EM ASIA CREDIT: Adani Ports: Q1 results

(ADSEZ, Baa3neg/BBB-pos/BBB-neg)

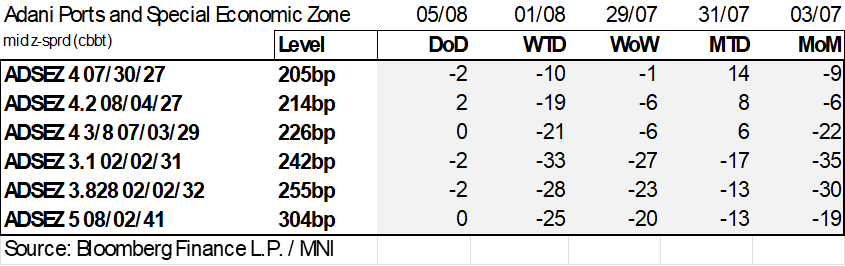

Q1 results solid beat, positive for spreads

Adani Ports, India’s largest commercial port operator with 15 ports and a total capacity of 633 million metric tonnes (mmt), reported strong 1Q26 earnings after market close yesterday. EBITDA rose 13% YoY to INR55bn, beating consensus estimates of INR50bn — positive for spreads.

Operationally, cargo volumes increased 11% YoY to 121 mmt, driven mainly by a 2.4x surge in international volumes. Growth was broad-based across cargo segments, led by containers and coking coal.

On credit metrics, reported leverage improved slightly, decreasing from 1.9x in FY25 to 1.8x LTM 1Q26. The company’s FY26 guidance continues to include leverage as high as 2.5x. FFO interest coverage remained stable at 7.0x for the quarter, compared with 7.1x in FY25.

For FY26, the company estimates EBITDA in the range of INR210–220bn, with cargo volumes expected between 505-515mmt.

Overall, strong operational performance and stable credit metrics support a constructive outlook on Adani Ports’ credit spreads.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Bear-Steeper Holds At Lunch, US Tariff Letters To Go Out Today

At the Tokyo lunch break, JGB futures are slightly weaker, -6 compared to the settlement levels.

- Japan's weak wage data released Monday shows that it is becoming more difficult for the Bank of Japan to pursue interest-rate increases. Inflation-adjusted wages fell 2.9% on the year in May, compared with a 2.0% drop in April. With trade negotiations between the U.S. and Japan seemingly stuck and Washington threatening to impose even higher tariffs on Japanese goods, the economic outlook is "incredibly challenging," says Moody's Analytics economist Stefan Angrick. (DJ via BBG)

- Cash US tsys are flat to 3bps richer in today's Asia-Pac session after resuming trading following the long weekend.

- US President Trump has posted via Truth Social that the US will start delivering letters outlining tariff levels to various countries starting 12pm Monday, US eastern time. Trade deals will also be announced at the same time. Focus will be on tariff levels, particularly after Trump remarks late last week, where he stated tariff levels could be as high as 60-70% (although further details weren't provided).

- Cash JGBs are flat to 6bps cheaper across benchmarks, with a steeper curve. The benchmark 5-year yield is 0.7bp higher at 0.978% ahead of tomorrow’s supply.

- The swaps curve has bear-steepened, with rates 1-3bps higher. Swap spreads are generally tighter.

AUSSIE BONDS: Slightly Stronger, Job Ads Point To Resilient LM Conditions

ACGBs (YM +1.0 & XM +0.5) are slightly stronger, but the ranges have been narrow.

- The ANZ June job ads print was +1.8%m/m, after a revised fall of 0.6% in May (originally reported as a -1.2% decline). In y/y terms, jobs ads are -0.4%. At the start of the year, we were at -13.7%. This was the best m/m increase for the index since Sep last year. It points to continued resilience in terms of labor market conditions.

- Cash US tsys are flat to 3bps richer in today's Asia-Pac session after resuming trading following the long weekend.

- US President Trump has posted via Truth Social that the US will start delivering letters outlining tariff levels to various countries starting 12pm Monday, US eastern time. Trade deals will also be announced at the same time.

- Cash ACGBs are 1bp richer with the AU-US 10-year yield differential at -15bps.

- The bills strip is little changed.

- RBA-dated OIS pricing is slightly softer on the day across meetings ahead of tomorrow’s RBA Policy Decision. A 25bp rate cut this week is given a 93% probability, with a cumulative 78bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Notably, today’s moves leave meetings pricing 15-32bps softer than levels before the May 20 RBA Meeting.

FOREX: Trump BRICS Tariff Threat Weighs On Risk Sentiment

The USD is supported post Trump headlines which threaten to impose an additional 10% tariffs on counties that align themselves with anti-American policies of the BRICS group. The Truth Social Post was: ""Any Country aligning themselves with the Anti-American policies of BRICS, will be charged an ADDITIONAL 10% Tariff. There will be no exceptions to this policy."

- USD/CNH has risen back above 7.1700, but is only 0.15% weaker in CNH terms versus end Friday levels. We are also still sub the 20-day EMA resistance point at this stage.

- USD/ZAR is up close to 0.50%, last near 17.67. This is only marginally above recent lows in the pair close to 17.50.

- AUD and NZD are off around 0.50% in the G10 space, with the latest Trump comments adding to the risk off mood and uncertainty around trade/tariff outcomes. AUD/USD was last near 0.6525, NZD/USD is back to 0.6025/30.

- US equity futures are holding weaker, down 0.40% for Eminis. Yen is also sifter, giving up earlier gains, last back to 144.75/80.