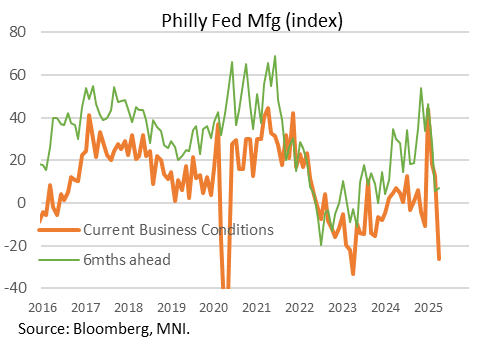

US DATA: April Philly Fed Survey Flashes Recession Signals

The Philadelphia Fed's Manufacturing Business Outlook Survey general business conditions index fell to -26.4 in April, a much bigger decline than expected (2.2 survey, 12.5 prior). The 38.9 point drop in the index has only been exceeded twice since 2000: October 2008, and March / April 2020 - both recessionary periods.

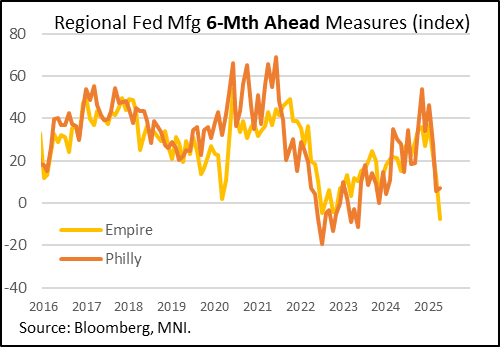

- The survey as a whole roughly translates to an ISM manufacturing print in the low 40s - deeply contractionary, and an even weaker than the earlier Empire State reading for April which was very weak in its own right. It may over-exaggerate negative sentiment - survey responses were collected from April 7 - 14, so just after the "Liberation Day" reciprocal tariff announcement, and amid the 90 day "pause" announcement on April 9 that may have relieved uncertainty for some manufacturers but increased it for others.

- Weakness was evident across the board: new orders collapsed to -34.2 vs positive 8.7 prior, lowest since April 2020 and outside of that, the worst figure since March 2009 (global financial crisis).

- Employment dropped to 0.2, after a promising 19.7 the prior month. Shipments were -9.1, down from positive 2. All of these are substantially lower than they were just 3-4 months prior.

- Inflationary conditions worsened too: prices paid rose to 51.0 (48.3 prior) for the highest level since July 2022, with prices received up 1 point to 30.7 (just below the recent high).

- If there was any good economic news in the report it is that forward looking expectations have stabilized, with the 6-month ahead outlook rising for the 1st time in 3 months to 6.9 from 5.6 prior - but these are still very subdued levels and may reflect the notion that the outlook can't get much worse.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US FEB INDUSTRIAL PROD +0.7%; CAP UTIL 78.2%

- MNI: US FEB INDUSTRIAL PROD +0.7%; CAP UTIL 78.2%

- US JAN IP REV TO +0.3%; CAP UTIL REV 77.7%

- US FEB MFG OUTPUT +0.9%

US DATA: Pickup In Import Prices Not Yet Worrying, But Just Beginning

Import price inflation was stronger than expected in February, printing 0.4% M/M (0.0% consensus, 0.4% prior after +0.1pp rev), while ex-petroleum import inflation also exceeded expectations at 0.4% (0.2% consensus, 0.1% prior unrev).

- That left overall import prices up 2.0% Y/Y (1.6% expected, 1.8% prior), just the second 2-handle since 2022 in another sign that benign annual base effects are wearing off (the low was -6.1% in Jun 2023).

- And ex-petroleum Y/Y returned above 2% for a 4th month in 5 after dipping to fell to a 5-month low (when unrounded) 1.8% in January.

- There isn't much evidence of tariffs and/or tariff front-running in the aggregate changes: nonfuel industrial supplies and materials inflation rose by the most (8.0%) Y/Y since Aug 2022, this is in the context of a steady increase as opposed to a sudden jump in February.

- That being said, manufactured goods prices from China (where additional tariffs applied in February) jumped 1.4% M/M in the month, albeit remain fairly flat on a Y/Y basis. Overall consumer goods import prices were slightly negative (ex-autos) Y/Y.

- That being said, with a higher set of tariffs to be implemented in the coming months across geographies, we would expect core import prices to rise much further. The overall effect will be to boost pipeline price pressures and core goods inflation over the coming months, exacerbating the existing upward trend in the latter (see chart).

- The data also offer the final input into February core PCE: import air passenger fares rose 3.4% M/M, which is in the middle of the range of previous February increases, suggesting that once seasonally-adjusted for PCE purposes it should not be too far out of line. As such we have no reason to believe analysts will adjust their core PCE forecasts for the month from the existing consensus of around 0.33% M/M.

US SWAPS: Little Changed To Marginally Tighter On The Day After Run Of Widening

Swap spreads little changed to a touch tighter today, with modest narrowing in the German equivalents a potential factor ahead of the German fiscal reform voting process.

- Note that long end U.S. swap spreads have widened for 5 consecutive sessions as of yesterday’s close.

- Hope for deregulation in the financial sector has been front and centre, on the back of intensification surrounding and ultimate delivery of the nomination of Fed Governor Bowman for the Vice Chair for Supervision role.

- 10- & 30-Year swap spreads are ~5bp off their respective ’25 highs, which were mostly driven by a previous round of speculation surrounding Bowman’s potential nomination.

- Note that Treasury Secretary Bessent has previously pointed to the SLR providing a binding constraint to Treasury trading, also factoring into regulatory reform hope/Bowman’s nomination.