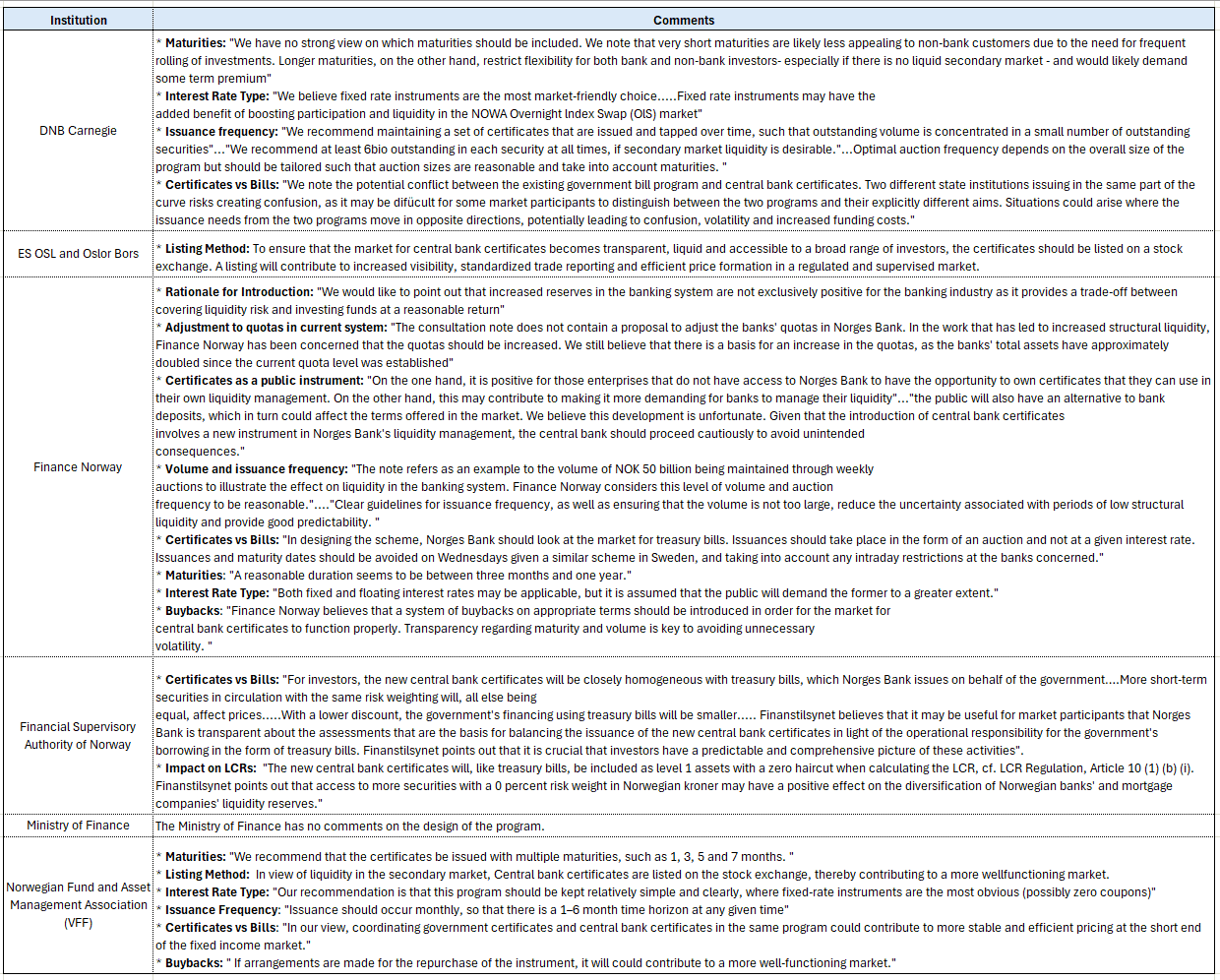

NORGES BANK: All Certificate Responses Published: Trade-off vs Bills A Concern

Yesterday, Norges Bank published all responses to its consultation on central bank certificates. See here

Of the six responses submitted, a two consistent themes were:

- That certificates will be very similar securities to Treasury Bills. Norges Bank will need to keep this in mind when designing the system, to avoid conflict/confusion amongst participants.

- Fixed rate certificates are likely to be more desirably than floating rate.

Full summary of comments in the image below. There are not yet any details around when Norges Bank will provide more information on the introduction of certificates.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: USDCAD Consolidating Tuesday Break Lower, 50-Day EMA Up Next

- The Canadian dollar notably outperformed yesterday, prompting USDCAD to break a cluster of recent lows and close below the 20-day EMA for the first time since mid-September. Continued weakness this morning prompted fresh 4-week lows for the pair, with session lows coming within 9 pips of the important 50-day EMA, which intersects at 1.3915.

- A clear break of this level would signal scope for a deeper retracement and potentially expose a channel support at 1.3840. The bull channel is drawn from the Jul 23 low, and weakness below this point would alter the medium-term bullish theme. Key resistance is at 1.4080, the Oct 16 high.

- Scotiabank have noted that the USD’s daily close below the 200-day MA yesterday should tilt risks towards a little more softness developing towards 1.3850/00 if the break lower is sustained. Separately, SocGen said the BOC may need to disappoint the consensus call for lower rates if fresh CAD sogginess is to be avoided.

- The Bank of Canada is set to cut its policy rate by 25bp for a second consecutive meeting today. The new 2.25% overnight rate would represent the bottom of the BOC's "neutral" estimate range (2.25%-3.25%).

UK FISCAL: Starmer Refuses To Rule Out Inc. Tax, NI Or VAT Hikes

PM Sir Keir Starmer has refused to rule out increases in income tax, National Insurance contributions, or VAT. In PMQs, the leader of the main opposition centre-right Conservatives, Kemi Badenoch, asks Prime Minister Sir Keir Starmer if he still stands by the commitment to the tax promises made in the 2024 Labour election manifesto.

- Starmer deflects, claiming that under Labour, retail sales are higher, inflation is lower, growth has been upgraded, and the UK stock market is at an all-time high. Badenoch notes that when she asked the same question of Starmer in July, his answer was a simple "yes".

- Later in PMQs, asked by a Conservative MP to rule out an extension of the freeze on income tax thresholds, Starmer answered only "the freeze was introduced by them". While it is not unusual for a PM to refuse to talk on specific policies ahead of a budget, given the media narrative surrounding the budget (that the gov't is preparing the ground for sizeable tax increases), these comments will do little to dispel that speculation.

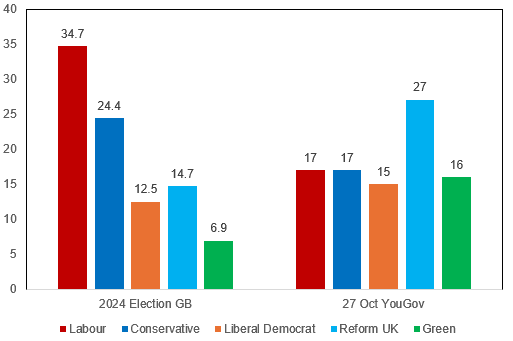

- Politically, the Labour gov't finds itself in a difficult position with record-low approval ratings and opinion polling support draining away to Reform UK on the right and the Greens on the left.

- The latest YouGov poll from 27 Oct shows Labour at a record low with the pollster, at just 17% support. This puts them level with the Conservatives and just one per cent ahead of the Greens, which have seen a notable boost following the election of left-wing populist Zack Polanski as leader.

Chart 1. 2024 General Election Results (GB Only) & 27 October YouGov Opinion Poll, %

Source: House of Commons, YouGov, MNI

STIR: Some Analysts See Incoming Data Supporting Dovish Recommendations

Summarising a few analysts views on front-end EUR rates ahead of tomorrow’s decision:

- Goldman Sachs: “With recent data and communication skewing slightly dovishly, we view risks to market pricing for 25Q4-26Q2 as tilted to the dovish side.”….“We expect the front-end to re-steepen as near-term risks around the ECB policy path combine with improving forward expectations for growth. We continue to recommend front-end steepeners, such as ERH6/ERH7”.

- Morgan Stanley: “We see limited potential for next week’s ECB meeting to trigger a meaningful market reaction and we keep our set of recommended trades: Feb-Mar ECB flattener, ERH6 call spread, and received 1y1y”….“However, with the ECB set to reassess its economic outlook again in December and our economists anticipating downside risks starting to materialize in the next round of data releases, we think data could start playing a more significant role for the market, supporting our long positioning.”

- Danske Bank: “While we see upside risks to current market pricing as we expect the ECB to remain on hold throughout 2026, we have recently taken profit on our payer positions in the short end of the EUR-swap curve as we see the risks as more balanced”.