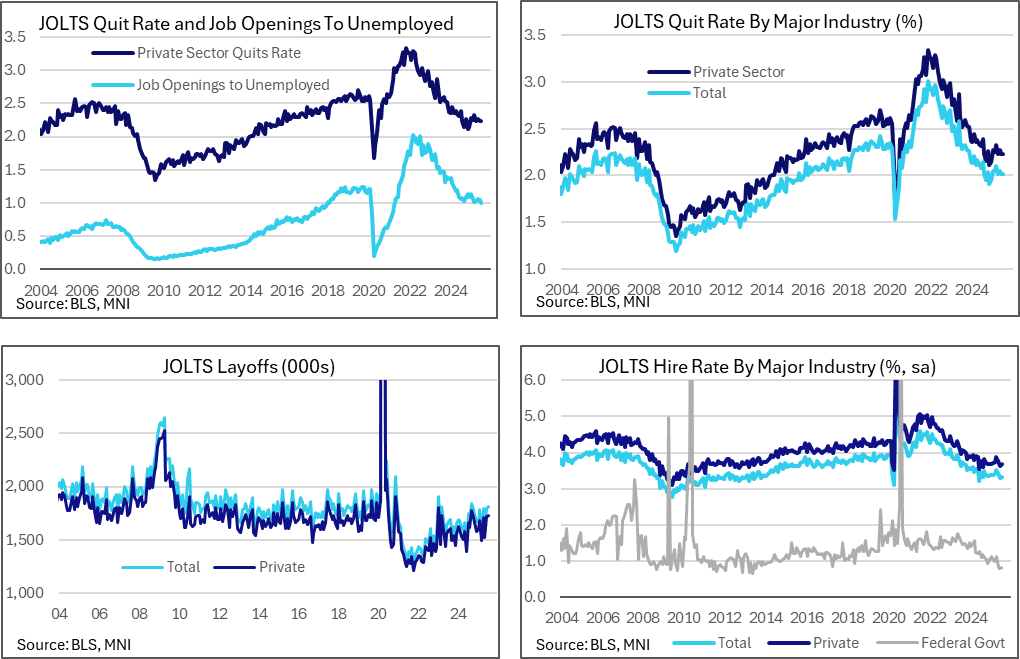

US DATA: A Soft JOLTS Report As Vacancy To Unemployed Tilts Lower

Sep-03 14:18

The JOLTS report for July was softer than expected, primarily on the openings front as the ratio of vacancies to unemployed fell to a new recent low. Powell at Jackson Hole had pointed to this metric in the category of little changed to only modestly softer over the past year, leaving sensitivity to any subsequent declines here.

- Job openings were lower than expected at 7181k (sa, cons 7380k) in July after downward revised 7357k (initial 7437k) in June.

- Combined with the already known sizeable rise in unemployment from last month’s payrolls report and the ratio of openings to unemployed fell to 0.99 from 1.05 (initial 1.06).

- That’s the lowest ratio since Apr 2021 having kept to a fairly tight range around an average 1.07 since mid-2024. That said it’s still not wildly different to the 1.02 and 1.03 seen in Mar-April.

- The quit rate was little changed at 2.01% after an upward revised 2.01 (initial 1.97) in June, having averaged 2.0% since Aug 2024.

- These quit rates remain low historically compared to pre-pandemic figures of 2.3% through 2019 and 2.2% through 2017-18, but see a steady trend rather than a further softening. Indeed, they remain above late last year’s recent lows of 1.9%.

- Hire rates meanwhile ticked up marginally to 3.33% from an upward revised 3.30% (initial 3.26), although that does little to reverse a pullback from a recent high of 3.52% in April.

- Layoffs were higher than expected as they increased to 1808k (cons 1675k) from an upward revised 1796k (initial 1604k) although we caution that the consensus comes from only three responses. Nevertheless, that’s still the highest since Sep 2024 and continues a broad uptrend back more clearly to pre-pandemic levels.

- Recall Powell from Jackson Hole (Aug 22): “The unemployment rate, while edging up in July, stands at a historically low level of 4.2 percent and has been broadly stable over the past year. Other indicators of labor market conditions are also little changed or have softened only modestly, including quits, layoffs, the ratio of vacancies to unemployment, and nominal wage growth.”

- Today’s report for July marks a further modest softening in the ratio of vacancies to unemployment although the quits rate has continued to stabilize.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: SONIA/Euribor Dec '26 Spread Forms Double Bottom Support

Aug-04 14:12

The SONIA/Euribor Dec ’26 Spread has formed double bottom support in the 145.5/146bp area, with focus on this week’s BoE vote split key given almost full discounting of and unanimous expectations for a 25bp cut on Thursday.

- With the market now more assured when it comes to pricing the ECB terminal rate (leaning towards one further 25bp cut in this cycle) any meaningful repricing is likely to come from the SONIA leg of the spread.

- Goldman Sachs remain long SFIZ6 vs. ERZ6.

- Signs of a slowing UK labour market have not been enough to promote a meaningful dovish repricing across ’26 SONIA spreads as of yet, with the SFIZ5/Z6 spread discounting just over 25bp of easing.

- With sticky inflation worries no doubt present, BoE cues may be required for a fresh extension lower, if such a move is to be forthcoming.

- We will provide deeper insight in our BoE preview but remind that the accompanying guidance at this week’s BoE decision is widely expected to be left unchanged with the "gradual", "restrictive" and "careful" buzzwords all likely to remain.

- Based on the 17 previews that we had read as of Friday providing vote split expectations:

- The modal expectation is a 2-5-2 vote split (7/17).

- 11 expect two votes for 50bp cut, 3 expect one vote, 3 expect no votes for 50bp cut

- 2 expect three votes for on hold, 9 expect two votes on hold, 4 expect 1 vote on hold, 2 expect no votes for on hold.

- 2-4-3 (50-25-0) is the most split committee within an analyst's base case, 0-9-0 is also an analyst's base case.

Fig. 1: SONIA/Euribor December ’26 Spread

Source: MNI - Market News/Bloomberg Finance L.P.

MNI: US JUN FACTORY ORDERS -4.8%; EX-TRANSPORT NEW ORDERS +0.4%

Aug-04 14:00

- MNI: US JUN FACTORY ORDERS -4.8%; EX-TRANSPORT NEW ORDERS +0.4%

- US JUN DURABLE ORDERS -9.4%

- US JUN NONDEFENSE CAP GOODS ORDERS EX AIRCRAFT -0.8%

MNI: US JUN FACTORY ORDERS -4.8%

Aug-04 14:00

- MNI: US JUN FACTORY ORDERS -4.8%

Trending Top

Jan-30 21:43

Jan-30 21:11