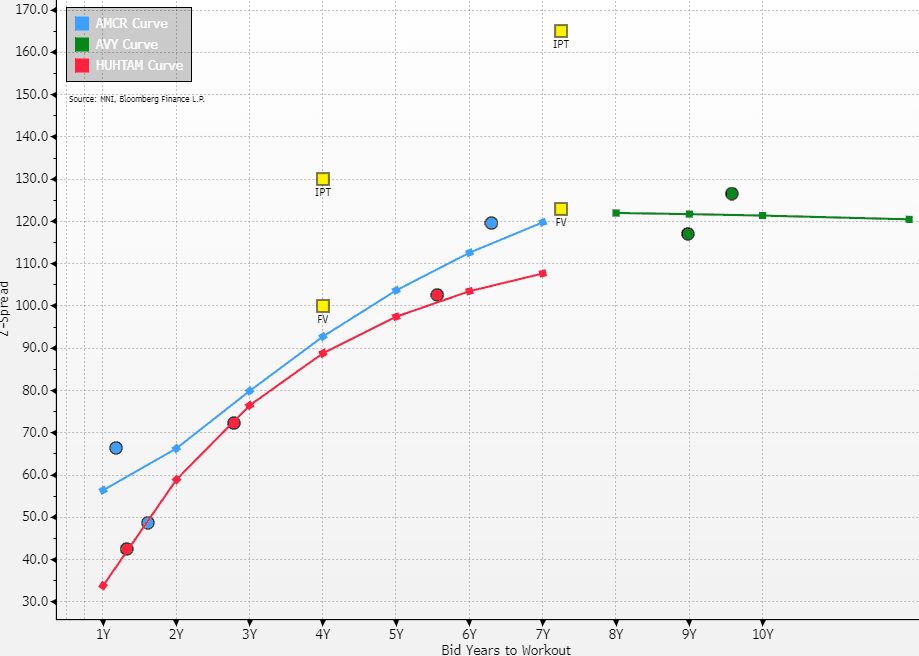

EU BASIC INDUSTRIES: Amcor: New Issue FV

(AMCR; Baa2/BBB/BBB+)

- MNI FV: MS+107a, MS+123a.

- IPT: EUR Benchmark 4Y MS+130a, EUR Benchmark Long 7Y MS+165a (market sources).

- Secondary is currently quoted up to 3bp wider, despite the earlier mandate announcement.

- We viewed recent results as marginally positive https://mni.marketnews.com/4nT2kqx.

AVY looks most interesting in the sector on RV, but we are positive on AMCR also. The sector is showing signs of stabilising and with the Berry merger integration progressing it should be able to delever as planned. Secondary is trading ~10bp wide to HUHTAM, upgraded to BBB- only this year.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Futures Through Next Resistance

{GB} GILTS: Gilts have rallied a little after trading either side of unchanged around the open, futures last +14 at 91.30, piercing resistance at 91.28.

- A fresh extension higher would expose more meaningful resistance at 91.82

- Yields 1-2bp lower, curve bull steepens.

- The impact of hope surrounding the potential for a moderation in Sino-U.S. trade tensions has worn off in recent trade, with gilts outperforming vs. Bunds by ~1bp.

- Fiscal headlines remain front and centre domestically.

- The IFS has noted that “It would be difficult, but not impossible, for the Chancellor to raise tens of billions of pounds more revenue without breaking Labour’s manifesto promise”:

- We have covered the remainder of the major fiscal stories from the weekend in another bullet.

- SONIA futures flat to +4.0, BoE-dated OIS prices ~6bp of easing through year-end, which we believe underestimates the odds of a Q4 cut.

- BoE’s Greene & Mann will speak later today.

- More focus will be placed on the labour market data & comments from BoE Governor Bailey (both due Tuesday).

EGBS: Bund Futures Testing Friday's High With Trade Uncertainty Back In Focus

Bund futures have drifted higher through the morning, now testing Friday's high at 129.41 (+10 ticks today). Despite the White House's softened weekend stance with respect to China tariffs, trade policy uncertainty is back in focus.

- A bullish theme in Bund futures is intact, with attention on key resistance at 129.44 (Sep 10 high). Clearance of this hurdle would pave the way for a climb towards 129.58, a Fibonacci retracement point.

- The German curve has bull steepened, with Schatz yields down ~2bps and 30-year Bund yields down ~1bp.

- A reintroduction of trade policy uncertainty and increase in US/China tariffs would have dovish implications for the ECB. Such an outcome would compromise recent optimism around the growth outlook and potentially renew concerns around disinflationary Chinese trade diversion. ECB officials will want to see how the situation evolves in the coming weeks, with focus also on the heavy regional data calendar towards the end of this month.

- 10-year EGB spreads to Bunds have moved away from early lows, with BTPs and OLOs now the only bonds trading narrower on the session.

- Markets remain sensitive to French headline flow. Lecornu's reappointment as PM is unlikely to reduce medium-term fiscal/political challenges facing France, so scope for meaningful OAT/Bund tightening still appears limited. OATs currently underperform peers, with the 10-year spread to Bunds +0.5bps at ~84bps.

- This week’s regional data calendar is light, headlined by final September HICP readings.

EQUITY OPTIONS: EU Bank Put Spread

SX7E (17th Oct) 210/200ps, bought for 0.10 and 0.15 in 9k.