LNG: Asian LNG Prices Largely Steady on Week: Reuters

Oct-24 17:45

Asian spot LNG prices were mostly steady this week as high inventories and weak demand balanced out colder weather and renewed sanctions risk, according to Reuters.

- The average price for December delivery into north-east Asia rose slightly by 10 cents/MMBtu on the week to $11.20/MMBtu.

- An early cold snap in northern China boosted immediate demand and lent some price support.

- However, rising domestic gas output and ample storage in China, along with softer demand in Thailand, are expected to cap prices.

- This downside is being offset by stronger heating demand in Korea and northern China, and potential disruptions linked to new sanctions on Russian LNG.

- In Japan, temperatures are forecast to drop below seasonal norms later this month, but this has yet to generate extra spot demand.

- Meanwhile, the U.S.–Asia arbitrage via the Cape of Good Hope is encouraging more American cargoes to head towards Asian markets.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY OPTIONS: Nov'25 10Y Skew Play

Sep-24 17:45

- +15,000 TYX5 111/112 put spds 1 over 114 calls ref 112-22.5

CANADA DATA: Pullback In Aug Manufacturing Sales In Line With Monthly Volatility

Sep-24 17:36

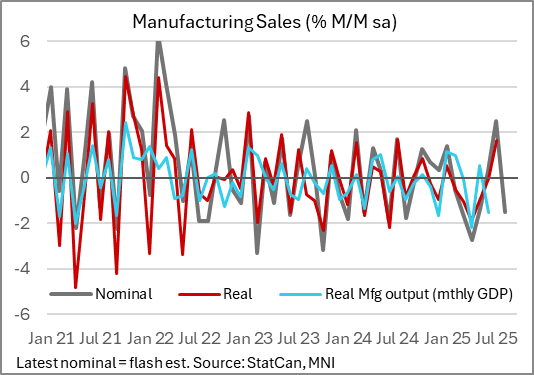

StatCan's advance estimate of manufacturing sales for August is for a 1.5% M/M decrease, which if confirmed would mark the first decrease in 3 months and partially reversing the 2.5% rise in July (all in value and not volume terms).

- As usual with the advance estimate there were no further details available, though StatCan reports the largest decreases were in the transportation equipment and food subsectors.

- Even with the M/M decrease, the comparison with the sharp drawdown in March /April/May means that manufacturing sales were due to post a 6-month best -1.5% on a 3M/3M annualized basis.

- As with other indicators, though, this one suggests the nascent pickup in activity and sentiment in various sectors in the summer - after the worst of the US-Canada trade conflict concerns - has subsequently petered out, with activity remaining volatile.

- We get July GDP data on Friday, with expectations and the advance estimate showing +0.1% M/M after -0.1% in June. Per StatCan's advance GDP release, there were no notable mentions of July manufacturing output :"Increases in real estate and rental and leasing, mining and quarrying (except oil and gas) and wholesale trade were partially offset by a decrease in retail trade" in the month.

- July manufacturing sales were confirmed at 2.5% last week, with wholesale sales ex-petroleum growth reported at 1.2% - so three of the four major "sales" categories point to a pickup in July activity (retail sales fell 0.8% however), in line with the StatCan advance anecdote).

- For August, retail sales are estimated to have bounced (1.0% M/M).

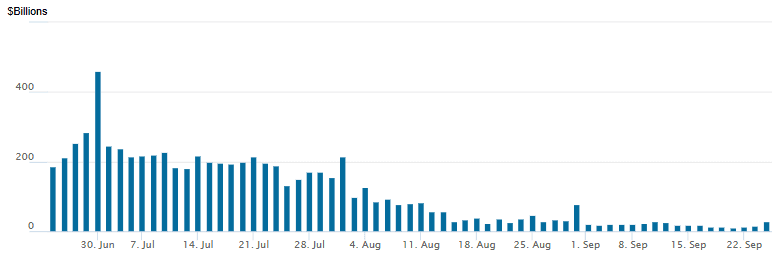

US: FED Reverse Repo Operation

Sep-24 17:30

RRP usage bounces to $29.172B with 22 counterparties this afternoon from $14.402B Tuesday. Compares to $11.363B on Friday, September 16 - lowest level since early April 2021. The year's high usage stands at $460.731B on June 30.