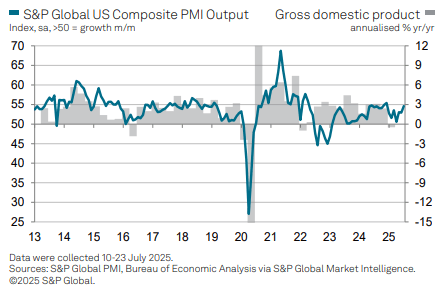

US DATA: A Mixed Bag For July Flash PMIs, Tariffs Increasingly Passed Through

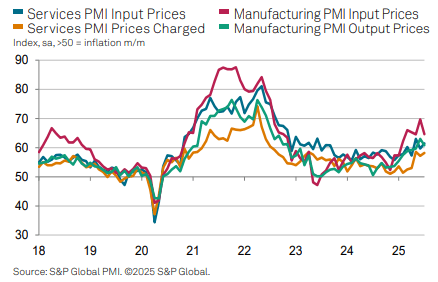

The S&P Global US PMIs were mixed in the flash July release, with manufacturing surprising with its lowest since December and back in contractionary territory whilst services surprisingly increased to the highest since December. Tariffs were reported as being “increasingly passed through to consumers”, with prices charged inflation for goods & services among the highest over the past three years.

- Manufacturing: 49.5 (cons 52.7) in July prelim after 52.9 in June

- Services: 55.2 (cons 53.0) in July prelim after 52.9 in June

- Composite: 54.6 (cons 52.8) in July prelim after 52.9 in June

Highlights (from the full press release here):

- “US business activity grew at a sharply increased rate in July, according to early ‘flash’ PMI® data, marking a strong start to the third quarter. Employment growth was also sustained.

- However, private sector expansion became increasingly unbalanced, as manufacturing business conditions deteriorated in contrast to a strengthening services economy, the latter fueled by rising domestic demand.

- Business confidence in the outlook meanwhile deteriorated in both sectors as companies reported ongoing concerns over the impact of government policies, especially in relation to federal spending cuts and tariffs.

- Alongside upward wage pressures, tariffs were also again widely linked to steeper cost inflation, which was increasingly passed through to customers. The resulting rate of inflation for prices charged for goods and services was among the largest seen over the past three years.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ECB: Context Around Lane's Remakrs On Services Inflation

Some more context on those Lane headlines. He still has confidence in the services outlook despite the headline run above:

- "Headline inflation is currently around a target, but what we always emphasise is that we want it to be around a target on a sustainable basis, not just because there's energy deflation. So we've focused quite a bit on whether services inflation is going to arrive at a level consistent with overall inflation being a 2% and in that case, that's not over".

- "There's still some distance to travel in relation to services inflation, but it's probably fair to say we have enough confidence in what's happened and what we think is ahead of us in terms of services inflation".

- "That backward challenge, bringing inflation down from the peak back to target, I think is largely completed"

EQUITY TECHS: E-MINI S&P: (U5) Uptrend Remains Intact

- RES 4: 6249.00 - High Feb 21

- RES 3: 6200.00 1.50 proj of the Apr 7 - 10 - 21 price swing

- RES 2: 6172.50 High Feb 24

- RES 1: 6143.75 Intraday high

- PRICE: 6125.75 @ 07:24 BST Jun 24

- SUP 1: 5959.00/5913.50 Low Jun 23 / 50-day EMA

- SUP 2: 5811.50 Low May 23

- SUP 3: 5645.75 Low May 7

- SUP 4: 5500.00 Low Apr 30

The trend condition in S&P E-Minis is unchanged, it remains bullish and this week’s strong start reinforces current conditions. Short-term resistance and a bull trigger at 6128.75, the Jun 11 high, has been pierced. A clear break of this level would confirm a resumption of the uptrend that started Apr 7. This would open the 6200.00 handle, a Fibonacci projection. Key support remains at the 50-day EMA - at 5913.50. A clear break of it would signal a reversal.

ECB: Chief Economist Lane Cautious On Services Inflation

"*ECB'S LANE: STILL SOME DISTANCE TO TRAVEL ON SERVICES INFLATION" Bloomberg

"*LANE: PROCESS OF BRINGING INFLATION BACK TO 2% LARGELY COMPLETE"