INFLATION: 1Y Inflation Expectations Trend Lower Whilst 1Y1Y Steady

Jun-25 17:10

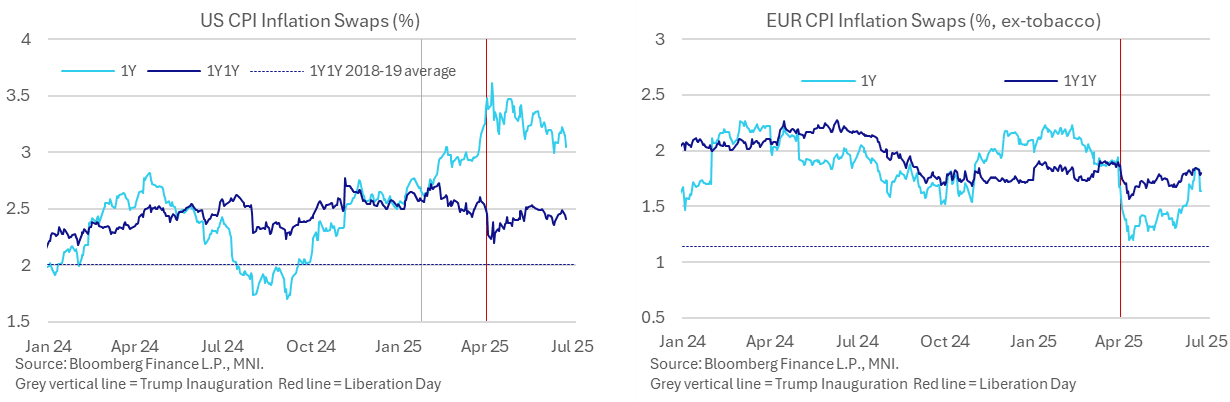

- US 1Y market inflation expectations have been below levels just before US Liberation Day tariff announcements of Apr 2 for most of June although are trending lower.

- However, at 3.05%, these 1Y CPI inflation swaps are only back to late March levels and hold a large portion of the widening vs 1Y1Y expectations since President Trump’s inauguration.

- WTI futures plunged early this week on the limited Iranian response to US airstrikes on nuclear facilities and a subsequent Israel-Iran ceasefire. However, with the August contract at $66/bbl, it’s only back to mid-June levels and at the lower end of pre-tariff rough ranges of $65-70/bbl.

- This is something partly reflected by the recent pullback in surveyed short-term inflation expectations, including in yesterday’s Conference Board consumer survey, leaving them with mixed degrees of relative elevation (see here).

- It follows trade policy de-escalation but with further focus increasingly turning to further trade deal prospects ahead of the current 90-day window ending July 8th.

- EUR CPI swaps meanwhile have seen the opposite, with the 1Y pushing back towards pre-Apr 2 levels having dropped sharply on growth fears. There have however been warning shots recently as deliberations continue – no deal would see tariff rates of 50% on nearly all EU goods exports from July 9th.

- Specifically, Reuters last week reported that European officials are increasingly resigned to a 10% baseline rate on reciprocal tariffs in any US-EU trade deal. One of the sources, an EU official, said negotiating the level down had become harder since the U.S. started drawing revenues from its global tariffs. "10% is a sticky issue. We are pressing them but now they are getting revenues," said the official.

- Bloomberg yesterday then reported that the EU is planning to impose retaliatory tariffs on US imports, including on Boeing, if the US puts a baseline tariff on EU goods.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: USD Set To Finish Off Of Worst Levels

May-26 15:04

The USD has underperformed many of its G10 FX peers for much of the day, with ongoing policy uncertainty continuing to provide headwinds for the greenback after President Trump delayed the timeline for the imposition of 50% tariffs on the EU following a conversation with EC President Von Der Leyen.

- The BBDXY registered a fresh ’25 low, piercing the Dec ’23 low in the process. Bears will look to force a break of the ’23 closing low (1,200.41) next.

- A reminder that liquidity was thinned by the U.S. & UK public holidays.

- EUR/USD extended the recent bullish move, trading as high as 1.1419 before fading back to 1.1380. Next resistance of note seen at the 76.4% retracement of the Apr 21 - May 12 bear leg (1.1453).

- GBP/USD topped out at 1.3593 before a pullback to 1.3560. The 1.382 projection of the Feb 28 - Apr 3 - 7 price swing (1.3605) presents the next upside area of note.

- USD/JPY has recovered from the lowest levels registered in May (142.23 printed in Tokyo trade), with the wider risk reaction to the delay of the tariffs on the EU providing some counter. Spot last deals at 142.80 after reaching 143.08, with bears remaining in technical control. A move through today’s lows would expose the 76.4% retracement of the Apr 22 - May 12 bull leg (141.96). Bulls need to retake the 20-day EMA (144.66) to start turning the tide in their favour.

- Risk proxy FX (AUD, NZD, NOK & SEK) outperformed for much of the session on the U.S.-EU tariff relief but also faded from best levels against the USD.

- Note that AUD/USD cleared next resistance at 0.6515 before fading back to 0.6500.

- U.S. consumer confidence & durable goods data headlines on Tuesday, complimented by Fedspeak from Kashkari & Barkin and ECB speak from Villeroy & Nagel.

US TSYS: TY Closes Opening Gap Lower

May-26 14:51

Tsy futures have closed the gap lower seen at the Asia open, with the contract last flat at 110-02+.

- This comes with e-minis and crude oil futures moving away from session highs, helping counter the sell off that was driven by Trump delaying the imposition of the 50% tariff on the EU.

- The contract’s technical bear cycle that started in early May remains intact.

- Initial support and resistance located at 109-13 & 110-21+, respectively.

- A reminder that activity ahs been limited by the presence of the Memorial Day holiday in the U.S., with cash Tsys closed and futures set to close early (13:00 NY/18:00 London).

- Roll activity has synthetically boosted volumes, latest completion estimates provided below:

- TU: 56.2%

- FV: 54.5%

- TY: 56.2%

- UXY: 44.3%

- US: 57.9%

- WN: 59.9%

- Minneapolis Fed President Kashkari underscored the need for the central bank to remain on hold for “a while” over the weekend, given the macro uncertainty evident at present.

- Fed Funds futures show ~46.5bp of cuts through December vs. ~48bp late on Friday.

- Durable goods and consumer confidence data headline the U.S. calendar on Tuesday, with comments from Fed’s Kashkari & Barkin also slated. Elsewhere, the Treasury will sell 2-Year paper.

EQUITIES: Stoxx Closes Tariff Threat Gap Lower As Trump Delays 50% Levy On EU

May-26 14:36

Euro Stoxx 50 futures hold onto the bulk of the gains that came after U.S. President Trump delayed the imposition of 50% tariffs on the EU over the weekend, with the market now familiar with Trump pushing back tariff deadlines/moderating tariff sizes as a deadline nears.

- A recent BBG report noted that “the European Union said it agreed to accelerate negotiations with the US to avoid a transatlantic trade war, signalling a more amicable approach just days after President Donald Trump criticized the bloc for taking advantage of the US and slow-walking talks.”

- Euro Stoxx 50 futures closed the gap lower that followed Trump’s 50% tariff threat on Friday, last +1.35% or 72 points.

- Our technical analyst notes that a bullish theme in Euro Stoxx 50 futures remains intact and suggests that the recent pullback appears corrective. Moving average studies are in a bull-mode setup, highlighting a clear uptrend and recent gains maintain the sequence of higher highs and higher lows. Sights are on 5,516.00, the Mar 3 high and key bull trigger. Key support to watch lies at 5,223.87, the 50-day EMA.

- Sector-wise, industrials, IT and materials outperform, while utilities lag, a setup you would probably expect on trade-positive news.

- In terms of stock-specific moves, Thyssenkrupp has rallied over 7% after Bild pointed to a restructuring for the name as it looks to cut overheads and divest units.