US DATA: An In-Line Existing Home Sales Report

Oct-23 14:30

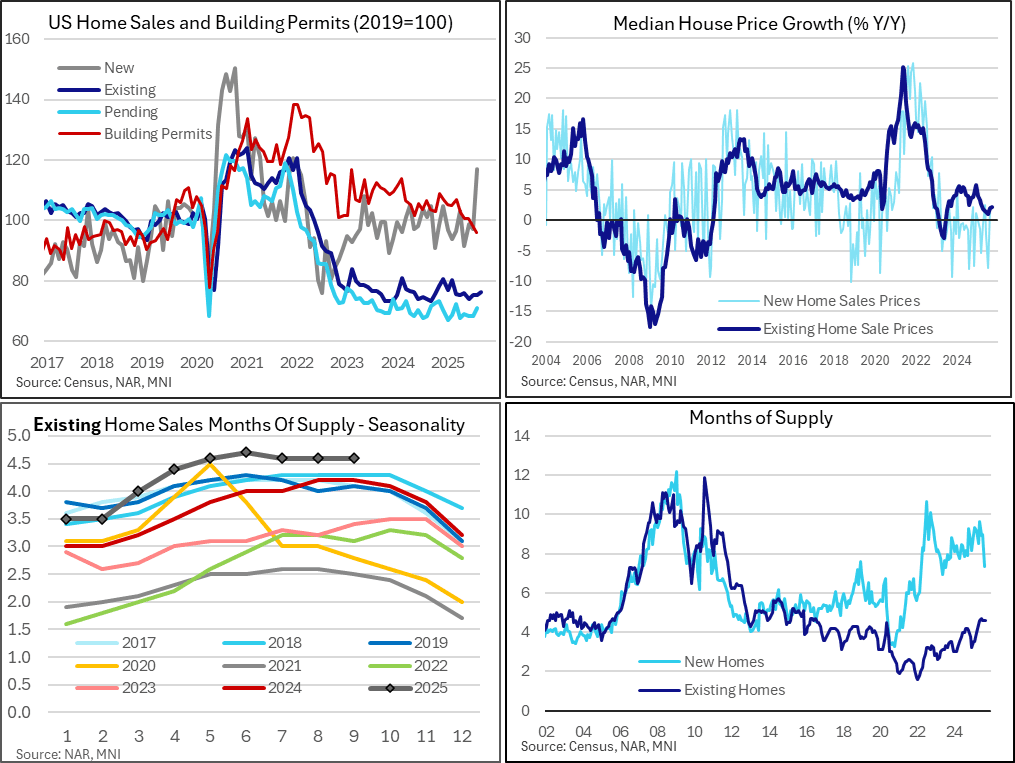

There were no surprises in the September existing home sales report, with sales nudging higher but still depressed. Relative supply remained high by recent year standards but not historically so, whilst median house price growth remained mild at ~2% Y/Y.

- Existing home sales were completely as expected as they nudged up to 4.06m (saar) in September after an unrevised 4.00m in August, for a 1.5% M/M increase.

- It holds what has been a narrow range close to lows for months now with an average of 4.01m since May.

- For context, the recent low of 3.90m in Sep 2024, which it came close to again with 3.93 back in June, was lowest since 2010. Current sales are running at ~75% of 2019 levels in continued signs of a depressed market.

- Factor in inventories and relative supply tells a similar story to recent months; high by post-pandemic standards and a few years prior the pandemic but low compared to the glut in the lead up to the GFC.

- Specifically, the 4.6 months in September compares with 4.2 in Sep 2024 (the same relative difference to the August Y/Y comparison) and 4.2 in Septembers in 2017-19 for a pre-pandemic comparison.

- There were little new developments in house price dynamics, with the median price rising 2.1% Y/Y. House price growth has averaged 2.2% Y/Y in the ytd after 4.5% in 2024 and 1.1% in 2023 followed the booming 10.5% in 2022, 18% in 2021 and 9% in 2020.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB OPTIONS: Schatz Call Spread Seller

Sep-23 14:27

DUZ5 107.00/107.30cs 1x2, sold at 4 and 3.75 in 5k.

EGB SYNDICATION: New 8-year OT / 3.625% Jun-54 OT tap: Priced

Sep-23 14:12

New 8-year OT

- Reoffer: 99.391 to yield 2.961%

- More to follow

- Spread: MS+37bps (guidance was MS+39bps area)

- Issue size: E3.5bln (a little higher than the E3bln MNI expected)

- Books closed in excess of E46bln (in E1.85bln JLM interest)

- HR 100% vs 2.60% Aug-33 Bund. Ref: 100.10 / +37.6bp

- Maturity: 14 October 2033

- Coupon: 2.875%, Long First

- ISIN: PTOTEQOE0023

- Timing: TOE 14:41BST / 15:41CET. FTT immediately

3.625% Jun-54 OT:

- Reoffer: 92.929 to yield 4.045%

- More to follow

- Issue size: E1.5bln (the middle of the E1-2bln range MNI expected)

- Books closed in excess of E35bln (in E875mln JLM interest)

- HR 97% vs 2.50% Aug-54 Bund. Ref: 84.76 / +71.6bp

- Spread: MS+110bps (guidance was MS+112bps area)

- ISIN: PTOTE3OE0025

- Timing: TOE 14:42BST / 15:42CET. FTT immediately

For both:

- Settlement: 30-September-2025 (T+5)

- Bookrunners: Barclays(B&D/DM)/BNPP/CAIXABI/CITI/CACIB/JPM

From market source / MNI colour

MNI EXCLUSIVE: Riksbank Governor Speaks to MNI

Sep-23 14:09

Riksbank Governor Erik Thedeen talks to MNI about the outlook for the policy rate and the central bank's balance sheet.- On MNI Policy MainWire now, for more details please contact sales@marketnews.com