FED: Asset Runoff Winding Down, KC's Schmid Eyes Shorter-Duration Holdings (2/2)

The overall size of the Fed's balance sheet was little changed in the latest week however, with a small ($4.6B) net rise in emergency lending/liquidity facility takeup. That included a $6.0B increase in dealer repo operations but a combined $1.4B drop in foreign bank swap line and discount window takeup. Some of that takeup appeared related to month-end October dynamics but those have abated and overall, emergency/liquidity facility takeup is down $1B over the last month.

- Asset runoff did not progress in the latest week, with no change in SOMA holdings, though they're down $20B over the last 4-week span ($4.5B Tsys, $16B MBS). QT will end on December 1.

- The Fed debate over what to do next continues to play out in public commentary among FOMC officials, and we await next week's October meeting minutes for any further insight into the discussion that preceded the decision to end QT. The latest official to weigh in is KC Fed President Schmid who said he supported the decision, he maintained a cautious tone over future balance sheet decisions: "in the longer-term I would like to operate with the smallest and least distortive balance sheet that we can. A large balance sheet increases the Fed’s footprint in financial markets, distorts the price of duration and the slope of the yield curve, and potentially blurs the line between monetary and fiscal policy."

- As with other Fed officials, he is eyeing the smallest possible balance sheet, and a shift in holdings toward shorter-duration securities. Of course, from Dec 1 onward, maturing/prepaid MBS will be rolled into bills, and it's likely the Fed will purchase bills in future reserve management operations.

- Schmid says: "Even without changing the overall size of the balance sheet, the Fed can take action to lessen its footprint in financial markets. Currently, our asset holdings are disproportionately weighted towards long-duration assets, which distorts the price of duration, lowering long-term rates and artificially flattening the yield curve. By shifting our holdings toward shorter-duration securities we can decrease this distortion. A shorter maturity balance sheet could also better adapt to the rapidly changing payments environment. While the ample reserves framework eliminates the need for day-to-day reserves management, once run-off ends there will still be a need to regularly assess the level of ample reserves. And I see little reason to think that reserve demand will grow steadily with nominal GDP, particularly given innovation in payments. For example, the move towards instant payments could have unforeseen effects on the level of ample reserves. A portfolio with a greater proportion of bills and short-term coupons could more quickly adjust should we see a shift in the demand for our liabilities."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

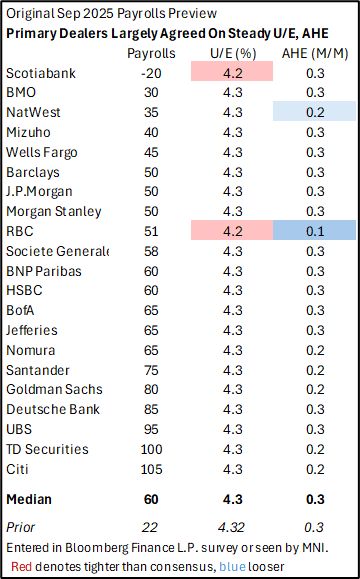

US LABOR MARKET: Median Primary Dealer Analyst Had 60k Payrolls Growth In Sept

From our "Shadow" employment report for September circulated earlier (PDF): While now of course delayed, the September nonfarm payrolls report had seen a primary dealer analyst median estimate of a 60k increase in nonfarm payrolls (range -20k to 105k).

- These estimates came with the usual analyst forecast round ahead of the release, including before a weak ADP release.

- It’s possible that these will be revised down ahead of the actual release, whenever that may be.

AUDUSD TECHS: Hammer Candle Highlights Possible Reversal

- RES 4: 0.6726 1.236 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 3: 0.6660/6707 High Sep 18 / 17 and a bull trigger

- RES 2: 0.6629 High Sep 30 & Oct 01 and key short-term resistance

- RES 1: 0.6556 50-day EMA

- PRICE: 0.6519 @ 16:00 BST Oct 15

- SUP 1: 0.6440 Low Oct 14

- SUP 2: 0.6415 Low Aug 21 / 22 and a bear trigger

- SUP 3: 0.6373 Low Jun 23

- SUP 4: 0.6357 Low May 12

A bear theme in AUDUSD remains intact. However, yesterday’s recovery highlights a possible reversal pattern - a hammer candle formation. If correct, it signals the end of the bear leg that started Sep 17. Note too that MA studies have remained in a bull-mode position during the latest bear leg, and this highlights a dominant M/T uptrend. Initial resistance is 0.6556, the 50-day EMA. A resumption of weakness would open 0.6415, the Aug 21 and 22 low.

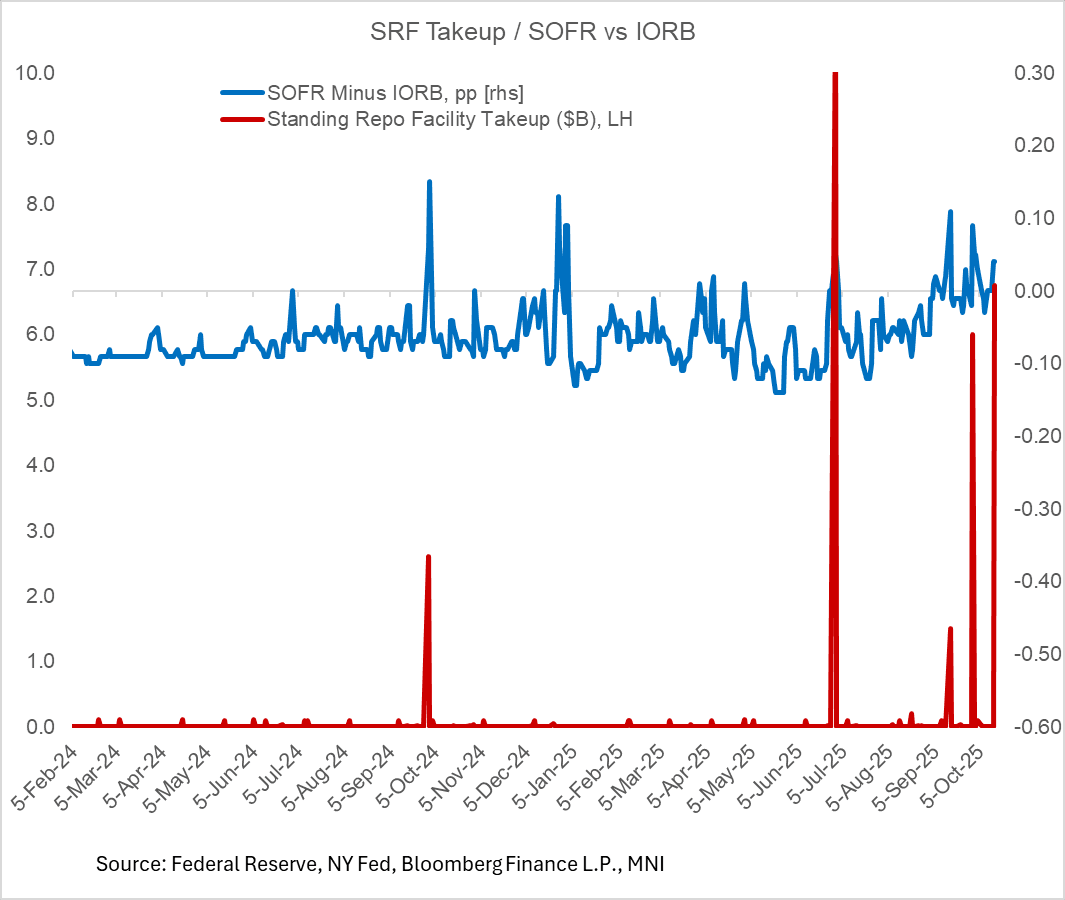

US TSYS/OVERNIGHT REPO: Fed Standing Repo Takeup Jump Part Of Wider Pressure

The Fed's Standing Repo Facility (SRF) saw its highest takeup this morning since the quarter-/month-end date of June 30.

- The $6.8B usage of the facility comes as SOFR printed 4bp above IORB (4.19% vs 4.15%) yesterday, with a variety of other indicators suggesting mounting funding market pressures. It compares with the $6.0B takeup at the last month-/quarter end date of September, and is the 2rd-highest takeup (after June 30) since Q2 2020. (The SRF was made permanent in 2021).

- Even so this rise should be put into perspective; takeup was many times larger in 2019 during a previous episode of funding pressures that led to the Fed restarting asset purchases. And per the September meeting minutes, "a few participants noted that the SRF would help keep the federal funds rate within its target range and ensure that temporary pressures in money markets would not disrupt the ongoing reduction in Federal Reserve securities holdings to the level needed to implement monetary policy efficiently and effectively in the Committee’s ample-reserves regime"

- Even so, there's a variety of factors contributing to the rise in takeup. Based on various measures we (and the Fed) look at, some funding market pressure has been building up for a few weeks now as reserves fell below $3T - the pressures are still on the light side but enough to get the Fed thinking about slowing runoff (as evidenced by Chair Powell's speech Tuesday in which he suggested QT could end in the coming months).

- Today's pressures may be related to a tax date and decently large coupon settlements (just under $40B, sandwiched between $52B in bills combined over Tuesday and Thursday) removing reserves from the system.

- SOFR was 4.19% Tuesday so it wouldn't be surprising if it weren't far below the 4.25% SRF rate today, making it a closer-than-usual tradeoff.