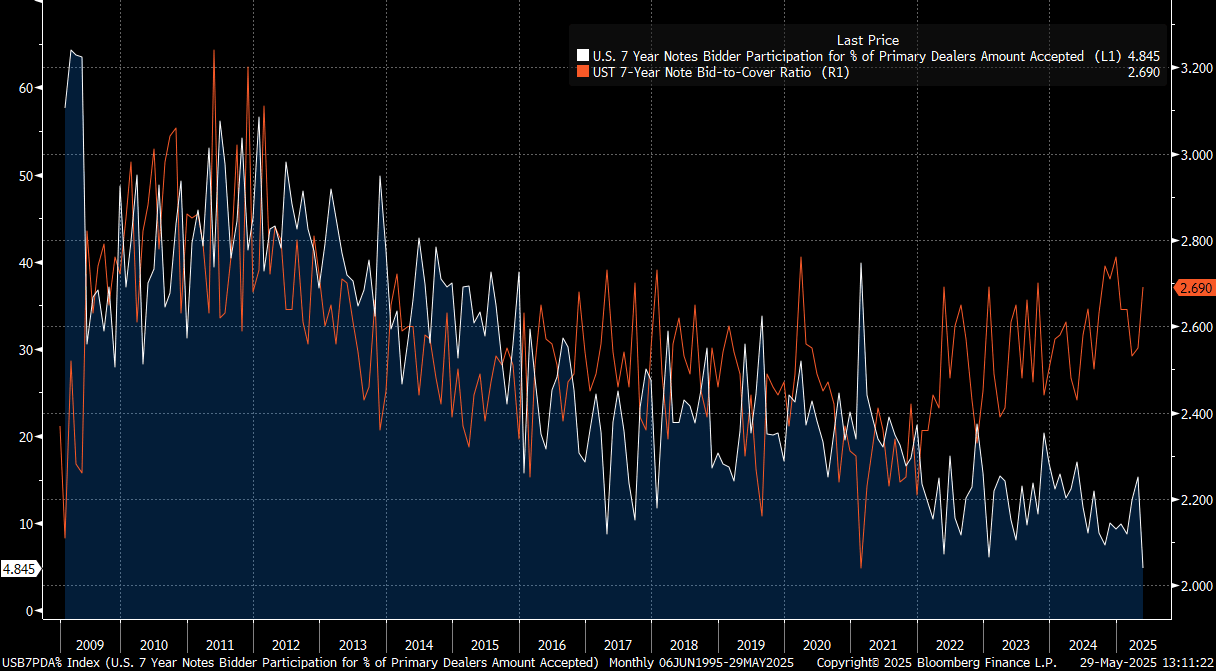

US TSYS/SUPPLY: 7Y Note Auction Trades Through, Record Low Primary Dealer Takeup

May-29 17:11

The 7Y auction saw a very strong result, trading-through the 4.216% when-issued yield by 2.2bp (4.194% high yield). This is the joint-highest trade-through (December 2024 also 2.2bp) since August 2022 (2.9bp).

- Even outside of the trade-through, this was a very strong auction to close out a strong set of sales this week (2s, 5s both traded through too), particularly noteworthy given the lack of intraday concession (high of the day was 4.32%).

- Primary dealer takeup was a record-low 4.85% of competitives, with indirects taking a solid 71.5% nad bid-cover of 2.69x - both within recent ranges.

- Treasury markets reacted positively, extending the intraday rally to session highs (10Y yield dropped to 4.4121%, lowest since May 16).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: EGBs-GILTS CASH CLOSE: Edges Higher On Soft Data

Apr-29 17:08

European FI gained slightly on Tuesday, retracing some of the previous session's weakness.

- Gains were fairly steady through the session, with few major headline/macro catalysts, amid a backdrop of data that was largely on the weaker side of expectations.

- Spanish April preliminary HICP came in firmer than expected, though Spanish GDP came in soft.

- ECB consumer inflation expectations rose for both 1Y and 3Y, though the EC Economic Sentiment survey was weaker than expected.

- Below-consensus US job openings and consumer confidence readings added to the theme.

- ECB's Stournaras sounded cautious on moving rates below 2% (from 2.25% at present); an MNI sources piece debate within the Governing Council ahead of the June rate decision.

- Both the German and UK curves bull flattened, with 10Y Gilts touching 3-week lows. Periphery/semi-core EGB spreads widened modestly, with Portugal underperforming.

- Wednesday's calendar includes French GDP and German retail sales/unemployment, but the highlight will be German, French, and Italian flash April inflation.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.6bps at 1.736%, 5-Yr is down 1.5bps at 2.044%, 10-Yr is down 2.4bps at 2.497%, and 30-Yr is down 2bps at 2.927%.

- UK: The 2-Yr yield is down 2.3bps at 3.843%, 5-Yr is down 2.8bps at 3.958%, 10-Yr is down 2.9bps at 4.48%, and 30-Yr is down 2.6bps at 5.244%.

- Italian BTP spread up 0.2bps at 111bps / Portuguese up 1.3bps at 55.3bps

PIPELINE: Corporate Bond Update

Apr-29 17:07

Corporate bond issuance looks to finish April strong with at least another $21.5B to price today:

- Date $MM Issuer (Priced *, Launch #)

- 04/29 $9B #World Bank $4B 3Y +35, $5B 7Y +55

- 04/29 $5B *KFW 5Y SOFR+42

- 04/29 $2B #ADQ $1B 5Y +85, $1B 10Y +95

- 04/29 $1.75B *Swedish Export Credit 3Y SOFR+45

- 04/29 $1B #GS Private $400M 3Y +225, $600M 5Y +250

- 04/29 $900M #Tyco Electronics $450M each: +5Y +83, 10Y +97

- 04/29 $800M #Weir Group 5Y +160

- 04/29 $500M #Constellation Brands 5Y +107

- 04/29 $500M Southwestern Public Service 10Y +115

- 04/29 $Benchmark Las Vega Sands 3Y +200, 5Y +225

FOREX: G10 Currencies Trade Mixed, Antipodeans Underperform

Apr-29 17:03

- Despite sentiment in equity markets not necessarily reflecting it, currencies trade with a moderate risk off tone. This has allowed the likes of AUD and NZD to give up the prior session advance, both falling around 0.65% as we approach the APAC crossover.

- Dented sentiment may be stemming from reports regarding Amazon, who on Tuesday denied a report that it planned to list the costs of President Trump's tariffs next to total prices of products after the White House slammed the mega online retailer earlier in the day. The clash came after PunchBowl News, citing an unnamed source, reported the shopping site will soon display the share of a product's cost that is derived from tariffs rolled out this month.

- For AUDUSD specifically, overnight highs at 0.6450 represented 4-month highs for the pair, which has subsequently drifted steadily lower through the session. Initial key support to monitor is 0.6307, the 50-day EMA, of which a clear break would be a concern for the bullish narrative.

- Elsewhere, lower US yields for a second consecutive session appear to be providing a yen tailwind, with USDJPY pressing towards the 142.00 handle. Technical conditions continue to highlight a dominant downtrend for the pair and below here, 141.49 (Apr 23 low) would provide the first support before the market refocuses its attention on cycle lows at 139.89.

- Economic calendar highlights for Wednesday’s APAC session include Australian CPI and China PMI’s. Later in the session, the focus will be on Eurozone inflation/growth data and US Q1 GDP. Other notable releases include US PCE and ADP, the MNI Chicago PMI and Canada GDP.