EM LATAM CREDIT: Adecoagro: USD300mn Common Share Registration – Positive

(AGRO; Ba2*-/BB*-/NR)

• The Brazil industrial agriculture producer Adecoagro registered to sell USD300mn of equity to finance their acquisition of Profertil, an Argentina fertilizer company. We view the issuance of equity to fund their acquisition as positive as well as the diversification benefits of acquiring a profitable business that fits well into their existing agriculture business. We also note that Q3 EBITDA from their sugarcane ethanol processing business was up 20% YoY and up 2x sequentially which was far better than one of their main competitors Raizen.

• AGRO 32s were last quoted T+ 471bp, or 8.68% yield,135bp wider than new issue July 2025. The company’s surprise Argentina acquisition at a time when conditions in its primary sugarcane ethanol processing business were challenging caused a lot of the widening, but the effect was exacerbated by the fallout from Brazil’s Braskem and Ambipar bond debacles.

• The concern expressed by the rating agencies was for a 100% leveraged transaction, so we saw the equity shelf filing as positive as well as today’s registration. Ratings are still likely to get downgraded because the company is increasing its exposure to ’CCC’ rated Argentina so bond ratings will likely move closer to the ‘B’ category from at least one of the agencies due to sovereign ceiling limitations.

• The company intends to offer in the next two days USD300mn common shares of which controlling 75% private equity shareholder Tether plans to buy USD200mn. The balance of the USD480mn acquisition cost will be financed with an already arranged term loan and cash on hand.

• We commented on the USD500mn shelf filing December 1st and the positive effect of issuing equity to finance the acquisition: https://mni.marketnews.com/3MwRFos

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

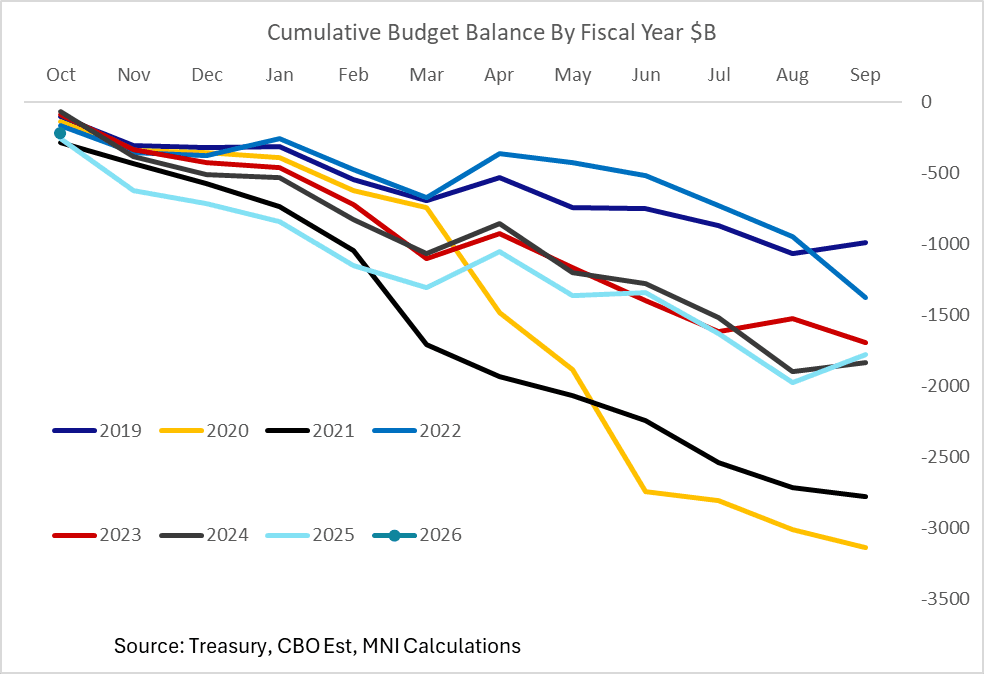

US FISCAL: CBO: October Deficit Shrinks, Shutdown/Timing Issues Muddy Comparison

The Congressional Budget Office estimates that the federal government posted a $219B deficit in October, vs just over $258B a year earlier. This would still be one of the bigger October deficit in recent years but regarding that $39B Y/Y decrease: revenues were up $75B vs a year earlier, "driven by larger collections of individual income and payroll taxes and by increased customs duties", and while outlays were up $37B that was due to a timing shift without which outlays would have decreased (not increased) by $70B vs Oct 2024.

- Overall accounting for timing changes in this first month of the fiscal year, "the decrease in the deficit for October also would have been larger— $145 billion rather than $39 billion. CBO estimates that outlays were smaller than a year ago in part because of the lapse in discretionary appropriations that began on October 1, 2025."

- As such the imminent reopening of the government will probably mean that outlays ramp up shortly to make up for lost ground.

- We should also note that CBO - whose estimates are usually quite accurate - undershot the actual September surplus by $34B, which it attributes to the lack of full data in shutdown: "Because data were not available from many agencies during the lapse in funding, CBO’s estimate of September spending did not account for certain transactions with the Treasury, a number of which were recorded as offsetting receipts."

- Treasury is due to publish its October estimates on Thursday but it's unclear whether it will produce a report even if the shutdown is resolved by then.

EURJPY TECHS: Bullish Trend Sequence

- RES 4: 180.37 1.500 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 3: 180.00 Psychological round number

- RES 2: 178.94 1.236 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 1: 178.82 High Oct 30 and the bull trigger

- PRICE: 177.84 @ 16:23 GMT Nov 10

- SUP 1: 175.29 50-day EMA

- SUP 2: 174.82 Low Oct 17

- SUP 3: 173.92 Low Oct 6 and a gap high on the daily chart

- SUP 4: 173.77 Bull channel support drawn from the Feb 28 low

The trend in EURJPY remains bullish and a price sequence of higher highs and higher lows is intact. Moving average studies are in a bull-mode position too, highlighting a dominant uptrend. Recent gains signal scope for an extension towards 178.94 next, a 1.236 projection of the Jul 31 - Sep 29 - Oct 2 price swing. Support to watch lies at the 50-day EMA, at 175.29. A clear break of this EMA would signal scope for a deeper retracement.

US TSYS: Late SOFR/Treasury Option Roundup: Jan'26 10Y Call Buying Still Strong

Treasury options leaning toward low delta calls - large Jan'26 buyer resumes, SOFR option volumes remained rather modest. Underlying futures weaker, near middle session range - bit of risk as hopes of ending US Gov shutdown rise after eight Democrats voted with Rep's on CR to fund gov through end of January. Projected rate cut pricing retreats vs morning levels (*): Dec'25 at -15.5bp (-16.3bp), Jan'26 at -25.1bp (-26.1bp), Mar'26 at -35.2bp (-35.8bp), Apr'26 at -41.3bp (-41.6bp).

- Treasury Options:

- 2,200 USZ5 115/119 strangles, 18 ref 116-31

- 1,500 USF6 115/116/117 put flys

- +25,000 TYF6 111.5 puts, 22

- over 52,000 TYF6 113 calls, 42-45, ref 112-23 to -22.5

- 1,300 TUZ5 104.5/104.87 put spds ref 104-05.38

- 1,100 FVZ5 110.75/FVF6 110.5 call spds

- +10,000 TYF5 113.5 calls, 31 (adds to +50k at 27 earlier)

- over 25,500 TY/wk2 TY 112.5 put spds, 11 (TYZ over)

- 5,000 TYZ5 111/111.5/112.5 2x3x1 broken call flys ref 112-21

- +50,000 TYF6 113.5 calls, 27 (last Thursday: +100,000 TYF6 113.5 calls, 30-32 vs. 112-18/0.32%)

- over +/-15,400 TYZ5 113 calls, 16-17 ref 112-19

- over 10,400 TYZ5 112.25 puts

- 3,000 TYZ5 113.5/114 call spds ref 112-19 to -18

- 1,200 TYZ5 110.75/111.75 put spds ref 112-18.5

- 2,300 TYF6 111/112 put spds ref 112-15.5

- -1,500 TYG6 113.5 calls, 39 vs. 112-15/0.35%

- +3,000 wk4 TY 113.5 calls, 11

- +1,000 TYH6 112.5 straddles, 226

- -4,000 wk2 TY 113.25 calls, 3

- +2,000 USF6 130 calls, 1

- 1,000 FVZ5 108.25/108.5/108.75 put flys ref 109-07

- +1,000 FVZ5 109.25 straddles, 34.5

- +3,000 Thu wkly FV 109 puts, 1.5

- 3,400 TYZ5 114.5 calls, 3 ref 112-19.5

- SOFR Options:

- +10,000 0QZ5 96.50/96.62 put spds, 1.5 vs. 96.865 to -.87/0.10%

- 3,000 0QX5 96.87 puts, 4.5 vs. 96.87/0.52%

- 4,000 SFRZ5 96.37 calls, cab

- over 4,000 SFRZ5 96.18 puts, 0.5 last

- 1,000 SFRZ5 96.06/96.12/96.18 put flys ref 96.24