US TSYS: Asia Wrap - Yields Edge Higher In A Quiet Session

Aug-06 2025 04:08

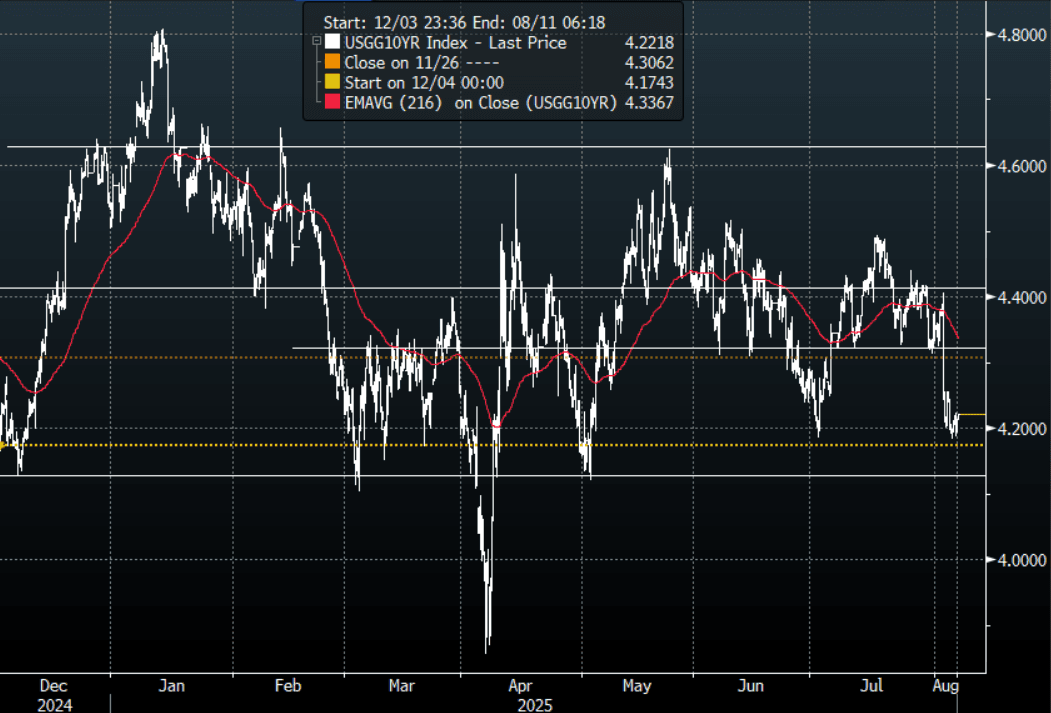

The TYU5 range has been 112-04 to 112-07 during the Asia-Pacific session. It last changed hands at 112-04, down 0-05 from the previous close.

- The US 2-year yield has edged higher trading around 3.726%.

- The US 10-year yield has moved higher trading around 4.222%, up 0.01 from its close.

- The 10-year yield had a powerful move lower in reaction to the NFP data, breaking below its 4.30% pivot within the wider range 4.10% - 4.65%. This now turns momentum lower in yields and you could expect buyers of treasuries on bounces back towards 4.30/35% now looking to initially test the 4.10% area.

- Bloomberg - “Trump said he’ll pick a successor for Adriana Kugler before the end of the week. He added that the replacement for Jerome Powell is down to four people and that Scott Bessent declined to be considered for the role.” - BBG

- The Department of the Treasury will auction $42 billion of August 2035 notes

- Bloomberg - “Bond traders are increasingly betting on up to 75 bps in Fed rate cuts in 2025 amid signs of a weakening US economy. The shift in sentiment follows soft payrolls data and stagnation in the services sector.”

- Truflation on X: “PCE close to 2%! All inflation metrics are falling. No more excuses. No more empty words. It's time to act, Powell.”

- Data/Events: MBA Mortgage Applications

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Bond Futures Drift Lower in the Morning Session

Jul-07 2025 04:06

- China's bond futures have drifted marginally lower in a lackluster trading session this morning despite a sizeable liquidity withdrawal from the OMO.

- The 10yr is down -0.01 to 109.10 to maintain its position above all major moving averages. The nearest being the 20-day EMA of 109.02

- The 2yr is down -0.01 at 102.50 and is between the 50-day EMA of 102.50 and the 20-day EMA of 102.49

- The CGB 10yr is at 1.64%.

- Wednesday sees the release of June PPI and CPI, which have both struggled to post positive outcomes in recent months.

RBA: MNI RBA Preview-July 2025: 25bps Cut Likely

Jul-07 2025 03:44

- The RBA is widely expected to cut by 25bps at tomorrow’s policy meeting. This is the sell-side consensus, albeit with a small number of economists expecting rates to be left on hold. Financial market pricing is also consistent with a 25bps cut. Our bias is also for a 25bps cut, which would take the RBA cash rate to 3.60% (still above neutral rates). If realized this would be 75bps worth of easing delivered so far in this cycle.

- Data towards the end of June, for May monthly CPI, should give the RBA confidence to cut. Headline inflation was close to the bottom end of the RBA’s 2-3% target band, whilst the trimmed mean eased to 2.4%y/y. Services inflation is still running at a stronger pace, but we continue to move off recent highs for this sub-sector of inflation.

- Some focus will be on the language the RBA uses and whether it considers a 50bps cut or not (assuming a 25bps cut is delivered). We feel the most likely scenario for the RBA board will be to consider holding steady or a 25bps cut. International risks are now arguably lower compared to the first part of Q2. This outlook can change quite quickly, but at the current juncture there are likely to be less fears around the global outlook.

- See this link for the full preview.

JGBS: Bear-Steeper Holds At Lunch, US Tariff Letters To Go Out Today

Jul-07 2025 03:17

At the Tokyo lunch break, JGB futures are slightly weaker, -6 compared to the settlement levels.

- Japan's weak wage data released Monday shows that it is becoming more difficult for the Bank of Japan to pursue interest-rate increases. Inflation-adjusted wages fell 2.9% on the year in May, compared with a 2.0% drop in April. With trade negotiations between the U.S. and Japan seemingly stuck and Washington threatening to impose even higher tariffs on Japanese goods, the economic outlook is "incredibly challenging," says Moody's Analytics economist Stefan Angrick. (DJ via BBG)

- Cash US tsys are flat to 3bps richer in today's Asia-Pac session after resuming trading following the long weekend.

- US President Trump has posted via Truth Social that the US will start delivering letters outlining tariff levels to various countries starting 12pm Monday, US eastern time. Trade deals will also be announced at the same time. Focus will be on tariff levels, particularly after Trump remarks late last week, where he stated tariff levels could be as high as 60-70% (although further details weren't provided).

- Cash JGBs are flat to 6bps cheaper across benchmarks, with a steeper curve. The benchmark 5-year yield is 0.7bp higher at 0.978% ahead of tomorrow’s supply.

- The swaps curve has bear-steepened, with rates 1-3bps higher. Swap spreads are generally tighter.