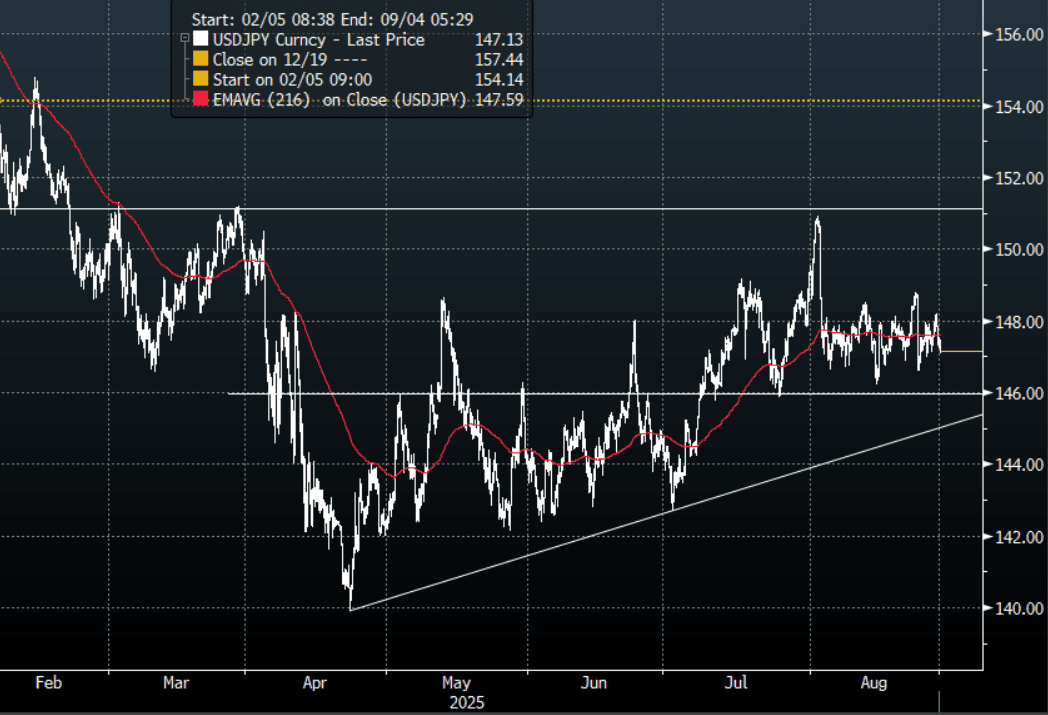

JPY: Asia Wrap - USD/JPY Drifts Back Towards 147.00

The Asia-Pac USD/JPY range has been 147.08-147.49, Asia is currently trading around 147.15, -0.20%. USD/JPY was capped by solid supply above 148.00 and when the USD demand was completed the pair proceeded to fall very easily again in the N/Y session. The demand towards 146.00 has been pretty solid all of July and August, keeping us for the most part in a 146.00-149.00 range. CFTC data for last week shows leveraged accounts again added to JPY shorts so they will be betting on the support continuing to hold. Should risk top out and have a deeper pullback this could create headwinds for cross-JPY.

- MNI BRIEF: BOJ's Nakagawa Sees Gradual Hikes; No Timing Hint. Bank of Japan board member Junko Nakagawa on Thursday backed a gradual rate hike but gave no guidance on the timing, citing high uncertainty. The remarks confirmed the BOJ’s economic and price outlook has remained unchanged since the July meeting.

- Offshore Investors Sell Japan Stocks For First Time Since June: Japan offshore investment flows were all negative last week, albeit with aggregate moves not large. Most notably were offshore investors selling nearly 500bn of local stocks. This was the first such outflow since mid June and indeed since early April we have only had two outflow weeks (including the latest observation)

- Futures Lower Post Poor 2yr Auction: The 2yr debt auction saw a bid to cover ratio of 2.84, the lowest since 2009. The tail from the auction, the gap between the average and lowest accepted prices, was higher at 0.022, versus 0.005 at the prior auction in late July. Note we have the 10yr debt auction on Sep 2, which is next Tuesday.

- Options : Close significant option expiries for NY cut, based on DTCC data: none.Upcoming Close Strikes : 145.00($1.17b Aug 29), 146.50($1.14b Aug 29), 147.50($806m Aug 29) - BBG.

- CFTC data shows last week asset managers have begun to add to their JPY longs after a consistent period of reduction +71379( Last +60866), leveraged funds though again used the dip to add to their newly built short JPY position -50848(Last -41257).

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

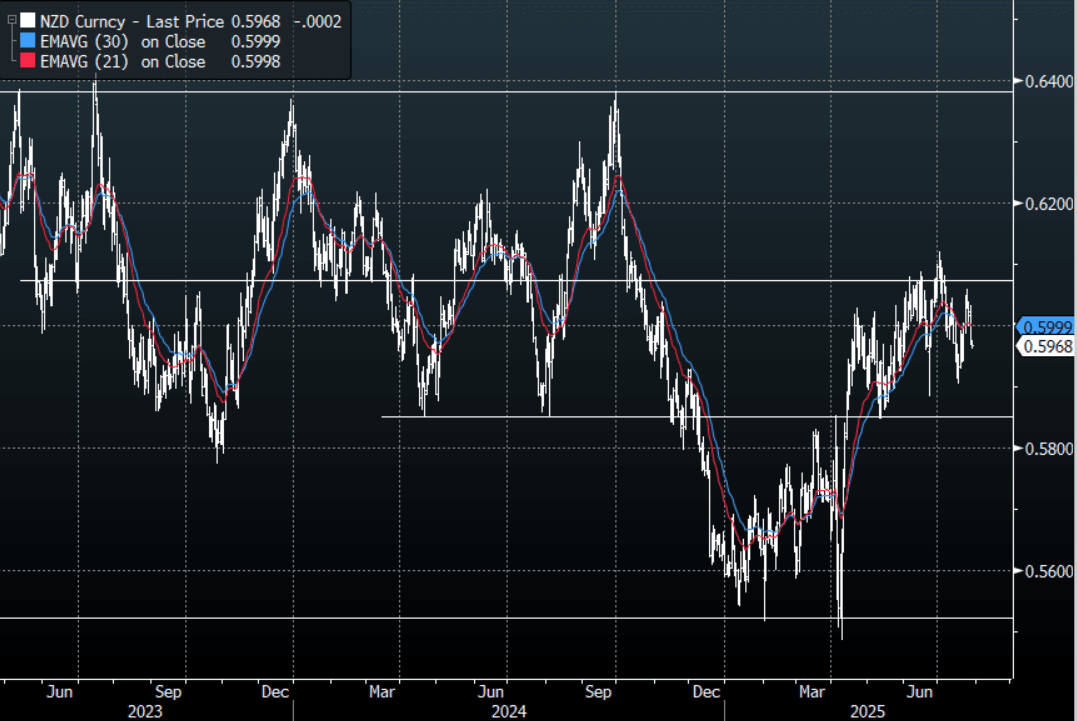

NZD: Asia Wrap - NZD/USD Fails Above 0.6000, Trades Heavy Into Month-End

The NZD/USD had a range of 0.5961 - 0.5976 in the Asia-Pac session, going into the London open trading around 0.5965, -0.08%. The pair could not hold onto its early gains yesterday and slid lower as the USD bounced strongly across the board. There is lots of event risk coming up this week and we are also heading into the corporate month-end today so there could be an extra demand for USD’s further pressuring the USD shorts. Support now seen back towards the 0.5850/0.5900 area.

- "NEW ZEALAND JUNE JOB ADS FALL 2.6% M/M: BNZ" - BBG

- "Job ads index fell 2.6% m/m following a revised 2% decline in May. Drops 2.8% y/y. After a year of relative stability, ads are again on a downwards trajectory: BNZ. “Consistent with the decline in job ads, we expect total employment fell modestly and the unemployment rate climbed to 5.3%” in 2q.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6000(NZD395m July 30), 0.5965(NZD424m July 31). - BBG

- CFTC Data shows Asset Managers again reduced their newly built longs in NZD +5034(Last +8192), the Leveraged community added slightly to their shorts last week -7328(Last -6744).

- AUD/NZD range for the session has been 1.0912 - 1.0930, currently trading 1.0928. Dips back to 1.0850/1.0900 should continue to find support as the pair tries to build momentum to move higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

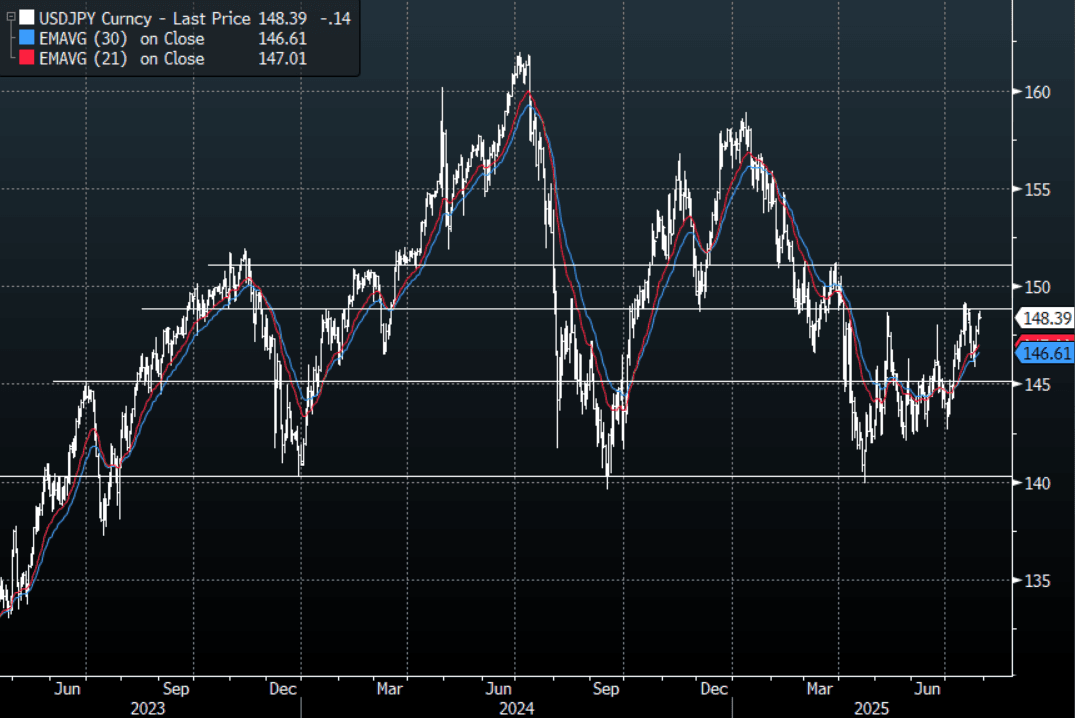

JPY: Asia Wrap - USD/JPY Consolidates On A 148 Handle, Eyes July Highs

The Asia-Pac USD/JPY range has been 148.29 - 148.71, Asia is currently trading around 148.45, -0.05%. USD/JPY continued to build on its momentum higher as the USD shorts reduce risk heading into an important week for risk. Corporate month-end today will add to the headwinds for the USD shorts. A move back above the highs for July would turn the focus towards the pivotal 151.00/152.00 area.

- The Japan Times via BBG - “In an annual white paper on Tuesday the government underlined the need to take all possible measures to realize wage increases that outpace inflation. In an annual white paper on Tuesday the government underlined the need to take all possible measures to realize wage increases that outpace inflation.”

- "X-BOJ DEPUTY GOVERNOR NAKASO: DOLLAR TO RETAIN SUPREMACY AS KEY GLOBAL CURRENCY BUT 'CRACKS' APPEARING AS INVESTORS DIVERSIFY INTO OTHER CURRENCIES. BOJ LIKELY TO RESUME INTEREST RATE HIKE IT RESTORES CONFIDENCE THAT ECONOMY, INFLATION WILL MOVE IN LINE WITH PROJECTIONS. BOJ MUST BE VIGILANT TO UPSIDE RISKS TO INFLATION AS RISING FOOD PRICES COULD LEAD TO OVERSHOOT IN INFLATION EXPECTATIONS" RTRS

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.65($823m).Upcoming Close Strikes : 149.00($1.16b July 30), 147.00($1.52b Aug 1), 146.00($1.43b Aug 1) - BBG.

- CFTC data shows Asset managers surprisingly added slightly to their JPY longs +72326( Last +71610), while leveraged funds have slightly reduced their newly built short JPY position -11571(Last -12606).

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Sentiment Mostly Weaker Ahead Of Key Event Risks

Most regional Asia Pac markets are down in the first part of Tuesday trade. Losses aren't large, but outside of South Korea and Malaysia, trends are negative throughout the region. This follows and overnight session where US markets modestly outperformed EU weakness. So far today, US equity futures are modestly higher, with Nasdaq futures slightly outperforming. This comes ahead of month end late this week.

- Earlier remarks from US Commerce Secretary Lutnick stated that Trump is considering a few deals before the Aug 1 deadline, he will then decide on the unilateral tariff rate. Lutnick stated that an extension of trade truce was likely in terms of the current meetings under with China officials. Trump also pushed back on the idea he was pursuing a summit with China President Xi.

- The China CSI 300 is off a touch, but still close to recent highs. The HSI is down around 1%, but still above the 25300 level. Japan markets are also weaker, the Topix off close to 0.85%. Proximity to earnings outcomes and the Fed decision/data is being cited as a headwind for these markets.

- Taiwan's Taiex is down around 0.85% as well, after a strong run higher in recent weeks. The Kospi is bucking these trends, up nearly 0.60% and firmly above the 3200 level. Earlier we had headlines of corporate tax increases and changes to the capital gains tax, but these shifts have been flagged in the local media prior to today, which may be limiting the market impact.

- In South East Asia, most markets are down, except for Malaysia. Losses are modest though at this stage. Thailand markets have returned, unable to build on recent positive momentum. Thailand has accused Cambodia of violating the recent ceasefire agreement, while a meeting between the countries respective militaries has been postponed.