EU UTILITIES: Acciona Energias(ANESM): Fitch Outlook Negative

We see this pressuring spreads, with risk heightened as a sole rated issuer. The move largely reflects increasing risk on asset sales, with base case that it should remain IG.

- Following a slow pace of asset sales and lower power prices Fitch now expects leverage to fall below threshold by FY26, a year later than previously.

- It sees FFO/ND at 6.6x for FY25, with a 4.5x rating sensitivity. That drops to 5.1x proforma for agreed asset sales.

- ~€2.3bn of new divestments are expected in 2026-28. Execution risk has increased, reflected in the slower than expected pace of sales this year.

- Capex is set to fall to €1bn p.a. from €1.7bn.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Friday's High In Futures Holds On First Test As Budget Week Gets Underway

Gilts firm at the open, mimicking moves in core global FI peers.

- Friday’s high in futures (92.43) holds on the first test before a fade back to 92.35.

- A break higher would expose the November 18 high (92.60), which protects the 20-day EMA (92.70).

- Meanwhile, support comes in at 91.51.

- Bears remain in technical control at this stage

- Yields ~1.5bp lower across the curve.

- Recent headlines reaffirm the idea that the OBR is set to downgrade growth across its forecast horizon.

- Elsewhere, we have highlighted the likely reduction in headline and services CPI surrounding the reported freeze of rail fares (-0.02ppt & 0.04-0.05ppt respectively in March ’26).

- Wider weekend reporting generally reaffirmed known focal areas and ideas as we move towards Wednesday’s Budget.

- Some buy-side names have outlined what they want to see in the Budget via the FT: https://www.ft.com/content/e01f51d9-11d5-45d8-a865-62446eeda545

- Note that the BoE will come to market with GBP750mln of medium-term paper from its APF this afternoon.

MONTH-END EXTENSIONS: Bond Extensions

Given the shorter Week can't rule out some small front running. Overall though, Extensions are below average and the impact should be limited.

Bloomberg Bonds:

- US Tsys: +0.11yr (average).

- EU Govies: +0.05yr (small).

- UK Govies: -0.03yr (non event).

MS Bonds:

- US Tsys: +0.08yr (average).

- EU Govies: +0.05yr (small).

- UK Govies: -0.03yr (non event).

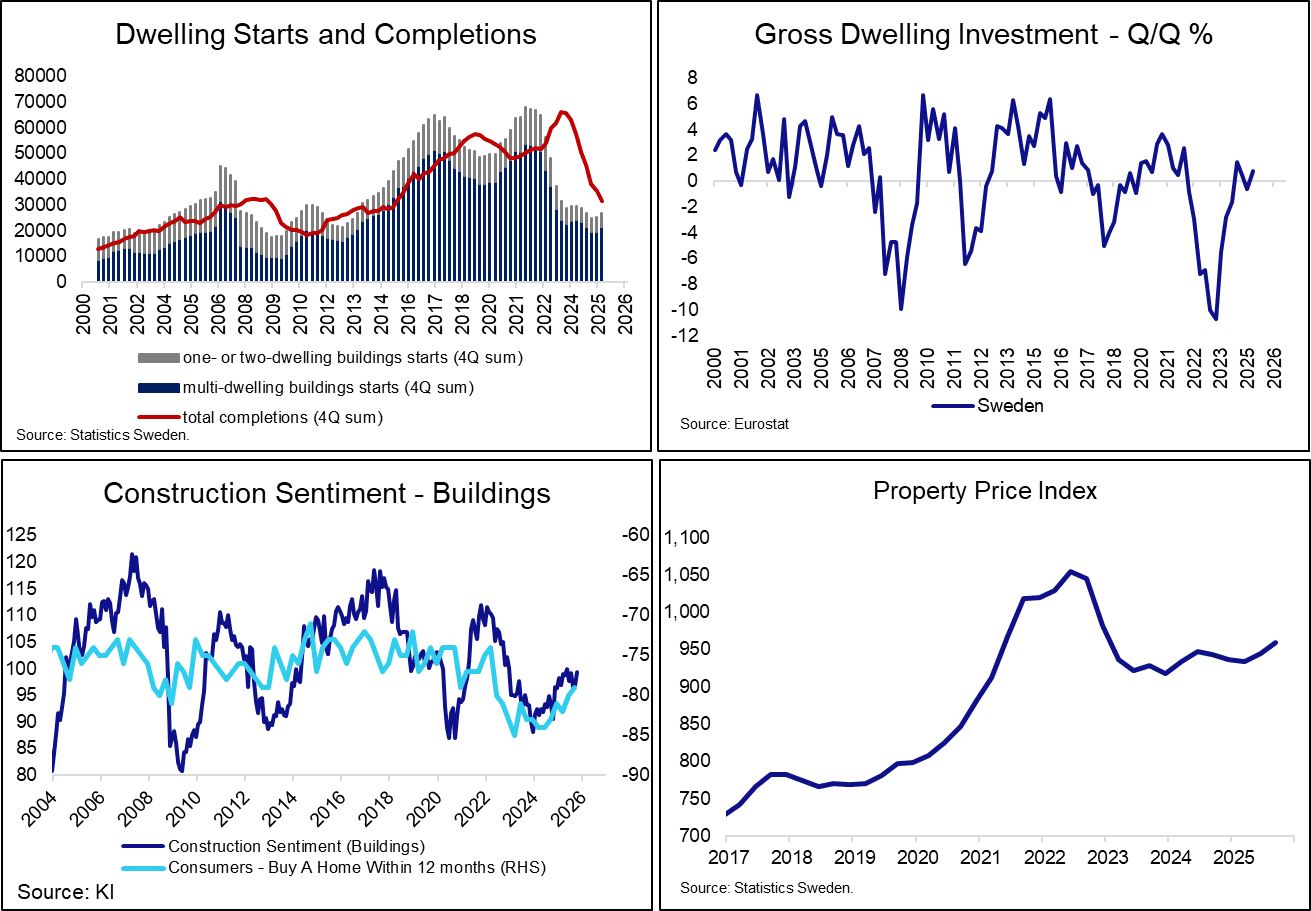

SWEDEN: Recovery in Residential Construction Sector Remains Sluggish

The recovery in the Swedish residential construction sector remains sluggish. Although this year’s rate cuts have provided financial relief, concerns around short- and long-term demand have constrained starts, and prevented completions from bottoming out. Property prices have started trending higher from 2023 lows, but remain well below 2021/2022 levels.

- Total housing starts increased by 6.5k in Q3, down from 7.5k in Q2. Measured as a 4Q rolling sum, total housing starts rose 26.9k in Q3, up from 25.4k in Q2 for the highest in a year.

- The number of completions remains firmly on a downward trend though, increasing 31.5k in Q3 after 35.3k in Q2 and 50.6k a year ago.

- While dwelling investment in the national accounts has rebounded from the Covid-induced slump, recent quarters have seen more stable (but no longer increasing) readings. Q3 GDP is due on Thursday.

- Although sentiment indicators in the Economic Tendency Indicator have stabilised in recent months (see charts), they remain below pre-covid averages.

- Furthermore, the Riksbank’s latest Business Survey noted that:

- “In residential and commercial construction, projects are sometimes being postponed because of uncertainty about how demand will develop. The weak demand for new housing means that construction companies can basically only sell projects that have largely been completed”

- ”Construction companies hope that the lower level of interest rates and the upcoming fiscal policy stimulation measures will kick-start the wider economy. At the same time, they see households as “so hesitant” and are unsure whether the measures will be enough to boost demand for new homes”.

- “In a longer perspective, the major construction companies emphasise that there is already a high supply of housing in the major cities, while population projections do not indicate that demand for new housing will increase in the years ahead.”