US DATA: A Small Uplift In Mortgage Activity As Rates Ease

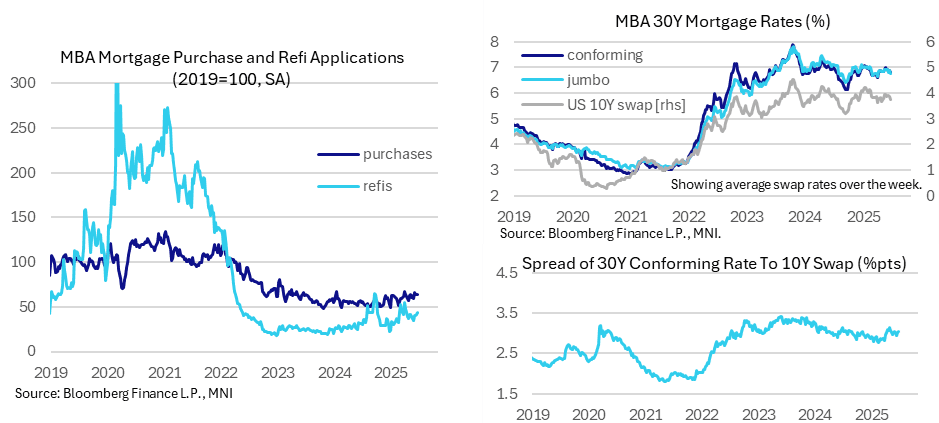

- MBA composite mortgage applications increased 2.7% (sa) last week after 1.1%, -2.6% and a strong 12.5% in the previous three weeks.

- Refis led the latest increase, rising 6.5% after 3.0%, as new purchase applications underperformed for a fifth consecutive week with 0.1% after -0.4%.

- The usual reminder of relative levels, however: composite applications stand at 55% of 2019 averages, consisting of 64% for new purchases and 44% for refis.

- The latest increase was helped by a 9bp decline in the 30Y conforming rate to 6.79% for its lowest since the week to Apr 4, marking a 13bp decline over the past month.

- With the average 10Y swap rate over the week dropping 12bp, the 30Y mortgage rate to 10Y spread widened further to 305bps (+3bp) for its highest since the week to May 9. That’s still below the 315bp in late April/early May but above the 285bp averaged in Q1 in a net tightening in conditions, potentially reflecting some more pessimistic looking housing data more broadly.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ECB: ECB Speak Wrap (May 27 – June 2)

See here for the full publication: 250602 - Weekly ECB Speak Wrap.pdf

The ECB has entered its pre-meeting quiet period ahead of Thursday’s decision, where a 25bp cut remains unanimously expected a fully priced by markets. MNI’s preview will be out later this week.

The MNI Policy Team’s latest sources piece headlines the past week’s ECBspeak. The ECB is likely to lower its inflation projection for 2026 to 1.7% or 1.8% in its June exercise, one or two tenths below the 1.9% seen in March, Eurosystem sources told MNI, adding that there could be a pause in rate cuts after a further 25-basis-point reduction next week. Despite this downward revision, this deviation below 2% will not be considered strong enough to automatically trigger an additional rate cut beyond the June meeting, as some of the drivers of this inflation revision could reverse course given uncertainty over international trade, sources said.

- This somewhat more cautious approach once rates reach 2.00% - the middle of the ECB’s heavily caveated neutral range – will likely be strongly advocated by hawkish leaning Governing Council members. On May 28, Knot said that “a monetary policy stance that is neither accommodative nor restrictive is in my view appropriate”.

- However, there is still scope for more cuts depending on the macroeconomic data and trade outlook. Speaking to the MNI Policy Team, acting Central Bank of Malta Governor Demarco (May 27) said that “if headline inflation in the medium term is expected to remain persistently well below 2% then it is more likely that there is room for interest rates to fall below 2%”.

OUTLOOK: Price Signal Summary -Bull Cycle In Bunds Remains In Play

- In the FI space, a bullish theme in Bund futures remains intact and the contract is holding on to its latest gains. The recent recovery suggests the move down between Apr 22 - May 15, has been a correction. A continuation higher would strengthen the reversal and signal scope for a climb towards 132.03, the Apr 7 high. Key short-term support to watch is 129.13, the May 15 low. First support lies at 130.39, the May 29 low.

- A bear cycle in Gilt futures remains in play. The contract has recovered from its recent lows - gains are considered corrective and this is allowing a short-term oversold condition to unwind. The bear trigger has been defined at 90.11, the May 22 low. Key short-term resistance to watch is 91.87, the May 20 high. It has been pierced, a clear break of this level is required to highlight a stronger reversal.

OPTIONS: Larger FX Option Pipeline

- EUR/USD: Jun03 $1.1348-50(E3.2bln), $1.1350-55(E1.2bln); Jun05 $1.1050(E5.9bln), $1.1300(E2.3bln), $1.1400(E2.2bln)

- USD/CAD: Jun04 C$1.3735-50($1.2bln)