FOREX: 0.9200 Remains EURCHF’s Line in the Sand, Swiss CPI Next Week

Jan-02 15:13

- The Swiss Franc on balance keeps a strong valuation, having held the majority of its substantial April surge over the course of 2025 in real, trade-weighted terms. Despite this, November’s dip below 0.9200 for EURCHF remained well supported, likely frustrating desks looking for a breakdown below the key level, and points to continued solid demand around this area.

- The hawkish tilt on SNB rate expectations has held over the last couple of weeks. SNB-dated OIS imply around a 20% cumulative chance of an SNB hike by end-26. This comes after the SNB has downwardly adjusted its conditional inflation forecast over the short term but kept its end-of-horizon medium-term view at 0.8% - suggesting they remain confident of an incoming uptick.

- Next week's December CPI is seen picking up to 0.1% Y/Y according to preliminary consensus, and even a temporary drop below 0% would likely be insufficient to put any easing discussions back on the table again. The most probable SNB path ahead is for a policy rate hold over the foreseeable future.

- Analysts seem not overly optimistic about a EURCHF break to the downside: 14 submissions of the Bloomberg survey for an end-26 view on the cross range from 0.92 to 1.02 with a 0.95 median. However, JP Morgan for example, which is not part of that survey, recommends going long CHF as part of a "long fiscal RV basket". A wider risk-off event would expectedly be the most straightforward path to EURCHF pushing lower.

- Looking past EURCHF, of particular note remains CHFJPY, which climbed to new record highs last week, edging closer to the 200 mark.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Post ISM Services React

Dec-03 15:04

- Treasuries scale back support after ISM services data - prices paid and new orders lower than expected while the Services index and employ component rise slightly.

- Currently, TYH6 trades 113-01.5 (+5) vs. 113-07 high, initial technical resistance at 113-11/22+ High Dec 1 / High Nov 25. Support below at 112-22 Low Dec 02

- Curves mildly steeper: 2s10s +.312 at 57.753, 5s30s +1.424 at 110.291.

MNI: US ISM NOV SERVICES COMPOSITE INDEX 52.6

Dec-03 15:00

- MNI: US ISM NOV SERVICES COMPOSITE INDEX 52.6

- US ISM NOV SERVICES PRICES 65.4

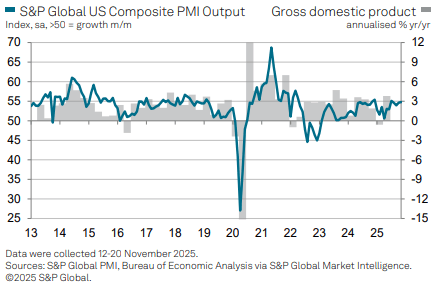

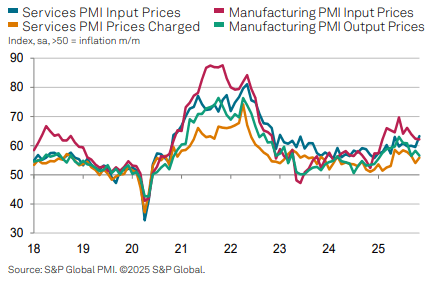

US DATA: Services PMI Revised Lower But Still Solid In Final November Release

Dec-03 14:56

The S&P Global US services PMI was revised lower in the final November release, dipping to its lowest since June rather than confirming what had been its highest since July. Along with this downward revision, input cost inflation was also trimmed from the highest since Jan 2023 in the flash to today’s six-month high, but as you can see in the chart below that's a close call having still seen a solid acceleration in November.

- US Services PMI: 54.1 (flash & cons 55.0) in Nov final after 54.8 in Oct

- US Composite PMI: 54.2 (flash 54.8) in Nov final after 54.6 in Oct

S&P Global US PMI press release opening highlights (release in full, here):

- “The US private sector services economy continued to expand at a solid pace in November, despite growth softening to a five-month low, according to the latest PMI® survey data from S&P Global.”

- “Activity was supported by the firmest rise in new work of 2025 so far, whilst confidence in the outlook strengthened following the end of the government shutdown and expectations of improved economic growth in the year ahead.”

- “Firms also took on additional staff to a stronger degree amid some evidence of capacity pressures, but with reports of higher labor costs and tariffs continuing to push up prices in general, input cost inflation accelerated to a six-month high.”