LOOK AHEAD: A Busy, and Key, First Half Of January For US Data

Dec-24 15:18

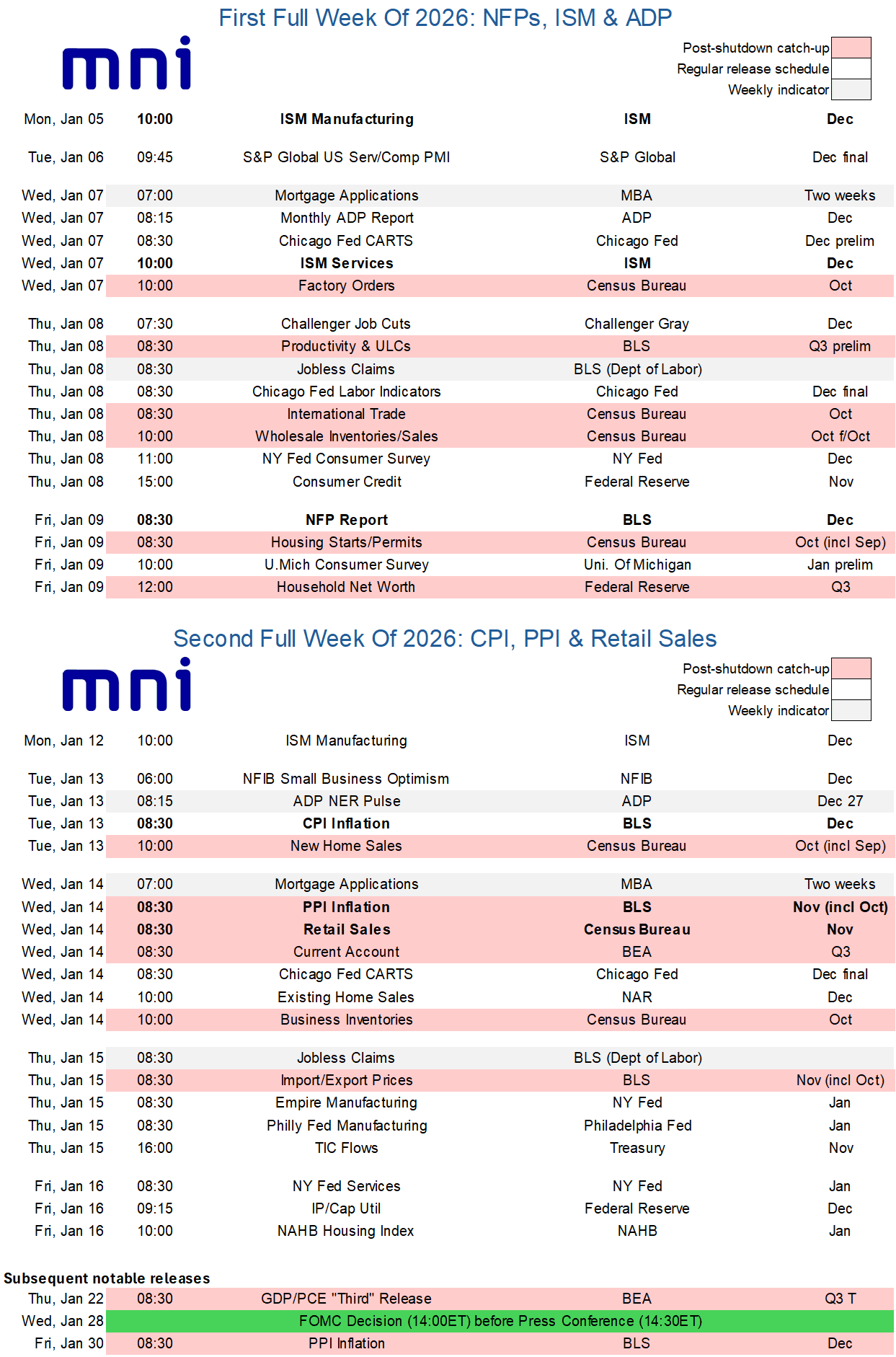

- The first two full weeks of the year see nonfarm payrolls and CPI reports for December with those two key reports back on their original schedules having been prioritized by the BLS.

- PPI and retail sales are also released but they’re still lagging and will only be for November (along with a full set of October details in the case for PPI). Note that PPI for December will then follow at the end of the month as the BLS continues to work on returning that report to its original schedule.

- Private sector reports meanwhile are highlighted by ISM manufacturing and services reports Jan 5 and 7.

- These all build up to the FOMC meeting on Jan 27-28, which is currently seen with low odds of a fourth consecutive 25bp cut with just 3bp of cuts priced. The next cut is fully priced for the June meeting under a new Fed chair.

- Of the other main releases, we’re still waiting for new release dates for monthly PCE (Nov originally scheduled for Dec 19 and Dec for Jan 29), JOLTS (originally set for Jan 7) and the advance release for Q4 GDP (originally Jan 29).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI EXCLUSIVE: Report on EC's Autumn Semester Package

Nov-24 15:17

MNI reports on economic details of the European Commission's draft Autumn Semester Package, to be released tomorrow -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

SOFR OPTIONS: BLOCK: Large Dec'25 SOFR Midcurve Put

Nov-24 15:16

- 35,000 0QZ5 96.50 puts, cab at 1012:07ET

GILTS: Under Slight Pressure As Equities Recover, Equities Eyed

Nov-24 15:12

{GB} GILTS: The uptick in cover at the latest medium-dated bucket sale from the BoE’s APF holdings provides some brief background support for gilts, but the move quickly fades.

- Cross-market moves have dominated for much of the session, with a recent uptick in equities weighing on gilts.

- Futures have filled the opening gap higher after Friday’s high (92.43) helped cap rallies (today’s highs is 92.44).

- Bears remain in technical control at this stage.

- Support comes in at 91.51.

- Conversely, extension higher would target the November 18 high (92.60), which protects the 20-day EMA (92.70).

- Yields little changed to 1bp higher, curve flatter.

- SONIA futures now little changed to -3.0, while BoE-dated OIS still prices over 80% odds of a December cut.

- Our detailed Budget preview is here.

- Meanwhile, our Gilt Week Ahead document details the key areas to watch at the event and updates on weekend press reports re: fiscal matters.