EU TRANSPORTATION: Air Baltic: Turns to Sale (bbg)

Jan-28 13:02

(AIRBAL Sec; NR/B Neg/B-) Lufthansa holds 10%, full article here : https://blinks.bloomberg.com/new...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Early SOFR/Treasury Option Roundup

Dec-29 12:56

Limited Treasury option volumes overnight, scant SOFR options so far. Underlying Tsy futures modestly higher, SOFR futures running steady to mildly higher in Reds-Greens. Projected rate cut pricing retreats slightly vs. late Friday levels (*): Jan'26 at -4.8bp, Mar'26 at -13.9bp (-14.5bp), Apr'26 at -20.3bp (-20.9bp), Jun'26 at -34.3bp (-35bp).

- SOFR Options:

- 1,000 0QH6 96.93/97.18 call spds vs. 96.75 puts

- -1,000 0QH6 96.68 puts, 6

- Treasury Options:

- -3,000 TYG6 112.75 calls, 32 vs. 112-26/0.45%

- +2,000 Wed wk5 TY 112.25/112.5 2x1 put spds, 2 vs. 112-19/0.04%

- +2,000 TYG6 113/114.5 call spds, 19 vs. 112-23.5/0.31%

- -1,000 FVG6 109.5 calls, 17.5

- -2,000 FVG6 108.5/109 put spds, 6.5-7

- -3,200 TUG6 104.12 puts, 2

FOREX: USD Buying Accompanies Stalling Treasury Rally

Dec-29 12:37

The phase of USD buying at the NY crossover appears to coincide with the stabilisation of the belly of the US curve, with activity picking up headed through to US hours.

- The resultant pressure on GBPUSD as the pair at new pullback lows, making 1.3456-61 the interim support (Dec 16 high / Dec23 low), but more material into 1.3413.

- AUDUSD is comfortably clear of 0.6700, meaning spot has faded fast off the new cycle high printed overnight of 0.6728.

- Fragility of market sentiment is a clear driver of prices between now and when markets resume in earnest in the new year, as the Sunday Trump - Zelensky meeting appears positive, but leaves little room for material progress toward a ceasefire.

- Similarly, commodity-tied currencies in G10 are trading poorly given the slippage in metals prices, but it's not uniform globally: in fact ZAR is outperforming, keeping USDZAR pinned toward the cycle lows printed on Christmas Eve at 16.6140.

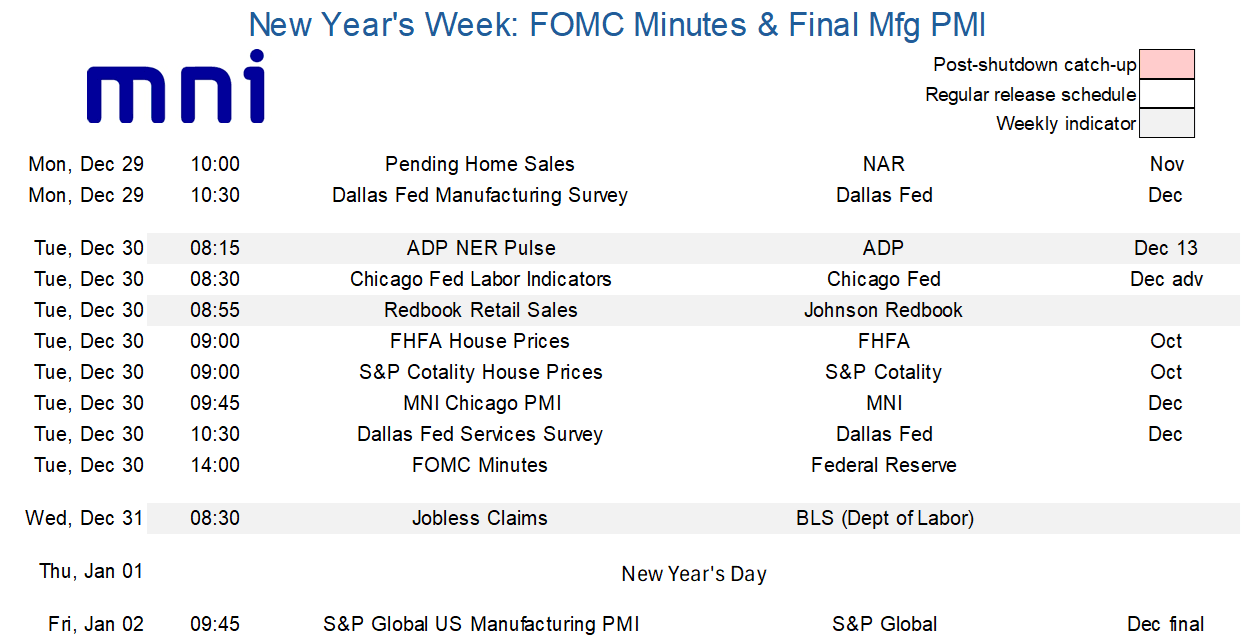

LOOK AHEAD: Highlights of This Week’s US Data Schedule

Dec-29 12:08

- The MNI Chicago PMI (Tuesday) offers an alternative look at manufacturing activity ahead of the ISM manufacturing survey the following week and should be watched after sliding 7.5 points to 36.3 in November with a particularly large drop in new orders.

- Weekly labor: ADP announced the "NER Pulse won’t publish Dec. 30 because the week ending Dec. 13 corresponds to the reference week of the monthly National Employment Report. Main Street Macro and the NER Pulse will resume publication Jan. 13, 2026."

- Jobless claims (Wednesday) meanwhile are a day early again and aside from offering a latest look at the health of the labor market will also give a better indication of continuing claims in the payrolls reference period.

- The final manufacturing PMI (Friday) rounds the week off after the flash release saw it at 51.8 after 52.2 for a five-month low. From the press release: “Production growth dipped to a three-month low as new orders fell for the first time since December 2024.”

- Away from data, the FOMC minutes from the Dec 9-10 meeting will be interesting (Tuesday). Powell delivered a not-so-hawkish 25bp cut but with signs of a still clearly divided committee whilst we watch for discussions around changes in administered rates.

- Powell on the perceived differences in the risks to the outlook on the FOMC: “"The risk is that tariff inflation just turns out to be more and more persistent... I think the other possibility is, less likely, and that is just that the labor market gets tight, or the economy gets tight. And you see, just traditional inflation. I don't see that as particularly likely, but ... again, all across the Committee, people see the picture pretty similarly, but see the risks quite differently. And some people do see the inflation risk. And I wouldn't dismiss that case. But you've got to make an assessment, and this is the assessment."