CHILE: Analysts Share View That BCCh Has Room to Cut Policy Rate This Month

Dec-05 13:35

- Front-end camara swap rates have edged lower following today’s benign CPI inflation data which look to have reinforced expectations of a new 25bp policy rate cut by the BCCh later this month. Following soft CPI data last month as well, the stabilisation of ex-volatiles inflation around 3.4% should ease BCCh concerns over persistent core CPI pressures. 1y swap rates have fallen by a further 5bp today, taking the move lower over the last month to more than 15bp.

- Goldman Sachs writes that consumer prices have printed welcome readings over the last four months and they expect inflation to end the year at 3.6% y/y, notably below the BCCh’s 4.0% forecast. They also expect core inflation to end the year 0.2-0.3pp below the central bank’s 3.7% estimate. As such, they see a 25bp cut this month, followed by another one in Q1 2026 to a terminal rate of 4.25%.

- Similarly, JP Morgan says that the backdrop appears favourable for another interest rate reduction and, barring any major surprises in the Dec 14 election run-off, they expect a 25bp move on Dec 16.

- Santander also believes that with activity evolving in line with the central scenario of the latest IPoM and inflation showing a reduction in risks, the BCCh has room to deliver a cut this month.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOE: MNI BOE Preview - November 2025: It's All About Bailey

Nov-05 13:34

For the full MNI BOE Preview click here

- Thursday's MPC decision is far from certain - indeed we would categorise our own view of the outcome as 50/50 between a 25bp cut and a hold.

- We look at the drivers for each members' vote and the key data since the last meeting / August forecasts.

- In essence, we think a 5-4 vote is the most likely outcome but that it could deliver a cut or a hold. Governor Bailey's vote will be the deciding factor here, in our view.

- We have also summarised over 20 sellside previews.

US: November Refunding: Starting To Considering Futures Increases To Coupon Size

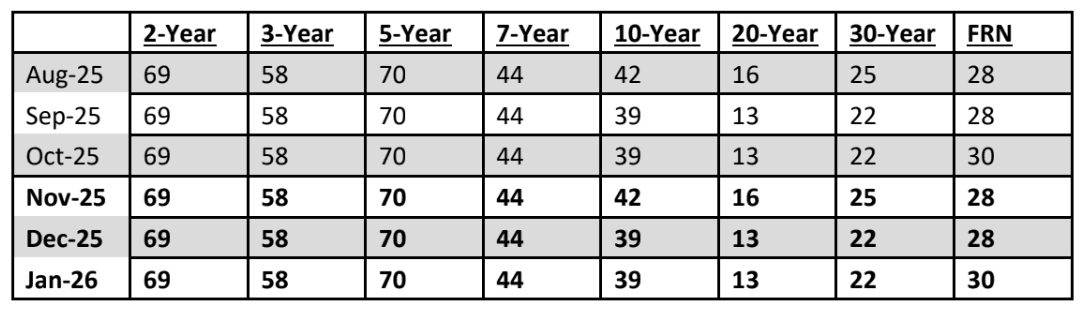

Nov-05 13:31

- Treasury left nominal Treasury coupon auction sizes unchanged for a 7th straight quarter and kept guidance that it anticipates maintaining coupon sizes for "at least the next several quarters."

- New added guidance hints that an increase is coming: "Looking ahead, Treasury has begun to preliminarily consider future increases to nominal coupon and FRN auction sizes, with a focus on evaluating trends in structural demand and assessing potential costs and risks of various issuance profiles."

- Refunding will be $58B in new 3Ys, $42B in new 10Y, and $25B in new 30Y next week, as expected.

- Bill offerings will be maintained through late November, then Treasury will implement modest reductions to short-dated bill auction sizes in December and increase auction sizes again by the middle of January based on expected fiscal inflows and outflows.

- TBAC was mixed on how Treasury should approach adjustments to its current forward guidance and said that current projections could warrant increases in coupon issuance in FY2027.

- Discussing the pressure on short-term interest rates in October, TBAC concluded it is both a supply/collateral story and a demand/reserves story. It recommended Treasury better communicate the need to keep a large TGA balance.

The below table shows the actual auction sizes for the August to October 2025 quarter and the anticipated auction sizes for the November 2025 to January 2026 quarter, in billions of dollars.

STIR: ADP Provides Limited Hawkish Adjustment In Fed Pricing

Nov-05 13:28

Modest hawkish reaction in the USD front end following the fairly limited upside surprise in the ADP employment reading and small revision to the prior reading.

- Relatively modest deviation in the print/revisions and the headline being quite close to the level implied by the weekly data help explain the limited follow through.

- FOMC-dated OIS now pricing 17bp of easing for Dec, 26bp through Feb, 35bp through March and 41bp through April, ~0.5bp less dovish vs. pre-data levels.

- SOFR-implied terminal rate pricing at 3.10% vs. 3.09% pre-data.