AUSSIE 10-YEAR TECHS: (Z5) Marked Lower

- RES 3: 95.982 - 76.4% retracement Sep’24 - Nov’24 downleg

- RES 2: 95.960 - High Apr 7 (cont.)

- RES 1: 95.900 - High Oct 17

- PRICE: 95.505 @ 16:03 GMT Nov 26

- SUP 1: 95.450 - Low Nov 26

- SUP 2: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 3: 95.275 - Low Nov 14 (cont) and a key support

Aussie 10-yr futures slipped lower again mid-week on the back of hawkish RBNZ rate cut, compounding the impact of the jobs data earlier in the month. The sustainability of the pullback will be dependent on prices holding above key short-term support at 95.510, the Sep 3 low. Near-term resistance remains 95.780, the Sep 12 high. A clear break of this level signals scope for a continuation higher and opens 95.960, the 76.4% retracement level for the Sep’24 - Nov’24 downleg.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (Z5) Strong Weekly Close

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 96.555 @ 15:52 BST Oct 27

- SUP 1: 96.280 - Low May 15 (cont.)

- SUP 2: 95.900 - Low Jan 14 (cont.)

- SUP 3: 95.760 - Low 14 Nov ‘24

Aussie 3-yr futures briefly bounced on the US CPI print keeping focus higher despite the break of support last week. Short-term resistance at 96.615, the Sep 12 high, has been broken, with 96.780 is the next upside target. Clearance of this level puts markets at fresh multi-month highs. 96.280 marks next major support - but markets are some way off this mark now.

AUSSIE BONDS: Front End Yields Higher, Nov Easing Odds Lower Post Bullock

Aussie bond futures are mixed, as the 3yr (YM) underperforms, down 3.5bps to 96.545, while the 10yr (XM) drifts higher to 95.815 (+1bps). This mirrors US Monday moves to a degree, although cautious comments from RBA Governor Bullock from early Monday evenings are also likely in play. ACGB yields are firmer at the front end, 2 and 3yr up +4bps, the back end softer, with the 10yr under 4.17%. The 3yr yield is back challenging key EMAs, although the 200-day at 3.52% is still intact. The 3/10s curve is flatter, last +72bps, levels last seen in April.

- Bullock said that they remain cautious and that they need more information on inflation (Q3 CPI out 29 October) and the labour market given the volatility of the monthly numbers. The AUD OIS market has around 10bp of easing priced in for 4 November and 16bp by year end, less than prior to Bullock’s comments (we had 16bps of easing priced for Nov at the end of last week.

- The AU-US 10yr spread is +19bps and risks are tilted higher amidst the current macro backdrop/more cautious RBA.

- All eyes rest on tomorrow's CPI print. We may need to see the trimmed mean surprise below 2.7%y/y expected (say around 2.5%) to renew confidence in RBA easing risks returning for the Nov meeting.

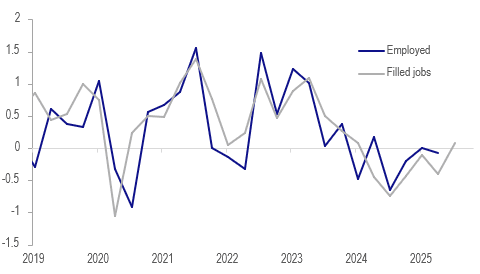

NEW ZEALAND: Filled Jobs Signal Q3 Labour Market Stabilisation

Q3 NZ filled jobs rose 0.1% q/q signalling that employment likely stabilised in the quarter after falling 0.1% q/q in Q2. Q3 labour market data print on 5 November and will be an important input into the 26 November RBNZ decision. September jobs rose 0.3% m/m to be down 0.4% y/y up from August’s +0.1% m/m & -0.9% y/y. Vacancies are also consistent with the start of a labour market recovery as SEEK job ads rose each month in Q3 to be up 4.3% q/q.

- Q3’s rise in filled jobs was the first since Q1 2024 and the labour market was slowing at that time.

NZ employment q/q%

- The largest monthly rise in filled jobs in almost two years was driven by the services sector. Services rose 0.4% m/m, goods-producers +0.1% m/m but primary industries fell 0.5% m/m.

- Compared to a year ago education and healthcare outperformed with jobs up 2.0% y/y and 1.8% y/y respectively. The market economy’s demand for labour is weak with construction down 4.5% y/y, professional & technical services -2.6% and manufacturing -1.7% but lower rates may help this turn around in coming quarters.

- Youth employment remains a problem with filled jobs for 15-19 years down 6.6% y/y, but there has been an increase in those in education since the labour market weakened. 20-24 years is 2.6% y/y lower and 25-29 -2.9% y/y.