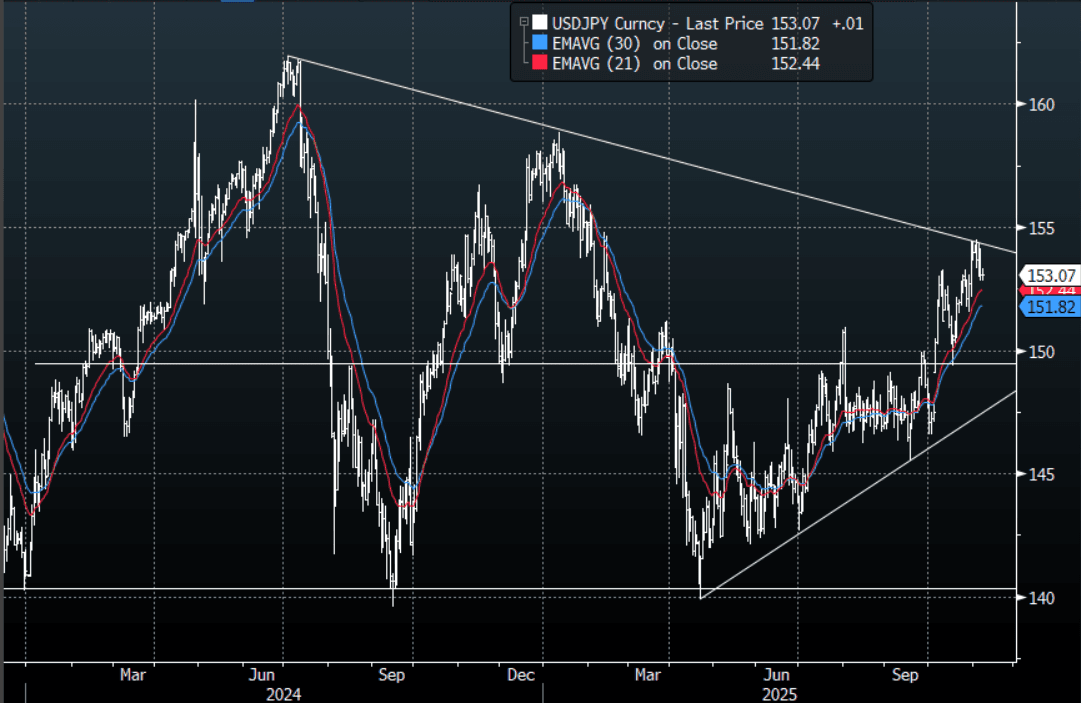

JPY: Asia-Pac: USD/JPY Consolidates Around 153.00

The USD/JPY range today has been 152.82 - 153.31 in the Asia-Pac session, it is currently trading around 153.10, +0.05%. The pair failed overnight again above the 154.00 area as cross-Yen came back under pressure as risk turned lower again. A lot depends on what your view is for risk from here, but the price action of the last few days signals we could be putting in a potential top and if a correction in risk plays out then I suspect the resistance around the 154/155 area should continue to offer solid resistance. With the crosses under pressure we could see some further pullbacks and therefore I suspect rallies on the day toward 153.50 should find better sellers, but I do think any correction lower will still find buyers happy to fade. The first buy zone is toward 151.50-152.00 and then the more important 149.00-150.00 area.

- MNI AU - Sep Household Spending Below F/Cs, Focus To Get Real Wages Higher: Japan Sep real household spending data was softer than forecast. Real spending fell 0.7%m/m, against a -0.1% forecast (per Rtrs). In y/y terms we were up 1.8%y/y, against a 2.5% forecast. Given generally softer cash earning outcomes in recent months some moderation in spending was not a surprise. The authorities focus will remain on returning cash earnings growth to real positive territory as without that we may see spending trends soften as we progress towards year end and into 2026.

- Options : Close significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : none - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Tech Rally Takes A Breather

Asia Pac equities are mixed, with some caution coming through in tech/AI related space. Hong Kong markets have returned weaker, with the HSI down over 1%, tracking lower for third straight session. The tech sub index off over 1.1%. We did see US tech related bourses underperform in US Tuesday's trade, while the Golden Dragon index lost 2.24%. Note onshore China markets return tomorrow.

- Reuters also noted: "U.S. lawmakers are calling for broader bans on chipmaking equipment to China after a bipartisan investigation found that Chinese chipmakers had purchased $38 billion of sophisticated gear last year." This has potentially weighed on China tech related plays in Hong Kong.

- BBG also notes Citigroup analysts who stated that Golden Week box office results were below expectations (hurting sentiment in this space).

- Taiwan's Taiex is off around 0.50%, but still 2700, so close to recent record highs. Even with this recent run higher, offshore investors have only added modestly to local stocks, (but regional holidays, with China and South Korea still out may be a factor).

- In South East Asia, trends are mixed. Indonesia went to a fresh record high, but is now tracking modestly lower. Onshore government bond yields continue to fall, amid the dovish BI outlook, while consumer sentiment data for Sep fell to fresh lows since 2022.

- Thailand stocks are up ahead of an expected BoT cut later (last 0.55%). We also stimulus measures (0.3-0.4ppts of GDP) announced yesterday to boost consumption (via BBG).

- NZ stocks are outperforming Australia, after the 50bps RBNZ cut surprised the market.

OIL: Crude Continues Trending Higher Ahead Of EIA Data & Fedspeak

Oil prices continued trending higher during today’s APAC session with little news to give them direction. US industry-based data showed product drawdowns and the market continues to monitor strikes on Russian energy infrastructure which are impacting refining rates. For now the US EIA’s forecast of higher non-OPEC output and lower prices has been looked through but the IEA’s report is not until 14 October.

- WTI is up 0.9% to $62.28/bbl after rising to $62.36 and Brent is 0.8% higher at $65.95/bbl following a peak of $66.04. Both benchmarks are up around 2.2% since the weekend’s cautious OPEC decision.

- Official EIA oil data will still be released Wednesday as the agency is continuing to publish for now despite the US government shutdown. Bloomberg reported mixed industry-based data with oil inventories building but falling at key hub Cushing last week, according to people familiar with the API data. The reported product drawdown has likely provided support to prices today ahead of the EIA data.

- A soft outlook was reflected in the EIA’s October report as it is forecasting global oil inventories to build through next year pushing Brent down to $52/bbl from $62 in Q4 2025. Global output rises across its forecast horizon driven by non-OPEC. It doesn’t believe OPEC will be able to achieve its higher production targets helping to support prices.

- Later the Fed’s Musalem, Barr, Goolsbee, Kashkari and the ECB’s Lagarde, Elderson, Buch, Tuominen and BoE’s Pill speak. The September FOMC meeting minutes will also be published.

MNI EXCLUSIVE: Former BoJ Chief Economist On The Policy Rate Outlook