US OUTLOOK/OPINION: Analysts Mixed On Control Sales;Eye Restaurant Spending(2/2)

Below is a diversity of analyst outlooks for the June advance retail sales report - listed from highest to lowest on June Control Group retail sales expectations. Note that, as pointed out in our preview, there is broad expectation that Control Group growth will exceed that of headline retail sales. We also note mixed opinions on food services/drinking places spending, which is not in the Control Group category:

- BofA: (0.7% headline, 0.9% Control Group): "Tariffs might have contributed to the strength in retail spending in June. But real spending should still be robust if our June forecast is correct. Investors should keep an eye on the food services category to assess whether tariffs are weighing on discretionary services...retail spending was more robust in June in the BAC card data, rising 0.7% m/m SA. In fact, spending growth picked up in all major retail sales categories that we report. The biggest increases were in gas (due to higher prices), general merchandise, clothing, home improvement and groceries."

- Citi (0.4% headline, 0.5% Control Group): "Retail sales have been weaker in the last two months after a strong increase in March, mainly reflecting front loading and then normalization in auto sales likely due to the implementation of auto tariffs. Overall Q2 consumption growth should be stronger than in Q1 but slower than the pace of consumption growth last year... We pencil in roughly flat auto sales... Restaurant spending the only services category in the retail sales report could rebound somewhat in June after falling in May, but we see downside risk... another ~1%MoM increase in non-store sales. If consumer goods prices start to pick up more in June data and in coming months, it will be important to look at real goods spending for a better sense of the real growth trajectory. We expect further slowing in real consumption growth in the second half of the year."

- Deutsche (0.2% headline, 0.3% Control Group): "Should our forecast for retail control end up close to the mark, the series would be up 3.6% annualized for Q2, down slightly from 3.8% annualized in Q1 and in line with our forecast for Q2 real PCE growth of 2.5%.

- Wells Fargo (0.0% headline, 0.3% Control Group): "We believe the control measure may overstate the strength of underlying spending today. Only half of all retailers reported a pickup in sales activity last month, which suggests tariffs may be negatively affecting consumer behavior...Some positive payback [in auto sales] may be forthcoming, given recent signs of a pickup in auto sales. Meanwhile, ecommerce sales, another large category, continues to outperform and offset weakness elsewhere."

- TD Securities: (0.1% headline, 0.1% Control Group): "Our forecast assumes a less acute m/m contraction in auto sales along with a rebound in sales at gasoline stations. However, we expect a moderation in control group sales to 0.1% m/m from 0.4% previously. We expect that the only services category, sales at food services and drinking places, will rebound sharply to a 1.0% m/m gain after declining 0.9% m/m in May. Note that retail sales is largely goods spending and only translates to less than a third of monthly personal spending as calculated by the BEA."

- UBS (-0.2% headline, 0.2% Control Group): "we expect the only component of the retail sales report which captures services spending — sales at food services and drinking places — to be soft again in June...We expect retail and food services sales fell in June, held down by autos, light trucks and sales at gas stations. Sales at the control group of stores we expect fares better and moves up 0.2% in June. Often though, revisions can be the bigger signal. Real consumer spending has been relatively weak thus far this year, down year-to-date in real terms and running just 1.2% annualized over the last four months. That should smooth through any pull-forward due to tariffs as well. Despite the upbeat narrative, the hard data does not look that great."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Instant Answers For June FOMC Meeting

The Instant Answers questions that we have selected for the June FOMC statement and projections are as follows (due to be released at 1400ET Wednesday):

- Federal Funds Rate Range Maximum

- Number of dissenters on size of rate move

- Median Projection of Fed Funds Rate at End of 2025

- Median Projection of Fed Funds Rate at End of 2026

- Median Longer Run Projection of Fed Funds Rate

- Number of 2025 Dots > 4.375%

- Number of 2025 Dots > 4.125%

- Number of 2025 Dots > 3.875%

- Number of 2025 Dots < 3.875%

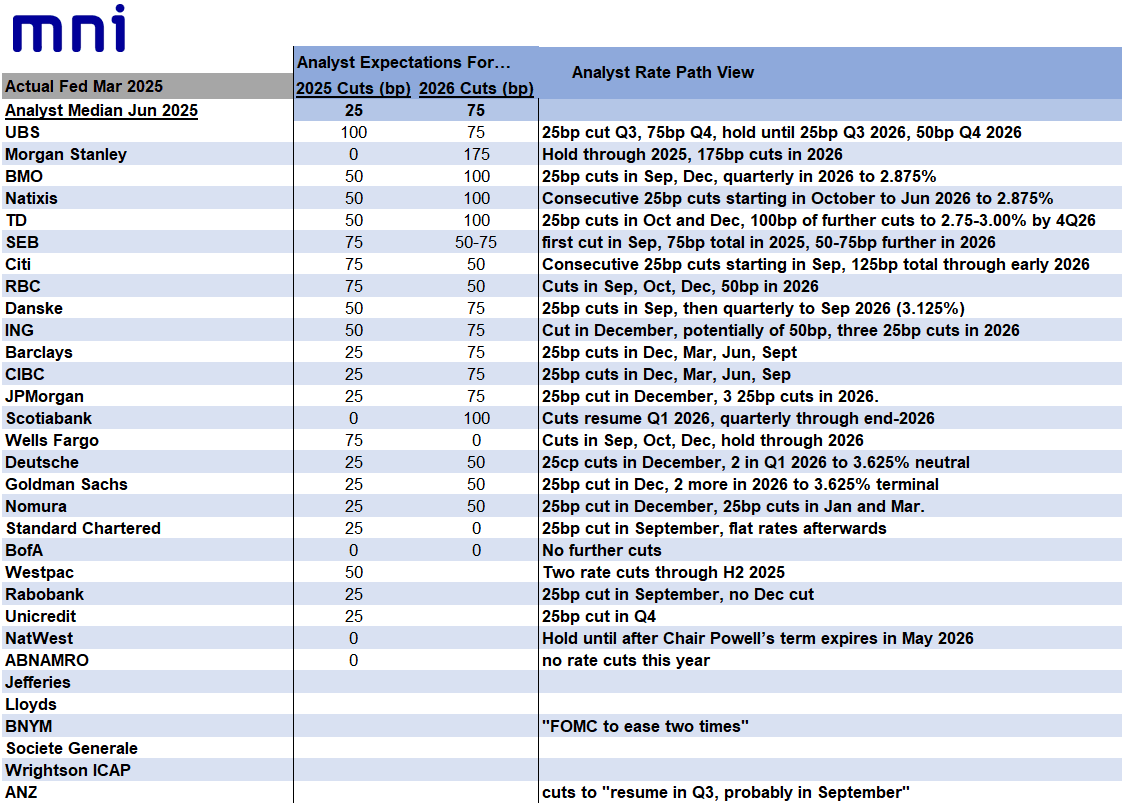

FED: Analysts See 0 To 100bp Of Cuts This Year, Up To 175bp Through 2026 (2/2)

Going into the June FOMC meeting, the median analyst is forecasting the Fed to deliver just 1 cut this year for 25bp of easing, but there is a wide range of opinions which includes 100bp of cuts (UBS) to zero (multiple). See table below.

- Opinion is accordingly split among most analysts about whether the next cut is in September, October, or December.

- The median analyst expectation is for 75bp of cuts in 2026, though again this ranges from no cuts to 175bp of easing (Morgan Stanley).

- The median analyst who has forecasts through both years sees 112.5bp of cuts, or between 4-5.

- UBS and Morgan Stanley see the most total easing (175bp), while BofA sees no further cuts.

US OUTLOOK/OPINION: Macro Since Last FOMC: Labor - Wages Surprise Hotter

- On the flip side, wage growth has also started to come in hotter. We wouldn’t put too much weight on the surprisingly strong 0.42% M/M increase in average hourly earnings in May in isolation but it followed a strong 6.6% annualized increase in unit labor costs in Q1 (strongest since 1Q24 and before that 3Q22).

- Productivity growth played a role here, falling -1.5% annualized for its first decline since 2Q22 after a period of some particularly strong gains, but the underlying wage growth series was still strong.

- Whilst Powell has previously said he doesn’t expect inflationary pressures to come from the labor market, wage growth is starting to warrant closer inspection.