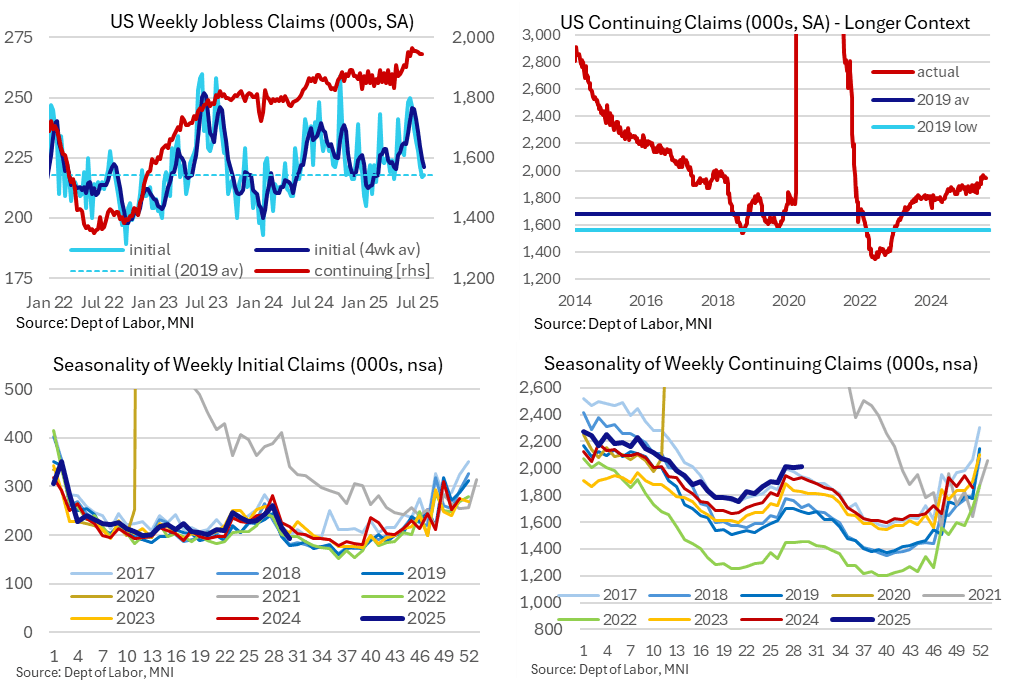

US DATA: Another Set Of Better Jobless Claims Data

Initial jobless claims surprised lower again in data up to last week as they trend closer to average levels in 2019, a period when the unemployment rate was 40-50bps lower than current levels. Continuing claims meanwhile are very slowly edging lower after a quick climb through May-June. The combination continues to support the “low fire, low hire” categorization of the labor market, with greater emphasis on the former in the past couple weeks.

- Initial jobless claims were lower than expected at 218k (sa, cons 224k) in the week to Jul 26 after an unrevised 217k.

- The four-week average continues to moderate, most recently hitting 221k (-4k) having recently peaked at 246k in mid-June.

- As such, initial jobless claims are roughly tracking at average levels in 2019 despite the population growth seen since then. 2019 was a period of previous labor market tightness during which the unemployment rate averaged 3.7% vs the 4.12% in June and the 4.2% expected in tomorrow’s July release.

- Continuing claims were also lower than expected at 1946k (sa, cons 1953k) in the week to Jul 19 after a downward revised 1946k (initial 1955k).

- That downward revision also sees a slightly more favorable figure when comparing payrolls reference periods, with the 1946k vs 1964k in June after 1907k in May and 1833k in April.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SONIA OPTIONS: Call Spread seller

SFIZ5 96.20/96.30cs, sold at 7 in 8k.

EURIBOR OPTIONS: Large Ratio Call Spread vs Put

ERU6 98.68/98.87cs x4.5 vs ERU6 98.25p x0.5, bought the cs for flat in 36k x 4k.

EUROPEAN INFLATION: M/M SA Services Inflation Still Above Q1 Average

Eurozone core inflation rose 0.27% M/M on a seasonally adjusted basis according to ECB data, up from -0.07% prior. Services prices rose 0.41% M/M (vs -0.14% prior), while non-energy industrial goods prices rose 0.03% M/M (vs 0.04% prior).

- The June inflation data was seen as a cleaner month to gauge underlying services inflation pressures, with April and May readings influenced by the timing of Easter and seasonal adjustment methodologies struggling to account for such calendar effects.

- In this light, the 0.41% M/M sequential reading was above the Q1 average of 0.29% and the 2024 average of 0.33%. From this perspective, there appears to still be some stickiness lurking in services prices. The final June inflation data on July 17 will shed more light on whether this is the case.

- 3m/3m annualised services inflation momentum was 4.07%, up from 4.00% in May and 4.06% in April.

- 3m/3m core inflation momentum was 2.66% Y/Y (vs 2.68% prior), but remains above March’s 2.34% Y/Y reading.

- ECB speakers continue to express confidence in the broader inflation outlook though. This morning, Bundesbank President Nagel said that “in the current situation, we are in calm waters”, with a similar rhetoric coming from Vice President de Guindos.