FOREX: AUD Crosses - AUD Underperformance Back In Focus

US stocks gave back all their gains overnight as a federal appeals court offered President Donald Trump a temporary reprieve. The AUD gave back all its gains overnight and resumed its path towards expressing weakness in the crosses.

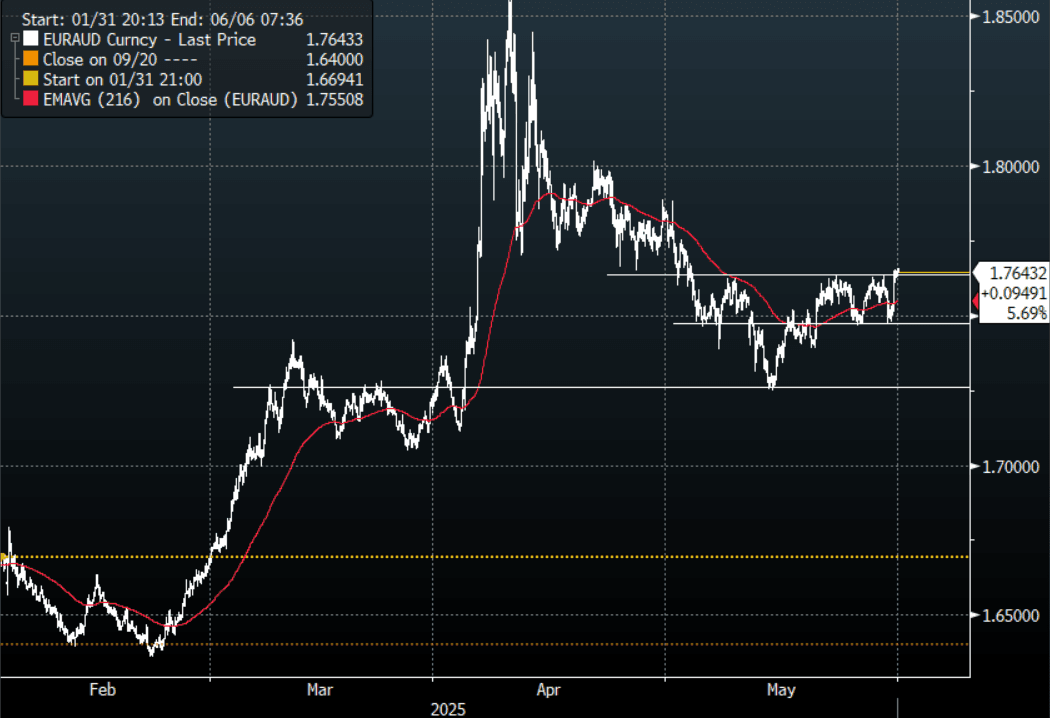

- EUR/AUD - Overnight range 1.7481 - 1.7659, Asia is trading around 1.7640. The pair saw solid demand sub 175.00 and was very quick to move higher on the news. Price action shows the market is bearish the AUD for now in the crosses. If price can hold this move back above 1.7650 it could signal its about to extend back to 1.7800 on route to 1.8000.

- GBP/AUD - Overnight range 2.0879 - 2.0970, Asia is trading around 2.0940. Good demand seen sub 2.0900. This pair continues to build for a potential break back above 2.1000.

- AUD/JPY - Overnight range 92.78 - 93.84, Asia is trading around 92.75. Ouch, what a mess. Price action shows the market was short, but was also very quick to re-instate positions. Range looks 92.00 - 94.00 for now, a sustained break sub 91.50/92.00 will bring focus back to towards the lows again.

AUD/NZD - Overnight range 1.0772 - 1.0823, the cross is dealing in Asia around 1.0780. A top looks in place now just above 1.0900, the market will have been looking for a more dovish tone from the RBNZ and AUD/NZD should now see supply on bounces. The sell zone is back towards 1.0825/50 with the first target being around 1.0650.

Fig 1: EUR/AUD spot Hourly Chart

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LNG: Gas Looking Oversold As Market Worries About Tariff Impact On Demand

European gas prices fell 2.2% to EUR 31.70 on Tuesday and only slightly off the intraday low of EUR 31.20. They are now down around 22% in April, and flashing oversold, driven by not only the end of the winter but also concerns over the impact of US protectionism on global energy demand. Uncertainty remains over the progress of US trade negotiations especially with China, which it continues to deny are taking place.

- The sharp fall in gas prices in April in addition to warmer weather has helped the outlook for Europe’s ability to refill storage ahead of next winter. Current weak demand from Asia has also contributed to increased LNG shipments to Europe. However, the region remains vulnerable to unexpected outages and a heatwave, particularly in Asia.

- Scheduled Norwegian maintenance has taken place this week.

- US natural gas rose 1.1% to $3.38 after reaching $3.46 earlier in the session, but it is still down over 20% this month which is part of the shoulder season with little demand for either cooling or heating. The rally was driven by unwinding of oversold positions as forecasts for the eastern and southern US signalled cooler weather, according to the Commodity Weather Group.

JAPAN DATA: Retail Sales Pot Slight Miss, Still Up +3%y/y

Japan retail sales were slightly below market forecasts. We were -1.2%m/m, against a 0.7% forecast, with Feb revised to a 0.4% gain. In y/y terms we rose 3.1%, against a 3.5% forecast and 1.3% in Feb.

- The y/y trend is around mid range of the past 12 months as we have oscillated between flat to +5%. The authorities remain focused on driving sustained/positive real household spending growth, aided by positive real wages growth. The next round of labour earnings data is due next Friday.

- Looking at the detail, the biggest m/m declines were for motor vehicles -4.8%m/m, and department stores -3.7%m/m.

US TSYS: Cash Open

TYM5 is trading 112-07, up 0-02 from its close.

- The US 10-year yield has opened in Asia around 4.16%, down 0.01 from its close.

- “The trade deficit widened to a record in March, and consumer spending slowed, contributing to the GDP growth slowdown. Any demand pulled forward ahead of tariffs will dampen growth in subsequent quarters, posing downside risk for the second half of this year.”(per BBG)

- MNI US Economist - The monthly PCE report should offer a timely update on consumer spending momentum heading into Q2. Its inflation components are expected to show a material moderation in core PCE to a ‘low’ rounded 0.1% M/M after a 0.365% M/M in February that stands a good chance of being revised up to the cusp of 0.4-0.5% M/M (making a March read-through from the earlier quarterly data more challenging).

- The 10-year Yield, has put in a lower high around 4.40% and has broken through the recent support around 4.25%. The next support is towards the 4.10% area.