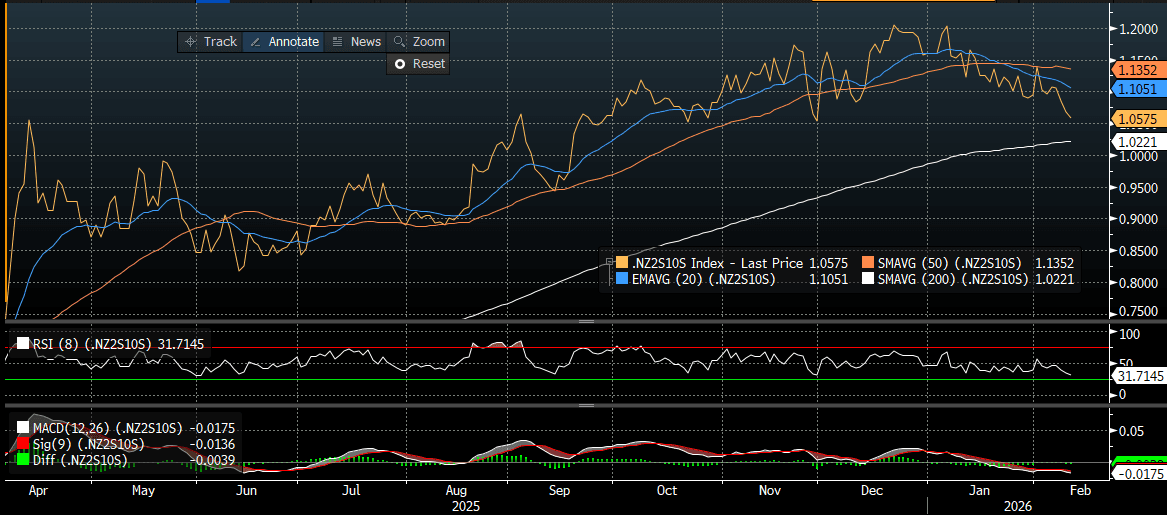

BONDS: NZGBS: Bull-Flattener Leaves Curve At Its Flattest Since Nov

NZGBs closed showing a bull-flattener, with benchmark yields 2-4bps lower.

- Nevertheless, NZGBs underperformed ACGBs with the NZ-AU 10-year yield differential 2bp wider on the day.

- There has no cash US tsys dealings in today’s Asia-Pac session, with Japan out on holiday.

- (Bloomberg) “New Zealand’s government has started an independent review of New Zealand’s monetary policy response to the Covid-19 pandemic. Purpose of the review is to identify lessons New Zealand could learn to improve the monetary policy response to future major events.”

- Swap rates closed 2-5bps lower, with the 2s10s curve flatter. At 1.06, the curve is at its flattest since late November (see chart).

- RBNZ-dated OIS pricing closed little changed across meetings. No tightening is priced for February, while December 2026 assigns 43bps.

- The local calendar will be light until Friday's release of BusinessNZ Manufacturing PMI, Net Migration and RBNZ Inflation Expectation data.

- Tomorrow, the NZ Treasury plans to sell NZ$250mn of the 1.50% May-31 bond and NZ$200mn of the 4.5% May-35 bond.

Bloomberg Finance LP