FOREX: AUD Crosses - AUD Continues To Outperform, Reaching Levels To Pare Back ?

US equities continued to grind back towards its all-time highs brushing off concerns of an imminent US shutdown overnight. This morning US futures have opened lower on our open as the shutdown begins to be executed, E-minis(S&P) -0.35%, NQZ5 -0.45%. The AUD looks to be rebuilding momentum higher in the crosses after a period of consolidation.

- EUR/AUD - Overnight range 1.7714 - 1.7849, Asia is currently trading around 1.7765. The pair topped out after multiple failures to extend above 1.7900. Price is still in the middle of its recent 1.7600 -1.8100 range having failed to extend lower after moving below 1.7750 overnight. Expect sellers to fade bounces while price remains below 1.8000.

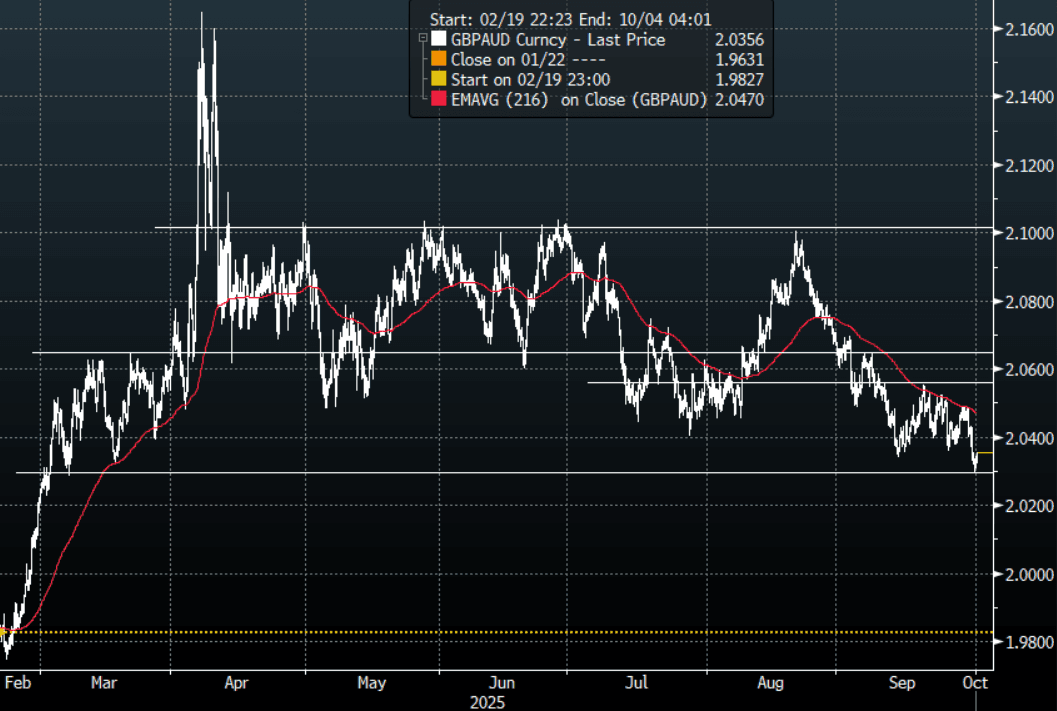

- GBP/AUD - Overnight range 2.0293 - 2.0428, Asia is trading around 2.0350. The pair has seen supply return on every look above 2.0500, the move lower has stalled back toward its support around 2.0300 where we should initially see some demand return, risk/reward looks a decent long first up. The price action of the pair is looking potentially exhaustive but a sustained break sub 2.0300 is needed to open up a deeper pullback towards 1.9800/2.0000.

- AUD/JPY - Overnight range 97.43 - 97.98, Asia is trading around 97.80. The pair found solid demand back towards 97.00 and bounced last week with the help of the AU CPI print. While above 97.00 the focus will remain on September’s highs toward 98.50.

- AUD/NZD - Overnight range 1.1359 - 1.1418, the cross is dealing in Asia around 1.1400. The Cross has broken above the multiple highs around the 1.1200 area and has accelerated up towards 1.1400. I would think this 1.1400/1.1500 area would initially be met with sellers and expect some work to be done up here before another extension higher.

Fig 1: GBP/AUD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Futures Softer, Following US Lead, Capex Data Stronger Than Forecast

The early bias for JGB futures is softer, the Sep future was last 137.42, -.12 versus settlement levels. Recent lows rest at 137.22, which will be a downside focus point. The bias in US futures has been to track lower in early Monday dealings, although today so there is no cash trading.

- The other weight for futures may be from slightly better than expected capex data, which was led by strong rises in manufacturing capex for Q2. This paints a resilient backdrop for this part of growth. However, JPY is little changed so far today, so it isn't impacting FX markets.

- The final outcome for the August print of the S&P manufacturing PMI has crossed. It came in at 49.7, against a preliminary August read of 49.9.

- In the cash JGB space, yields are higher across the benchmarks, with the back end leading a touch. The 10yr is edging back up towards 1.62%. The 30yr is around 3.20%. The 2/30s JGB curve is little changed though at +232bps.

- Swap rates are biased higher as well, the 10yr last close to 1.425%.

US: What Are Trump's Options If SCOTUS Agrees On Tariff Judgement ?

The Court of Appeals for the Federal Circuit has upheld that decision by a 7–4 majority, saying the emergency powers law Trump relied on — IEEPA — which was never meant to authorize tariffs. Where does Trump go from here and what are his options should the Supreme court uphold the judgement ? Alexander Stahel wrote a thread on X expanding on Trump’s possible alternatives: https://x.com/BurggrabenH/status/1961978205084012795

- “Trump’s “Liberation Day” tariffs rested on the International Emergency Economic Powers Act (IEEPA), a law that gives presidents sweeping authority to act during genuine national emergencies involving foreign threats — freezing assets, blocking sensitive goods, and so on. But as two federal courts have now made clear, it was never meant to cover tariffs. Unless the Supreme Court reverses those rulings, this door is effectively closing.”

- “IEEPA is not the only tool available. The other big weapon is Section 232 of the Trade Expansion Act, the so-called national security tariff authority. Trump used it in 2018 to impose tariffs on steel and aluminum, arguing they were essential to national security.”

- “A third possibility is Section 301 of the Trade Act of 1974, which allows tariffs in response to unfair trade practices by specific countries. Lighthizer (Trump 1.0) leaned heavily on this authority in his first term, especially against China, citing intellectual property theft and forced technology transfers. But Section 301 is narrower: it targets specific offenders, not the world at large. It should justify tariffs on China, but not a blanket 15% levy on the EU, 39% on Switzerland, or dozens of others.”

- “Finally, there is Congress. Under the Constitution, tariffs are Congress’s prerogative. If Trump wanted to go further than the existing laws permit, he would need Congress to pass new legislation. Given today’s polarization, with Democrats firmly opposed and many Republicans split on tariffs, it seems unlikely that Congress would hand him additional powers.”

- “Bottom line? Under IEEPA, the courts are saying no — with the Supreme Court judgment likely by the summer of 2026. Then, sadly, the saga likely continues under different laws. Time will tell.”

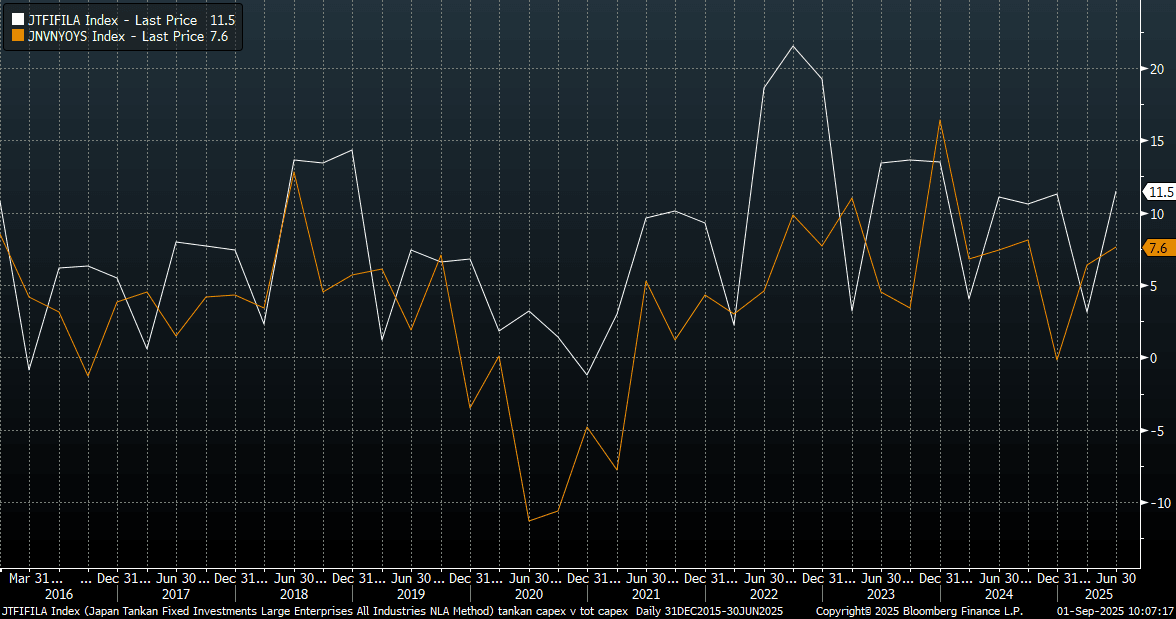

JAPAN DATA: Q2 Capex A Touch Above Expectations, Led By Manufacturing

Japan Q2 capex was a touch above market expectations. The headline figure rising 7.6%y/y, against a 6.1% forecast, while Q1's outcome was 6.4%. Ex software capex was also above expectations, up 5.2%y/y, against a 4.9% forecast, but down from Q1's pace of 6.9%. Company sales were up 0.8%y/y in Q2, against a 1.4% forecast and 4.3% prior. Profits were 0.2%y/y, against the -0.4% forecast and 3.8% gain in Q1.

- The detail on the capex side should manufacturing up 16.4%y/y in Q2, with ex software up 17.0%y/y. In the quarter capex was up 1.6%, led by manufacturing's 6.3% rise.

- The chart below plots the headline capex result against the Tankan survey of capex estimates (which is the white line in the chart). This continues to paint a resilient backdrop, with the Q3 Tankan survey out at the start of Oct and likely to be a key watch point for the BoJ.

- On the profit side, weakness in manufacturing -11.5%y/y, weighed on the overall result.

- For sales, manufacturing and non-manufacturing slowed in y/y terms relative to Q1.

Fig 1: Japan Capex & Tankan Capex Expectations

Source: Bloomberg Finance L.P./MNI